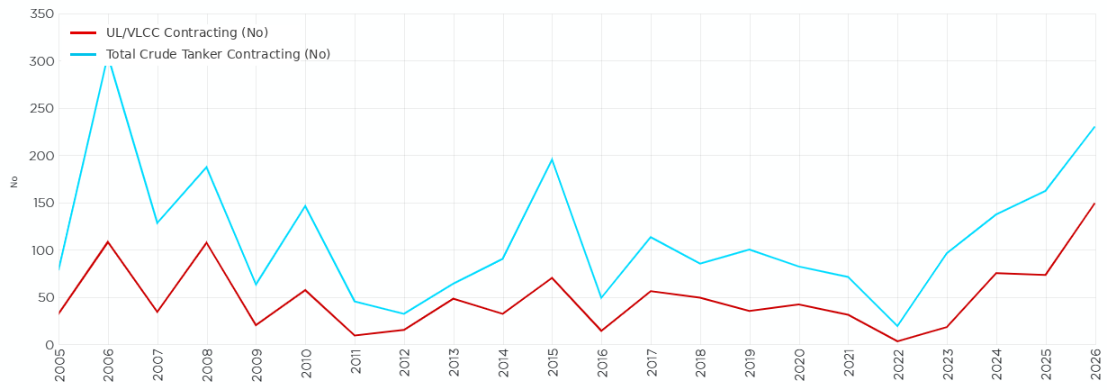

VLCC contracting has moved from a relatively subdued market into the strongest ordering wave of the past decade. Global annual contracting averaged about 31 vessels between 2016 and 2023, before rising to 75 in 2024 and 73 in 2025. By 21 July 2026, 149 VLCCs had already been contracted—more than twice the total for the whole of 2025. Owners and financial investors are therefore competing for modern capacity scheduled for delivery toward the end of the decade.

JPMorgan is one of the most prominent entrants in this ordering wave. South Korea’s Hanwha Ocean recently disclosed a approximately $262 million contract with an unidentified North American shipping company for two 320,000-dwt VLCCs, scheduled for delivery by March 2030. JPMorgan is being identified as the shipowner behind the order.

The Hanwha order would take JPMorgan’s reported VLCC programme to ten vessels. The other eight are being built in China for delivery in 2029.

The ordering wave has been accompanied by persistently high newbuilding prices. JPMorgan is paying near the upper end of the current VLCC price cycle for each of its ten vessels. The two Hanwha Ocean ships are the most expensive ($131 million each), compared with an average contract value of about $122 million for VLCCs ordered globally in 2026. JPMorgan is therefore committing capital when both ordering and prices are elevated—not at the bottom of the cycle. The investment case turns on two separate questions: why VLCCs are suited to the changing crude trade, and why it may still be rational to order them now.

Why VLCC?

Crude is travelling farther

Tanker demand is measured in tonne-miles—the volume of cargo multiplied by voyage distance. The recent uplift has been driven more by longer routes than by higher cargo volumes.

