SK Hynix, one of the leading manufacturers of DRAM and NAND, will list American Depositary Receipts on Nasdaq, issuing up to 17.8 million new shares to raise around $29.6 billion at $166 per share. The offering is slated to be the largest ADR debut in Nasdaq history, surpassing both Alibaba's 2014 listing and Saudi Aramco's 2019 IPO — though it still falls well short of the recently concluded, record-breaking SpaceX IPO, which remains the largest IPO raise to date.

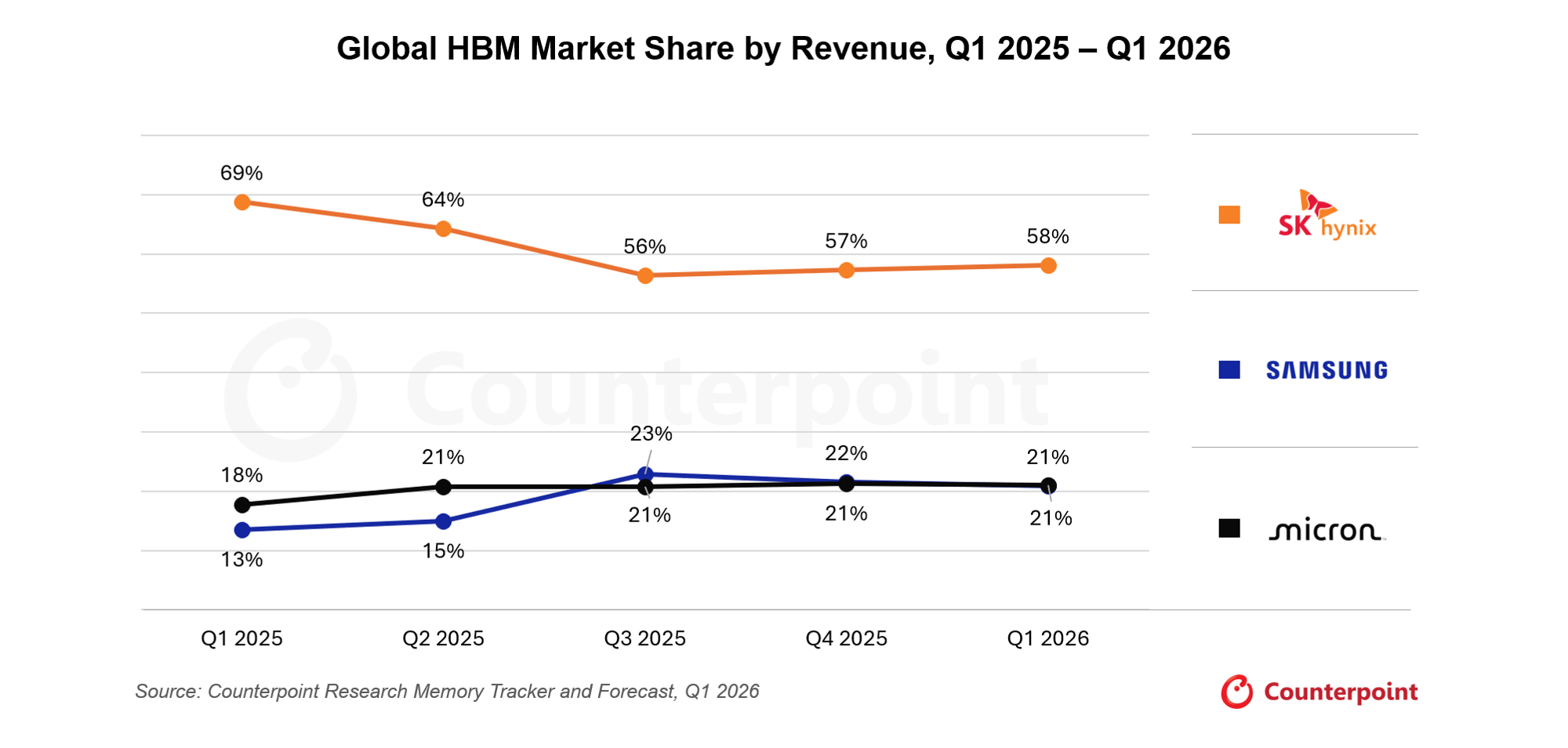

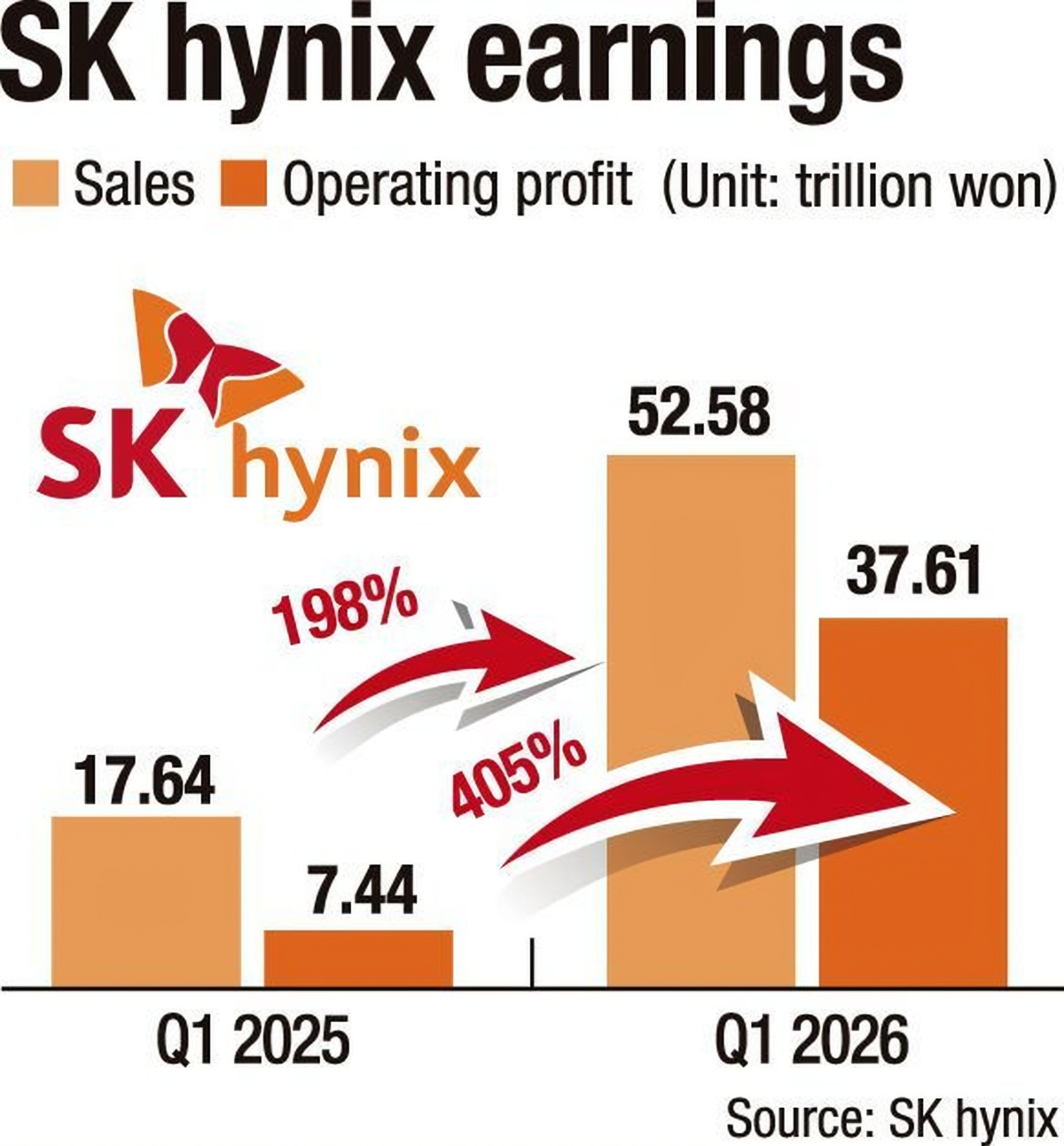

The timing is no accident. SK Hynix is up more than 300% this year, carries a $1.2 trillion market cap, and has just dethroned Samsung as South Korea's most valuable company for the first time this century. It is now the leading supplier of high-bandwidth memory (HBM), counting Nvidia and Google among its key clients, and by 2025 it had captured roughly 58% of the global HBM market — a comfortable lead over Samsung and Micron. Its Q1 operating margin of 72% was the product of a perfect storm: soaring AI demand colliding with a structural shortage of memory components, as hyperscalers and data centers aggressively reallocated capex toward memory.

