Strategy (NASDAQ: MSTR), formerly MicroStrategy, disclosed on June 1 that it had sold 32 BTC during the period from May 26 to May 31. If the company sold Bitcoin before May 31, then a market asking whether MicroStrategy sold any Bitcoin by May 31 sounds like it should resolve Yes.

And yet, the market was proposed to resolve No, then disputed twice.

That sounds absurd at first. But the deeper issue is not whether Strategy sold Bitcoin. The deeper issue is whether a prediction market should resolve based on the historical facts of an event, or based only on evidence that was publicly available before the market deadline.

The one-day gap between the sale window and the public filing exposed a major design problem in event contracts: when the event happens before the deadline but proof arrives after the deadline, who should get paid?

What happened

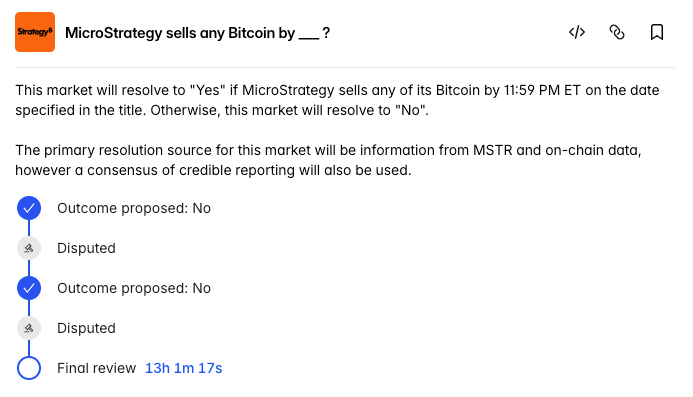

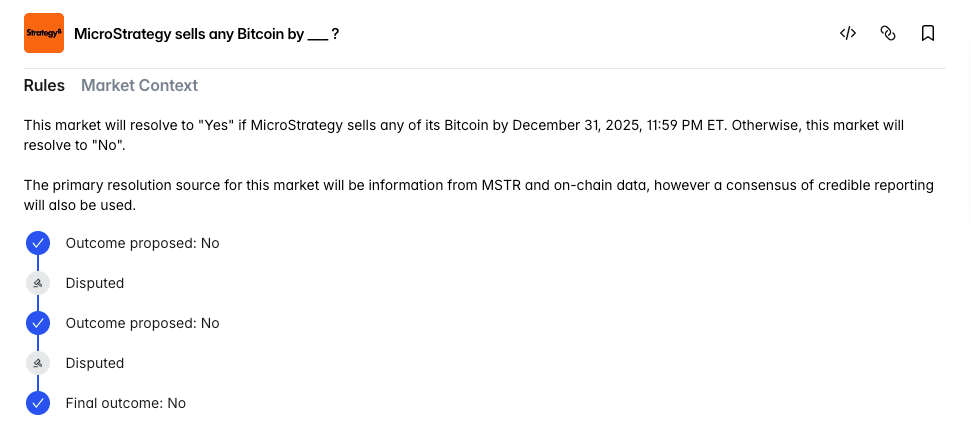

The market said it would resolve Yes if MicroStrategy sold any of its Bitcoin by 11:59 PM ET on the date specified in the title. Otherwise, it would resolve No. The primary resolution source would be information from MSTR and on-chain data, with credible reporting also usable.

For the May 31 market, the key deadline was therefore May 31 at 11:59 PM ET.

Before that deadline, there was no clear public confirmation that Strategy had sold Bitcoin. Traders did not have an official announcement from the company, a confirmed filing, or a broad consensus of credible reporting proving that a sale had occurred.

Then, on June 1, Strategy disclosed that it had sold 32 BTC during the May 26 to May 31 period. The sale was small relative to Strategy’s massive Bitcoin holdings, but symbolically important because Strategy had long been associated with a “never sell” Bitcoin narrative. The sale also mattered enormously for the Polymarket contract, because it seemed to confirm that the underlying event had happened before the market deadline.

The Yes case: the market was about the event

The strongest Yes argument starts from the plain wording of the market rules.

The rule did not say “MicroStrategy announces a Bitcoin sale by May 31.” It did not say “MicroStrategy publicly confirms a Bitcoin sale by May 31.” It said the market resolves Yes if MicroStrategy sells any of its Bitcoin by the specified deadline.

That sounds like an occurrence-based condition. The decisive question should be whether a sale happened before the deadline, not whether the sale was announced before the deadline.

From this perspective, the June 1 filing is not a new event. It is later evidence of an earlier event. The filing did not cause the sale to happen. It merely revealed that the sale had already happened.

In many real-world contexts, evidence often arrives after the underlying event. If prediction markets always ignored later evidence about earlier events, some markets would resolve against the truth simply because the relevant confirmation arrived too late.

Under this interpretation, the purpose of the market was to determine whether Strategy sold Bitcoin. Since Strategy later confirmed that it did, the market should resolve Yes.

That is a clean and intuitive argument.

The No case: the market was about verifiable evidence by the deadline

The strongest No argument starts from a different principle: prediction markets require finality.

A deadline is not just decorative. It defines the end of the market’s factual observation window. Traders need to know what universe of evidence counts. If evidence published after the deadline can determine the result, then the deadline becomes less meaningful.

This is especially important in markets involving corporate disclosures. A company may conduct an action before the deadline but disclose it later. If post-deadline evidence is always admissible, traders are effectively betting on hidden corporate records, not publicly observable events.

That creates several problems.

First, it creates information asymmetry. Insiders or people with better private information may know that an event occurred before public traders do. If public confirmation can arrive later and still decide the market, then ordinary traders are exposed to hidden-information risk.