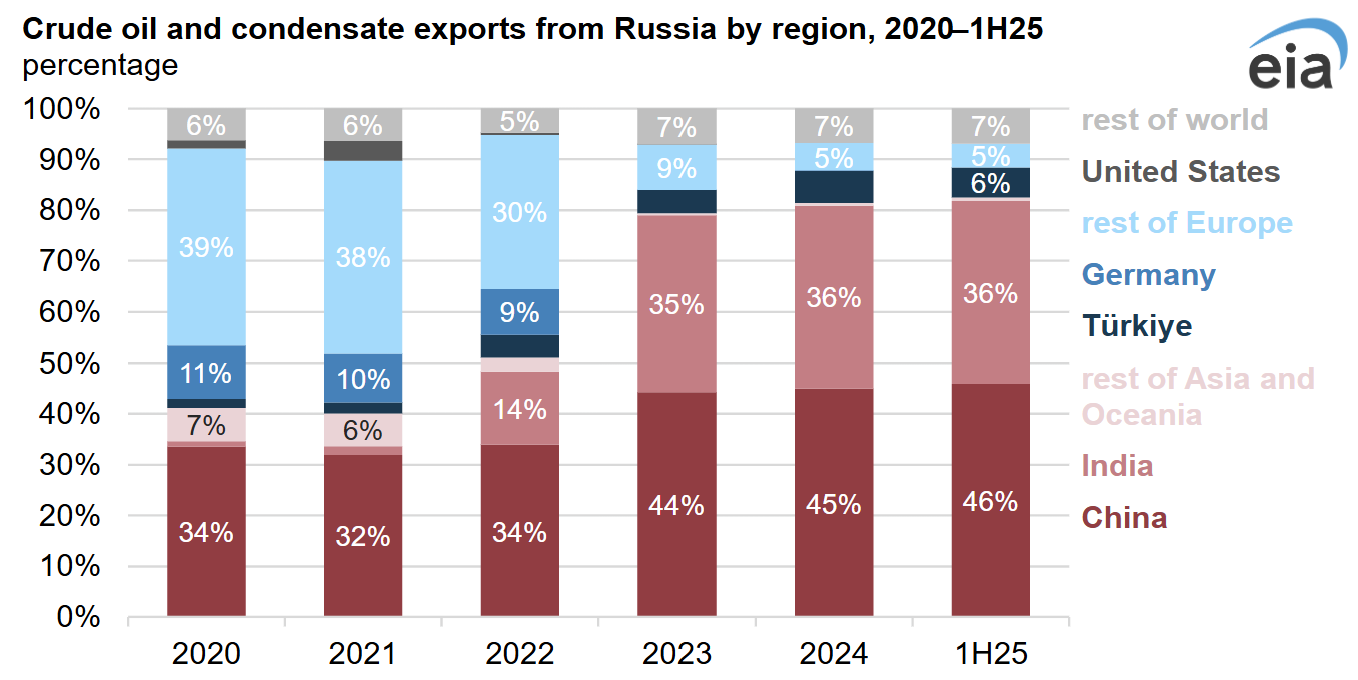

Russia’s invasion of Ukraine in 2022 produced one structural shift in crude trade. Europe’s share of Russian crude and condensate exports fell from 51% in 2020 to 11% in the first half of 2025, while Asia’s share rose from 41% to 81%.

Russian barrels that moved to nearby European ports now travel mainly to India and China. Europe, in turn, imports replacements from the Americas, Africa and the Middle East. A Baltic–India voyage can take roughly six times as long as a Baltic–Northwest Europe voyage.