That backdrop frames the question the listing really poses. Is this a move to recoil from the long-standing "Korea discount," or a bid to take the fight to Micron?

Shifting Away from the Korea Discount?

It wouldn't be a stretch to say the listing is designed to kill the Korea discount, with management targeting a valuation alongside Micron's. The funds raised will also help expand fabrication capacity and acquire critical manufacturing equipment from ASML.

According to HSBC, SK Hynix's valuation could rise 20% following the Nasdaq listing, narrowing a gap with Micron that has persisted for years — the US rival has traded at an average 35% premium to SK Hynix over the last 13 years. HSBC attributes that gap largely to Micron's access to a wider US investor base and its shareholder-friendly policies, and it has revised Hynix's price target to 4 million won from 2.9 million won, citing the listing as a key catalyst. Eugene Asset Management and Jupiter Asset Management strike a similar note, projecting up to 30% upside.

Micron Gets a Pure-Play Rival

The re-rating story has a flip side, though. It is not only about Hynix climbing toward Micron's multiple — it is about why Micron was elevated in the first place.

For more than a decade, Micron enjoyed a singular position: the only liquid, US-listed pure-play on AI memory. Any investor who wanted exposure to HBM had eyes only for Micron — a scarcity that helped the stock surge over 325% year-to-date and 854% over the last 12 months, backed by gross margins of roughly 81% in fiscal Q2.

But that premium is essentially a scarcity premium, and it is exactly the kind of advantage that evaporates once Hynix lists. A second pure-play removes the reason investors had to pay up for the only one available.

Looking Beyond the 72% Operating Margin

Both bull cases rest on margins holding, which raises the key question: is SK Hynix's 72% operating margin a level or a peak? At $166, the ADR is priced at roughly 8 to 9x forward earnings — a number that sits comfortably on top of memory's most aggressive up-cycle, with DRAM pricing expected to climb as much as 300% through 2027 and margins forecast to keep rising until the fourth quarter of that year.

Meanwhile, the company has slowed down on its HBM4 expansion to focus on the DRAM windfall. The decision to recalibrate its strategy is down to pragmatic profit taking, with the general DRAM segment seen as more lucrative than the HBM. Due to immense demand, the company has already sold out its HBM production capacity for 2026, thus confirming that aggressive expansion is unlikely to yield additional revenue.

Will SK Hynix's HBM Market Share Cross 70% by Q4 2026?

Following Up on TSMC Principles?

It's no surprise that parallels are being drawn to TSMC's ADR. The bull case leans on a tidy precedent: a foreign chipmaker lists in the US and ends up valued like a US company. TSMC's ADR has long traded at a durable premium to its Taipei-listed shares, at a multiple US investors are happy to pay.

But TSMC's premium has nothing to do with where it is listed and everything to do with what it is. The company trades at a premium because its moat — a near-monopoly over the foundry market and the pricing power that comes with it — justifies one. The premium wasn't created by the ADR; it was created by the business. Listing location alone doesn't manufacture a re-rating.

The Dilution Risk – If It’s a Risk

Issuing up to 17.8 million new shares does mean dilution, but it amounts to only around 2.5% of the company's issued and paid-up share capital. For a company worth more than $1.2 trillion, parting with 2.5% to raise around $29.6 billion is hardly a foreboding number — particularly when, as noted, the proceeds are already earmarked for capital expenditure. In effect, existing holders are giving up 2.5% of the company in exchange for HBM economics that could deliver greater returns.

The dilution is also a transfer of marginal ownership from Hynix's home-listed base to the US, with the aim of building the US institutional ownership that could finally close the Korea discount.

The Real Test

The Korea discount is often described as a venue problem with a venue fix. But the more important reality is that SK Hynix is a cyclical priced at peak margins — which is why the Micron–Hynix spread is the metric to watch once the ADRs begin trading.

That is also where the two questions in the headline collapse into one. If the spread closes because Micron declines rather than because Hynix surges, the market won't have re-rated Hynix up toward Micron; it will have de-rated the entire AI-memory premium, confirming its ceiling.