Prediction markets often look like separate bets, but related contracts can be stitched together into one implied probability model that hints deeper pricing. Colombia’s 2026 first-round election markets are a good example. The first-round winner market, second-place market, third-place market, advance-to-runoff market, standalone outright-win market, and final-winner market are not independent signals. They are different slices of the same election tree.

The basic electoral rule is simple: Colombia holds a second round on June 21 if no candidate wins more than 50% of valid votes in the first round on May 31. Polymarket’s first-round winner market resolves to the candidate with the greatest number of valid votes, regardless of whether that candidate clears 50%. The same logic applies to the second- and third-place markets. The advance-to-second-round market resolves to the pair that advances, but if someone wins outright in the first round, it resolves to “1st Round Outright Winner.”

The market’s implied ranking

The first-round winner market has Iván Cepeda Castro at about 65%, Abelardo de la Espriella at 35.1%. That means the market thinks Cepeda is the most likely first-place finisher.

The second-place market then fills in the next layer. It prices De la Espriella at about 61% to finish second, Cepeda at 31.8%. This is exactly what we would expect if the two main rank-order paths are (1) Cepeda first, De la Espriella second and (2) De la Espriella first, Cepeda second.

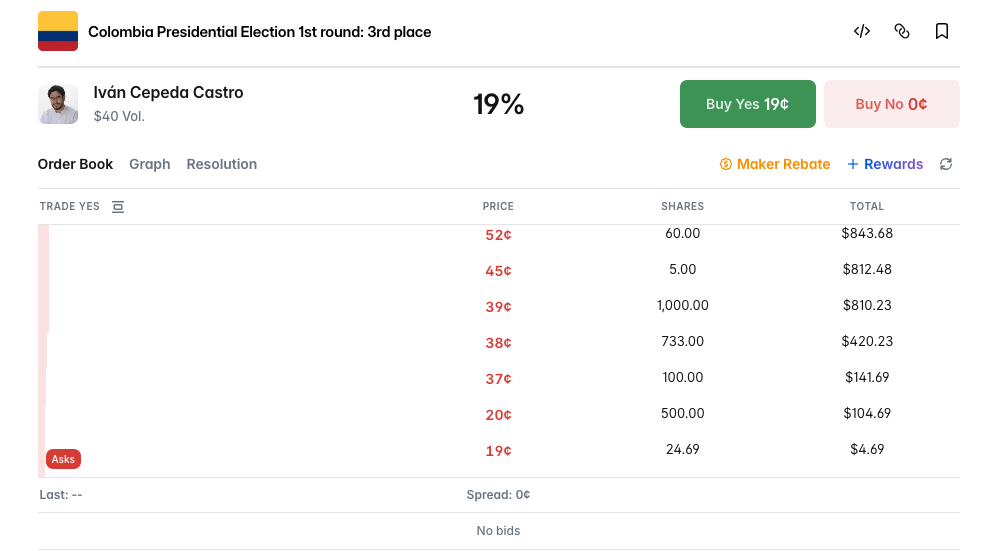

The third-place market makes the implied ranking even clearer. It shows Valencia as the dominant third-place candidate, although this market is thin.

Furthermore, Cepeda's odds on this market are displayed at 19% on the webpage, which does not make any sense at first glance. However, it is not difficult at all to find out there is no bid in the order book. In other words, you cannot simply sell YES at the displayed price and capitalize your "alpha" due to a lack of liquidity.

So the precise price should not be over-interpreted, but the direction is clear: the market expects Valencia to finish behind Cepeda and De la Espriella.

The advance market fits the ranking markets

The advance-to-second-round market prices the pair De la Espriella + Cepeda at about 81%, while the outright-winner branch is about 15% (there is a standalone outright-winner market as well).

The key calculation is for a conditional probability:

This means the market is not merely saying De la Espriella and Cepeda are likely to be top two. It is saying something more precise:

Conditional on there being a runoff, the runoff is overwhelmingly likely to be Cepeda versus De la Espriella.