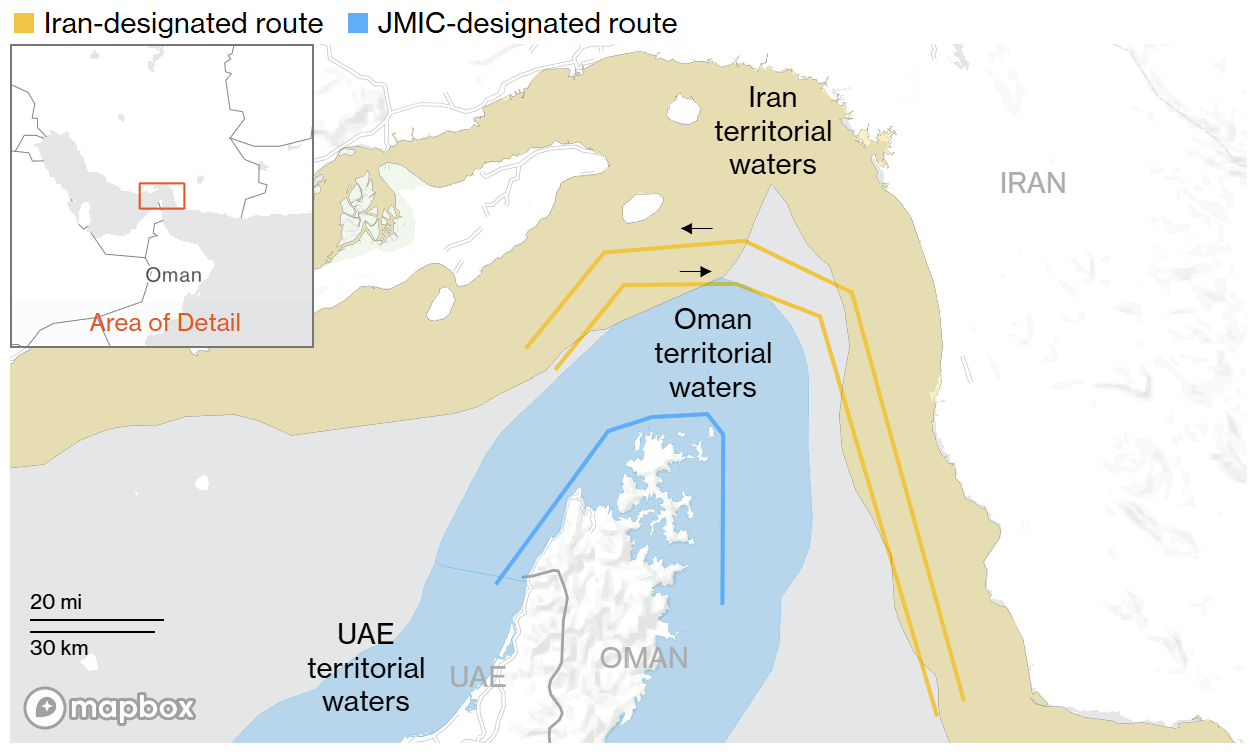

Attacks in the Red Sea added further distance by prompting vessels to avoid the Suez Canal. Rerouting via the Cape of Good Hope adds about 15 days to an Arabian Sea–Europe voyage.

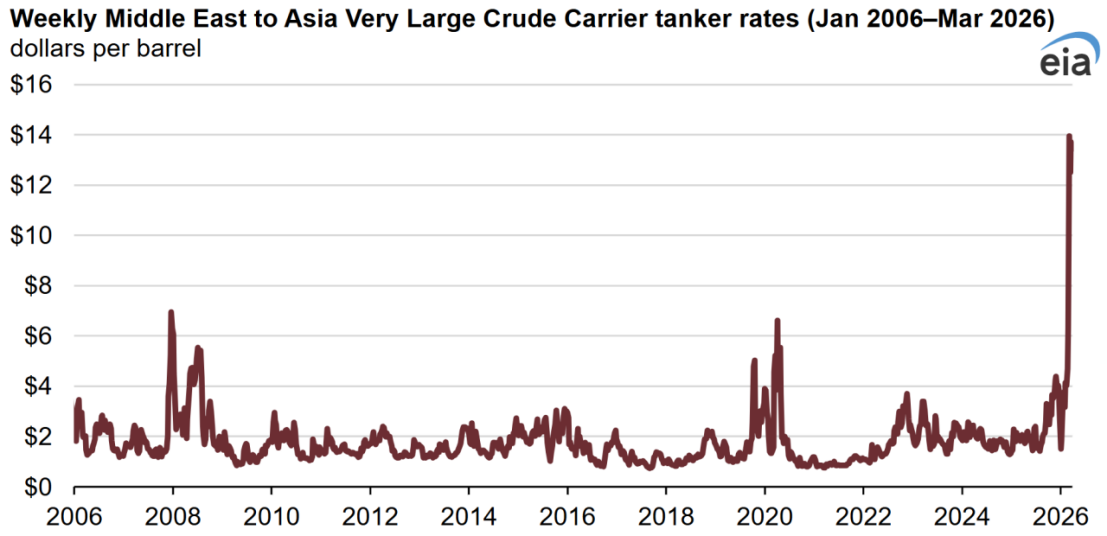

The 2026 Gulf conflict had an outsized impact on the VLCC market. The Arabian Gulf is one of its principal loading regions. Gulf export terminals generate large, regular cargoes, while Gulf–Asia is both a core VLCC trade and a key freight benchmark.

The effective closure of the Strait of Hormuz pushed Middle East–Asia VLCC rates to their highest level since 2005.

Asia had to replace disrupted supplies with barrels from more distant producers. Atlantic Basin crude exports—primarily bound for markets east of Suez—increased by 3.5 million b/d between February and May, led by suppliers including the United States, Brazil and Canada. US crude exports reached a record 5.6 million b/d in April, 21% above the previous monthly record.

This shift increased tanker demand even without a comparable rise in global oil consumption. Crude that would normally have travelled from the Gulf to Asia was increasingly replaced by cargoes moving from the Atlantic Basin, substantially extending average voyage distances.

The combination of higher Atlantic Basin exports and longer voyages to Asia therefore raised tonne-mile demand and strengthened demand for VLCCs, the most economical vessels for transporting large crude cargoes over long distances. A VLCC carries about 2 million barrels—roughly twice a Suezmax cargo—and offers the lowest transport cost per barrel on large, long-haul trades. Major export terminals in the US Gulf, Brazil and West Africa can accommodate these vessels.

The Gulf Remains the Structural Core of the VLCC Market

The Arabian Gulf remains one of the world’s largest crude-export systems and holds most of the world’s spare production capacity. Flows through the Strait of Hormuz remained broadly around 20 million barrels per day from 2018 through early 2025 despite repeated geopolitical tensions. In 2024, the strait carried more than one-quarter of global seaborne oil trade, while about 84% of its crude and condensate flows went to Asian markets.

