A couple of weeks later, I think the Illinois Democratic primary was actually pretty simple.

Traders looked at the races and basically said: okay, who has the biggest pile of cash, the fanciest profile, or the most recognizable name? Then they bought that candidate.

Trading Real-World Events on Prediction Markets

Voters were playing a different game. They cared more about who had the real local backing, the better endorsement chain, and the stronger on-the-ground coalition. So the market was betting on the glossy campaign brochure, while the electorate was voting on neighborhood plumbing. That’s why the pricing got so silly.

Take the Senate race. Right before the vote, Kalshi had Raja Krishnamoorthi around 56%-61% and Juliana Stratton around 40%-44%. Raja also had the kind of balance sheet that makes traders weak in the knees: about $30 million raised plus more than $19 million transferred from his House account. On paper, that looks like a monster favorite.

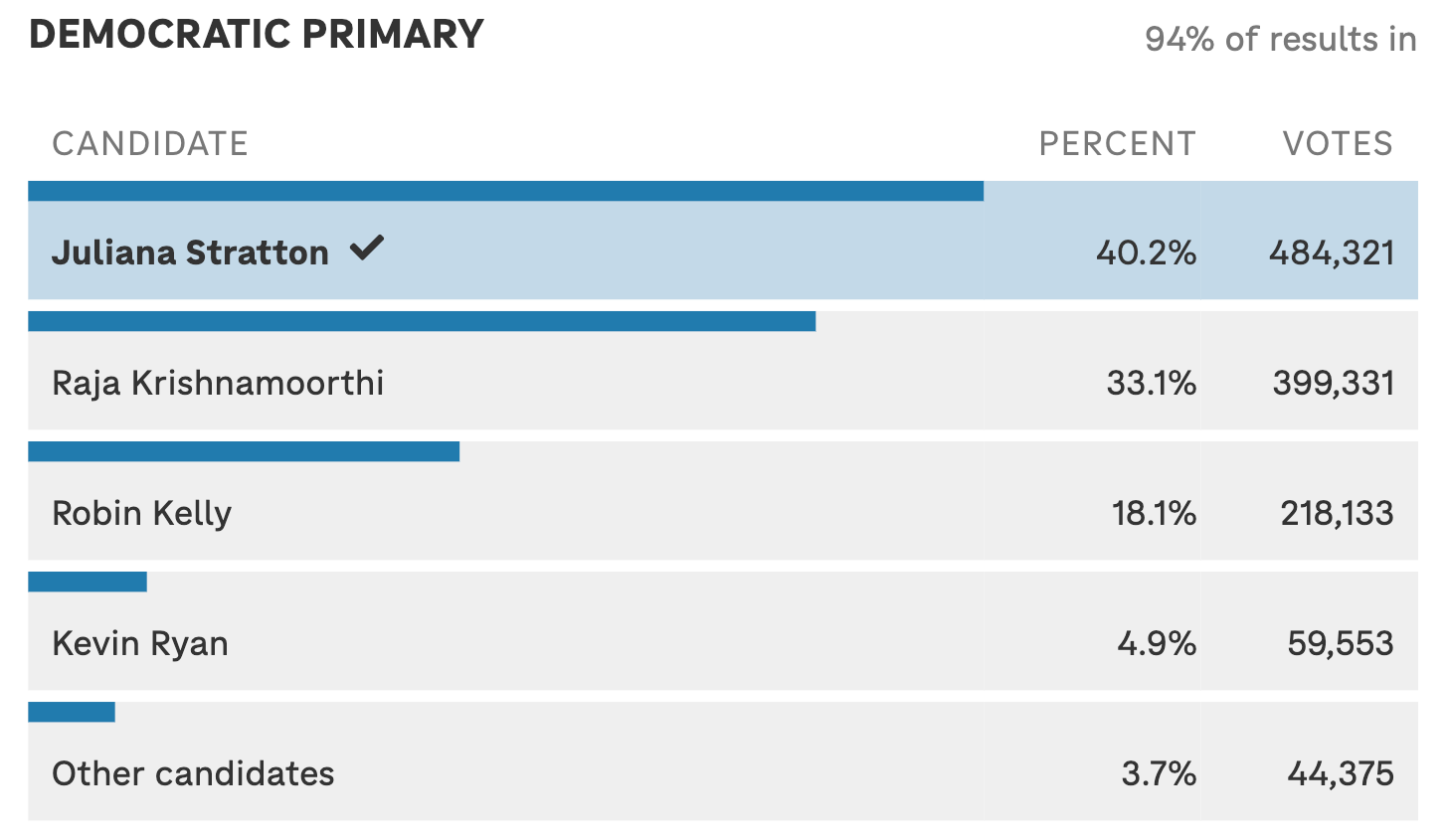

Then Stratton won anyway, at roughly 40%, with Raja at about 33% and Robin Kelly at 18%.