That is consistent with the first- and second-place markets. Cepeda is the most likely first-place finisher, and De la Espriella is the most likely second-place finisher.

The important caveat is that the first- and second-place markets are resolved by vote ranking even if someone wins outright. But the advance-to-second-round market does not name a candidate pair if someone wins outright. It resolves to “1st Round Outright Winner.”

That means we should not compare these markets too mechanically.

For example:

This is why the correct relationship is:

So if the advance market has Cepeda + De la Espriella at 81% and outright at 15%, the implied probability that Cepeda and De la Espriella are the top two in raw first-round vote ranking could easily be in the low-to-mid 90s. That fits the first- and second-place market, where De la Espriella and Cepeda together account for roughly 98% and 93% of displayed first- and second-place probability.

Consistency check

The markets pass the main logic tests.

First, the standalone outright market and the advance-market outright branch are aligned at roughly 15%. That is the most important identity.

Second, both markets say there is about an 85% chance of a runoff, and within that runoff state, about a 95% chance that the pair is Cepeda and De la Espriella. That is consistent with the first-place and second-place markets.

Third, the third-place market, although very thin (to the extent that existing limit orders hardly get filled), supports the same hierarchy by putting Valencia as the most likely third-place finisher.

The final winner market

If De la Espriella is priced around 67-70% to win the presidency, while the Cepeda + De la Espriella runoff pair is priced around 81%, the market is implicitly assigning him a very high probability of beating Cepeda in the second round.

A rough way to see this is (if cases where De la Espriella reaches a runoff against Valencia or another candidate are ignored):

where A is De la Espriella and C is Cepeda.

Since the overall outright branch is 15%, and De la Espriella is only about 35% in the first-round winner market, a simple allocation would put his outright-win contribution at roughly 15%×35%=5.25%.

If his final-winner market is around 67%, then the implied runoff conversion is approximately:

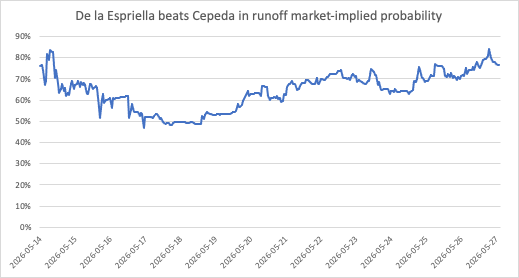

Using the same logic, we can calculate a time series of the market-implied probability that De la Espriella beats Cepeda in a runoff.

The chart shows the market gradually moving from uncertainty about De la Espriella’s runoff strength toward a much more aggressive conditional view.

The lows around May 17-18 reflect that the race had not yet fully consolidated around the De la Espriella versus Cepeda runoff frame back then. The rebound after May 19 reflects the market increasingly pricing him not merely as a top-two candidate, but as the likely winner of a Cepeda-De la Espriella runoff. That is directionally consistent with two recent polls. Invamer’s poll, conducted May 13-20, indicated Cepeda beating De la Espriella 52.4% to 45.3%, with a 2.4-point margin of error. AtlasIntel’s poll, conducted May 18-21, showed De la Espriella beating Cepeda in a runoff by 50.0% to 41.3%, with a 1-point margin of error.

Conclusion

The Colombia markets are useful because they show why related prediction markets should not be read one by one. The first-round markets and the advance market support the same structure: Cepeda will meet De la Espriella in the runoff if there is one. The final-winner market then adds the more controversial assumption. It implies that De la Espriella is heavily favored to win the expected runoff against Cepeda. Whether that assumption is correct is a polling and turnout question. But the linked-market structure makes the assumption visible.

That is the value of reading these contracts together. The headline price tells us who the market thinks is likely to win at each stage. The market complex helps us decompose.

Below are two of my previous articles that apply the same way of thinking.

Andy Burnham Is the Favourite. That Does Not Make Him Inevitable

California’s Billionaire Tax Looks Strong - Until You Look Closer

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.