Second, it creates hindsight resolution. A market that appeared unresolved at the deadline can flip days, weeks, or even months later because new evidence emerges. That turns resolution into a retrospective investigation rather than a clean settlement process.

Third, it creates manipulation risk. If an event can happen before a deadline but be disclosed after it, then the timing of disclosure can affect market outcomes. Companies, governments, campaigns, or other relevant actors may not be trying to manipulate a prediction market directly, but their disclosure timing can still determine who gets paid.

Fourth, it creates a slippery boundary. If evidence released one day later counts, what about one week later? What about one month later? What if a later lawsuit, audit, memoir, or government report proves that something happened before the deadline? At some point, the market stops being a prediction contract and becomes a historical research project.

Under this interpretation, the June 1 filing may prove that the event happened, but it should not matter for a market that closed on May 31. The relevant question is not “what do we know now?” It is “what could be established by the stated deadline?”

That is also a clean and defensible argument.

The real problem: the natural-language rules & the evidence universe

The most important point is that this dispute was caused by a mismatch between the market’s natural-language question and its evidence universe.

The phrase “sells any Bitcoin by May 31” sounds event-based. It asks whether a corporate action occurred before a time cutoff.

But the resolution mechanism relies on sources: information from MSTR, on-chain data, and credible reporting. Once a contract depends on sources, the timing of source availability becomes crucial.

The market did not clearly state whether post-deadline evidence could be used if it confirmed a pre-deadline sale. That missing sentence created the whole dispute.

The problem is that the actual market language left room for both an event-based interpretation and a confirmation-based interpretation. Yes traders were trading occurrence. No traders were trading confirmation. Once the June 1 filing arrived, the dispute became inevitable.

Why “on-chain data” does not fully solve the issue

One might argue that Bitcoin is on-chain, so this should have been easy. If Strategy sold Bitcoin before May 31, surely the blockchain would show it.

In practice, it is more complicated.

On-chain data is public, but corporate wallet attribution is not always complete or universally agreed. Even if a wallet moves BTC, traders still need to know whether the wallet belongs to Strategy, whether the transfer represents a sale, whether it is a custody movement, whether it is an internal reorganization, or whether it is connected to a broker or exchange transaction.

A blockchain transaction is objective. The interpretation of that transaction is not always objective.

This matters because the market did not simply ask whether any Strategy-linked wallet moved Bitcoin. It asked whether MicroStrategy sold Bitcoin. A sale is an economic transaction, not just a blockchain movement. Without official confirmation, credible reporting, or highly reliable wallet attribution, on-chain evidence may not be enough for ordinary traders to verify the event before the deadline.

So while “on-chain data” sounds like a clean resolution source, in this context it may still require judgment. That judgment becomes even harder when the relevant company disclosure arrives after the deadline.

The dispute process should not become a deadline extension

Another important issue is the role of the dispute process.

A dispute window exists so participants can challenge whether the proposed resolution follows the rules. It should not automatically extend the market’s factual deadline.

If new evidence released during the dispute period can determine the outcome, then the effective deadline is no longer the date written in the market. The real deadline becomes the end of the dispute process. That is dangerous because traders are no longer betting only on what happens by 11:59 PM ET. They are also betting on what evidence might emerge while the market is under review.

That creates a moving target.

However, there is also a cost to an extremely strict cutoff. If the market refuses to consider any post-deadline evidence, it may resolve against the true event. In the MicroStrategy case, this is exactly why the dispute feels uncomfortable. Strategy’s own filing appears to confirm that the sale occurred during the market window. Ignoring that fact may feel like choosing procedural finality over reality.

But that trade-off needs to be decided before the market opens. It cannot be improvised after money is already on the line.

The platform should not let traders discover the true resolution philosophy only after a dispute begins.

The platform’s lesson: technical correctness is not enough

Polymarket may have a defensible argument for No if it applies a hard deadline rule. But even if that resolution is technically defensible, the broader user-experience problem remains.

Many ordinary users would naturally read the market as “Did Strategy sell Bitcoin by May 31?” If the answer is historically yes, but the payout is No because confirmation arrived one day later, those users will feel trapped by a technicality.

That feeling matters as prediction markets depend on trust. Traders need to believe that the contract they are trading means what it appears to mean. If the natural reading of the rules points one way while the resolution convention points another way, the platform may win the dispute but lose user confidence.

The solution is not to eliminate edge cases. That is impossible. The solution is to standardize market types more clearly.

In my opinion, Polymarket and similar platforms should explicitly distinguish between at least two categories:

- Event-occurrence markets: the question is whether an event indeed happened by the deadline, and later authoritative evidence can be used to verify it.

- Public-confirmation markets: the question is whether credible public evidence exists by the deadline.Evidence emerged after the deadline will not be taken into consideration.

Each category should have standard language about evidence timing. Especially for corporate actions, government decisions, and private meetings, the admissibility of post-deadline evidence should not be left implicit.

Prediction markets are not courts

This case also highlights a philosophical difference between prediction markets and courts.

Courts often try to reconstruct historical truth. They can subpoena records, wait for discovery, hear testimony, and spend years determining what really happened.

Prediction markets cannot operate like that. They need fast, predictable, and scalable resolution. A market with millions of dollars in volume cannot wait indefinitely for perfect evidence. Finality is part of the product.

But prediction markets also cannot completely ignore truth. If markets frequently resolve against what obviously happened, users will stop treating them as credible information mechanisms.

So the goal is not simply “truth at all costs” or “deadline finality at all costs.” The goal is rule clarity.

If a market is designed to trade public confirmation, say so. If it is designed to trade historical occurrence, say so. If post-deadline evidence counts, say so. If it does not count, say so.

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.