The Senate margin market on both Kalshi and Polymarket are trading at 95+% on “Stratton 6–9%”.

And that’s really the whole story. The market saw money and assumed money would turn into votes. But Illinois was a crowded, no-runoff primary with heavy early voting.

In that kind of race, money matters, sure, but it’s not magic. If another candidate has the cleaner coalition, the better machine support, and the more natural fit with the electorate, your giant ad budget can start to look a bit like bringing a gold-plated fork to a street-food contest. Nice fork. Still not the point.

What makes the miss more interesting is that the market had multiple chances to avoid it.

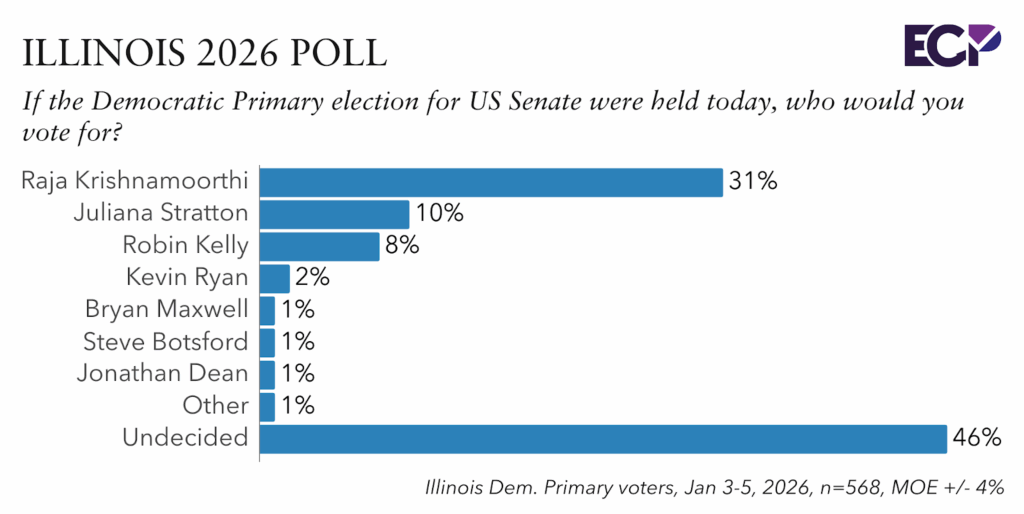

Emerson’s January poll had Krishnamoorthi at 31%, Stratton at 10%, Kelly at 8%, and 46% undecided. That should’ve scared traders. With nearly half the vote still up in the air, “Raja’s leading” was a lot less solid than it looked.

Same with the expectation data. NPR Illinois said likely Democratic voters thought Krishnamoorthi would win 46% to 20% over Stratton, with Kelly at 16%. But that wasn’t proof. It was more like everyone telling each other the same story and then mistaking it for reality.

Then the race shifted. Immigration and ICE became more important late, and that fit Stratton better. The market was still asking who had more money and ads. Voters were asking who sounded more like them. By then, the price was stale.

The funniest part is that the Senate race wasn’t even the only example. The market made the same mistake in the House races too.

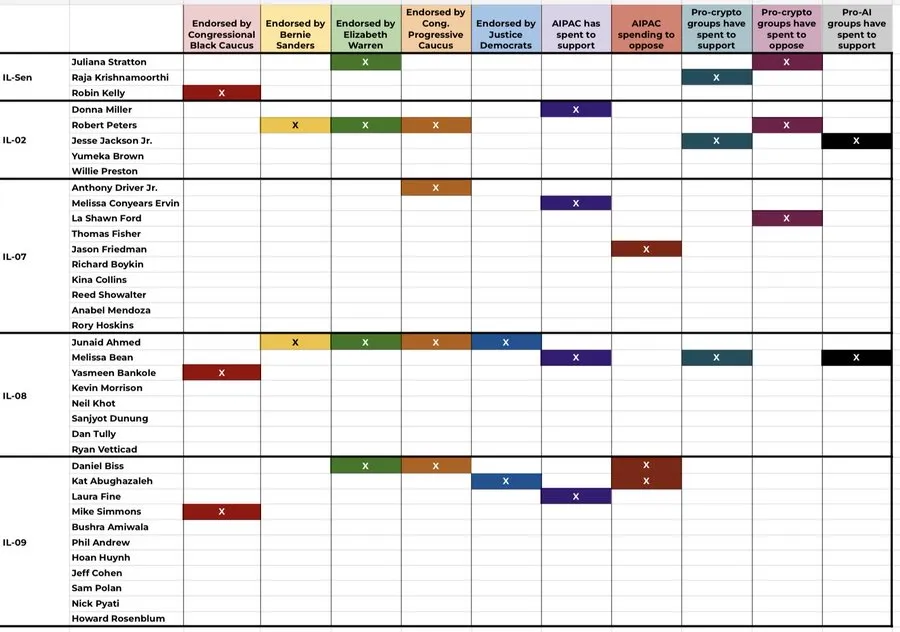

In IL-02, Kalshi had Jesse Jackson Jr. around 74%–76%, and then he lost badly to Donna Miller, who won about 40% to 29%.

