Narrative and the prices on screen

The emotional version of this story is easy to sell. Labor union wants to tax billionaires. Tech money wants to kill it. California is fighting over whether to backfill healthcare and social spending with a one-time levy on extreme wealth.

The market version is colder. On Polymarket, as I am typing this line, the dedicated ballot contract prices qualification at about 66%, while the passage contract prices final enactment at about 38%. In other words, traders think the measure is more likely than not to reach the ballot, but still more likely to fail than pass. That basic two-step framing is correct. The real question is whether the market is still overpricing the second step.

The key number is the market’s implied conditional probability. If the measure is 38% to pass overall and 66% to make the ballot, then the market is implicitly saying:

On Kalshi, the "ballot qualification" contract price is 68%, and the passage contract price is 38%. This gives the same conditional probability at 55.9%.

So the screen is effectively telling you that once the measure qualifies, it becomes roughly a 57% favorite in November. That is the part I still dispute. The new polling from SurveyUSA is better for Yes, but not good enough to justify a near 60-40 conditional favorite.

The proposal

The proposal itself is straightforward enough. California’s Legislative Analyst’s Office says the initiative would impose a one-time 5% tax on the net worth of billionaires who were living in California on January 1, 2026. The tax would be due in 2027, taxpayers could spread payments over 5 years, and real estate, pensions, and retirement accounts would be excluded. 90% of the money would be set aside for healthcare.

The LAO also says the tax would likely generate a temporary revenue windfall measured in tens of billions of dollars, but could also produce an ongoing decrease in state income-tax revenue of hundreds of millions of dollars or more per year if billionaires change behavior or leave the state. That is not campaign spin but the state’s own nonpartisan fiscal office putting the upside and downside in the same paragraph. And that is the sort of sentence opponents will turn into a weapon. You do not need to prove the measure is economically disastrous. You only need to make enough swing voters uncomfortable with the tradeoff.

The qualification mechanics are also concrete. The Secretary of State says the initiative was cleared for circulation on December 26, 2025, requires 874,641 signatures, has a circulation deadline of June 24, 2026, and had already reached the 25% signature milestone on February 26, 2026. The dedicated market exists for that branch, it has more direct information than public commentary, and the public facts do not obviously refute a mid-60s qualification probability. So for pricing purposes I treat the market’s 66% qualification number as basically fair.

Polling data

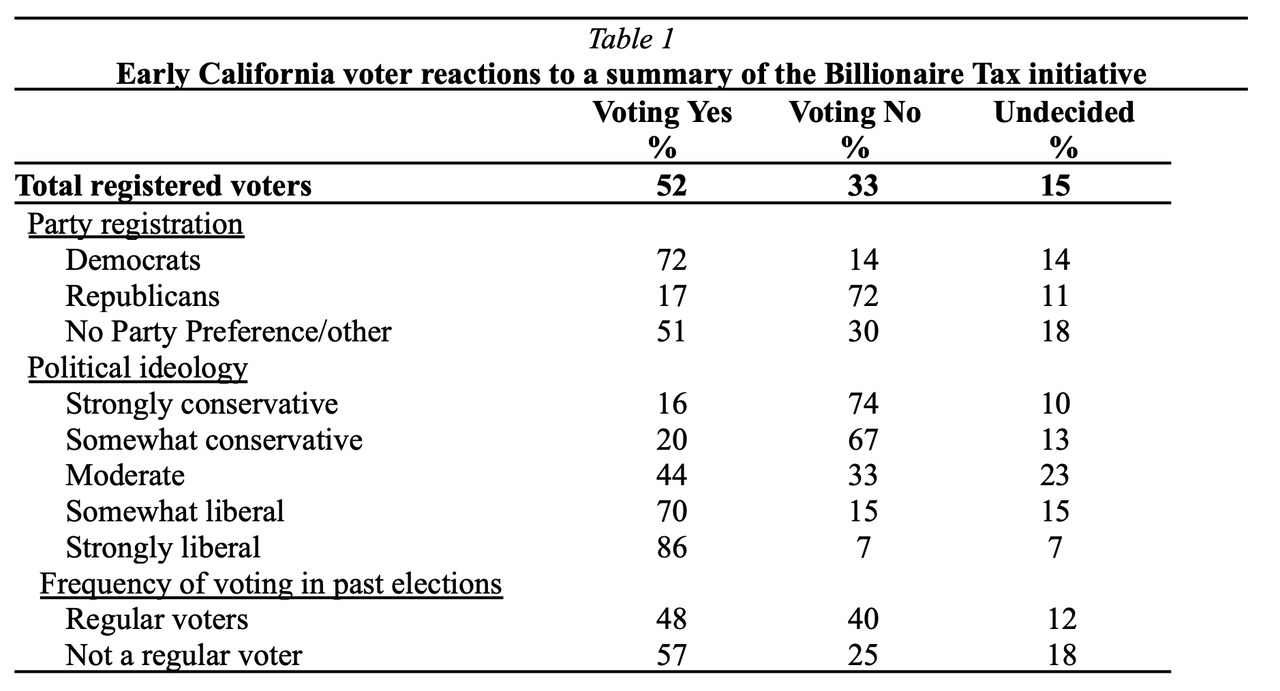

Given the market-implied 57% conditional pass probability in the draft, the real question is not whether the initiative has support. It clearly does. The available public polling shows a genuine lead. Berkeley IGS, fielded March 9-15, found 52% Yes, 33% No, and 15% undecided among California registered voters (with a 2% margin of error). SurveyUSA, fielded April 8-10, found 63% Yes, 23% No, and 14% not sure among registered voters (with a 4.2% credibility interval). That is not a weak measure. But it is also not a measure with no room to move.

The more important point is how that support is distributed. Berkeley crosstabs shows strong partisan asymmetry: Democrats support the measure 72% to 14%, while Republicans oppose it 72% to 17%. Among No Party Preference/other voters, support is positive but softer at 51% Yes to 30% No. Berkeley also shows a turnout-skewed electorate: among regular voters, support drops to 48% Yes and 40% No, compared with 57% Yes and 25% No among non-regular voters.

SurveyUSA, meanwhile, shows support holding above 60% across major regions, at 61% in the Inland region and 66% in the Bay Area. So the combined data do not say the measure is barely alive. They say it leads. But they also say the coalition is uneven, geographically broad, partisan in composition, and less dominant among higher-propensity voters.

That is why I would frame the disagreement with the market more narrowly. The polls support the claim that the initiative is a real contender and that majority sentiment currently exists. What they do not prove is that a qualified measure should automatically be priced as a near 57% favorite to pass. In both polls, a large bloc remains available to persuasion: Berkeley has 48% either No or undecided, and SurveyUSA still has 37% either No or not sure. For a highly controversial tax initiative facing an expensive opposition campaign, that is still a meaningful amount of movable ground. The data justify a positive baseline, but not an unqualified green light.

Why the structure still matters

The reason I still do not buy the market’s 57% conditional-passage assumption is that this is not just a polling contest. It is a campaign contest. The opposition has real money and real institutional tools. The Guardian reports that Sergey Brin alone has given $45 million to oppose the measure, and that the same anti-tax network is funding related efforts, including a rival “Protect Retirements” measure aimed at crippling the wealth-tax framework. Recent San Francisco Chronicle reporting says that if both measures pass, the one with more Yes votes would override the other. That creates a second layer of risk beyond simple voter approval. At the same time, CalMatters reports real discomfort inside the progressive coalition itself, with some liberal lawmakers and labor groups unconvinced even before the full paid war begins. That is not what an easy game looks like.

My probabilities

My base case is:

P(Qualifies by June 25) = 66%

P(Wins in November | Qualified) = 47%

So:

P(Passes) = 0.66 × 0.47 = 31%

Against a live market price of 38%, the contract still looks rich by about 7 percentage points.

Why 66% for qualification? Because the measure has a serious union backer, real salience, and enough runway to remain more likely than not to qualify (the circulation deadline is June 24). But given the intensity of billionaire-funded counter-mobilization and the fact that circulation is still at its early stage, we still need to be cautious. I do not claim an edge here as I think the tradable disagreement is in the conditional branch.

Why 47% for conditional passage? Because the polling data does not show a hardened majority. It is a soft lead that must survive months of paid attacks, fiscal criticism from a nonpartisan state office, capital-flight messaging, and rival-measure confusion. The key thing is not the support rate in March/April. It is the fact that the measure probably needs to enter late October already above the low-to-mid 50s to survive a fully funded anti-tax blitz. Right now it is not there.

What will reprice this market

The first catalyst is the signature and certification window. This is the obvious one. Until the measure is officially on the ballot, the market is really trading both qualification and passage together. Any strong evidence of signature sufficiency should lift the "Yes" price mechanically. Any sign of delays, weak collection pace, or ballot-law complications should hit Yes immediately. The relevant deadline is late June.

The second catalyst is the next serious public polling wave with cross-tabs. Not another vague “Californians support taxing the rich” sentiment readout, but a ballot-wording poll after both sides have been on air. Watch independents and late deciders, not Democrats. If independents slide from 51% support toward the mid-40s, the conditional passage probability should compress fast. If they hold or improve, the market’s current pricing becomes harder to fade.

The third catalyst is the rival-measure battlefield. If the poison-pill countermeasure qualifies, the billionaire tax market should cheapen even if the tax itself qualifies, because the path to victory becomes more complex and more expensive. Conversely, if the rival effort stalls while the tax qualifies cleanly, the "Yes" price could bounce even without better polling. The market is likely to be underpricing this interaction risk due to simple binary ways of thinking.

The trade

The cleanest trade is still No on final passage, NOT No on qualification. I do not see a large enough public-data edge against the dedicated qualification market to fight it hard. But I do see a real edge against the idea that qualification turns this into a probable November winner.

For people who can structure it, the sharper expression is a conditional spread trade: trade the tree, not the slogan. Stay relatively neutral on the ballot leg and fade the passage leg. In plain English, the disagreement is not “will this initiative get close enough to be real?”. The disagreement is “once it is real, should it really be priced like a modest favorite?”.

The market is now pricing the measure as if high-50s conditional passage is the natural consequence of qualification. The data says that it is still too generous. If qualification happens and the market reflexively reprices the passage contract as if ballot access solved the hard part, that could be the moment to re-short Yes. Ballot qualification removes one risk, but it also starts the expensive, high-information phase where soft support usually gets stress-tested.

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.