Miller's organized credibility brought him this victory. He had a cleaner profile, the fundraising lead, and enough organizational ballast. Illinois showed that, in fractured Democratic primaries, transferable networks beat famous surnames.

In IL-07, Melissa Conyears-Ervin was around 73% on Kalshi and still lost to La Shawn Ford.

Ford had the one asset that mattered more in a crowded, low-plurality race: Danny Davis’s succession blessing. He won with just 23.9% to Conyears-Ervin’s 20.5%, which is exactly the kind of result you should expect when a local machine handoff outruns paid media.

So this wasn’t one weird pricing error. It was a pattern. Traders kept paying up for the candidate who had the strongest surname recognition or who looked strongest in a fundraising memo, while voters kept rewarding the candidate with the better real-world network.

The market was broadly right only where coalition ownership was clearer, like Melissa Bean in IL-08, who won 32% to Junaid Ahmed’s 26.5%, and Daniel Biss in IL-09.

That’s the part prediction markets still get wrong more often than they should. People love measurable things. Cash totals are measurable. Famous last names are easy to recognize. TV ad saturation feels concrete. Coalition strength is messier. Local endorsements are messy. Transferable political networks are messy. But messy things still win elections.

And honestly, that’s why this was such a good lesson. The market wasn’t fooled by some last-minute shock out of nowhere. It just put too much weight on the wrong variables. It treated “most money” as if it meant “most likely to finish first”.

In a fragmented plurality race, that’s just not reliable. Sometimes the richest candidate is the best candidate. Sometimes he’s just the guy burning money while someone else is quietly stacking actual voters.

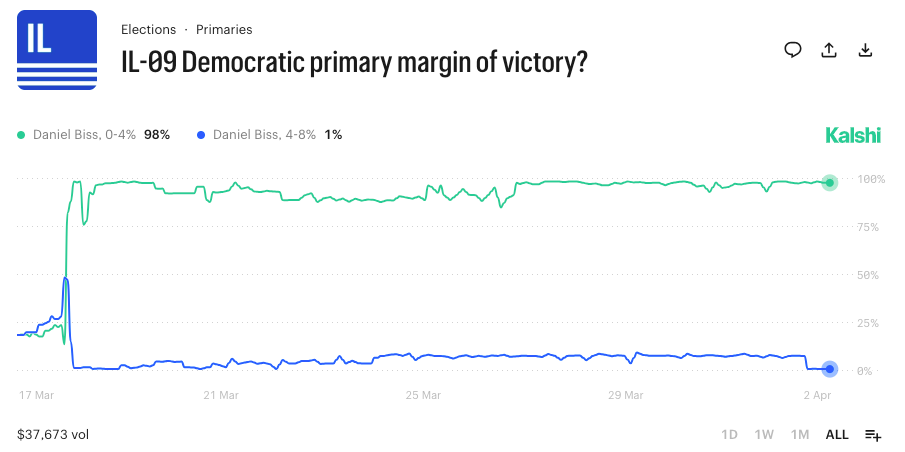

In addition, the best hedge in races like these is usually not candidate-versus-candidate. It is winner plus margin.

In Illinois, crowded fields compressed victory bands. Kalshi’s IL-09 market had Biss by 4-8 points at 29 cents and Biss by 0-4 at 24 cents shortly before polls closed, which was a far more realistic read of a 15-candidate plurality race than paying up for a cartoon blowout.

That framework generalizes well: in future no-runoff Democratic primaries, pair the undervalued coalition candidate with narrower margin bands rather than paying for a dominant-win narrative.

There was an instance where prediction markets picked Texas Democratic Primary winner but missed on GOP race.

Now that the primary is over, the edge is gone. The market has mostly gone back to treating Illinois like Illinois. But the lesson is still useful, especially if you trade primaries.What I’d remember next time:

- Cash isn’t a coalition

- Big names get overpriced most of the time

- In crowded no-runoff races, local political machinery matters more than traders want to admit

- If the market is buying the obvious story, check whether voters are playing a different game

If you want the one-line version: Illinois wasn’t a story about voters doing something shocking. It was a story about traders doing something lazy.

How to Trade and Profit on Prediction Markets?

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.