The market can reasonably view the Hormuz disruption as severe but potentially reversible. A prolonged closure would damage Gulf producers as well as importers, while pipelines can replace only a fraction of normal flows. Historically, repeated threats and attacks did not result in a permanent closure.

Russian sanctions appear more persistent. Enforcement has expanded beyond cargoes to vessels, managers, insurers and maritime services. The EU has extended its economic sanctions to July 2027, with little indication of an imminent return to the pre-2022 trading system.

Gulf cargo flows may recover, but the division between compliant and sanctioned VLCC capacity is likely to persist.

Will Asian refiners become less dependent on Middle Eastern crude after the Hormuz disruption?

Why Now?

A five-year-old VLCC was valued at about $138 million, $9 million above the average newbuilding price of $129 million in 2026. Buying a secondhand vessel at that premium is a bet that today’s high freight rates will continue. Ordering new vessels is a bet that compliant VLCC capacity will remain scarce later in the decade.

Regulation is accelerating fleet renewal

The IMO’s EEXI and CII requirements became mandatory in 2023. EEXI measures a vessel’s technical efficiency, while CII assigns an annual operational carbon-intensity rating. Ships rated E, or D for three consecutive years, must submit corrective-action plans. Compliance can involve engine-power limitations, slower sailing, operational optimisation or technical upgrades.

These measures disproportionately affect older VLCCs, which generally consume more fuel and emit more carbon per tonne-mile.

They may not automatically forced into demolition: high freight rates can justify retrofits or slower operation. But both options carry an economic cost. Retrofitting requires capital, while slow steaming reduces annual carrying capacity by keeping the vessel occupied for longer. Newer ships therefore gain an advantage through lower fuel consumption, stronger CII performance and broader acceptance among charterers and financiers.

The shadow fleet inflates headline supply

Sanctions on Russian, Iranian and Venezuelan oil have created a parallel transportation market: the shadow fleet. Its vessels typically have opaque ownership, uncertain insurance, frequent flag or manager changes, irregular AIS activity and complex ship-to-ship transfers. They can still carry crude but are less acceptable to mainstream charterers, banks, insurers and terminals.

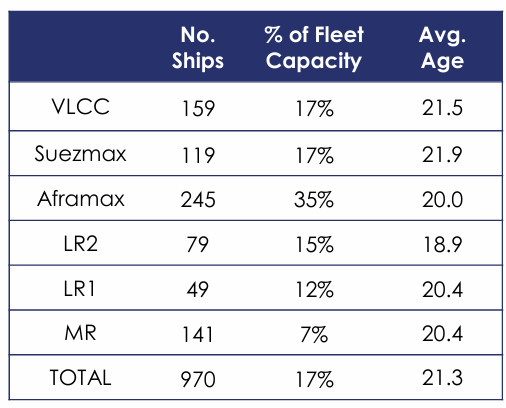

The shadow fleet now represents a material share of nominal supply. S&P Global estimated in July 2026 that tankers associated with shadow-fleet activity accounted for about 22% of the global fleet. Analyze classified 17% of VLCCs and 35% of Aframaxes as part of the dark fleet in the second quarter. The higher Aframax share reflects Russia’s Baltic and Black Sea trades, while shadow VLCCs are more closely linked to Iran and long-haul Asian routes.

Age will tighten effective supply further. Sanctioned VLCCs averaged 21.5 years in 2026, compared with about 14 years for the overall tanker fleet. VLCCs typically enter their economic retirement window at 20–22 years, although shadow demand can extend operations toward 25 years. Rising survey, repair and insurance costs should increase retirement pressure toward the end of the decade.

The result is a two-tier market. Shadow vessels inflate headline capacity but contribute less to the pool available to mainstream cargo owners. The relevant constraint is therefore not the total number of VLCCs, but the number that remain compliant, properly insured and commercially acceptable.

Shipyard capacity makes waiting costly

A further reason to order now is physical capacity. VLCC construction is concentrated among a limited group of Asian shipyards with the dock space, engineering experience and quality record required to build large crude tankers. The same yards also compete for LNG carriers, container ships and other high-value projects.

As their orderbooks fill, available VLCC delivery slots move further into the future. For an investor that expects to need modern tonnage near the end of the decade, delaying the contracting decision by one year may not simply mean ordering the same ship one year later. It may mean accepting delivery several years later, selecting a less-preferred yard or paying more for the remaining capacity.

The Risks

Old VLCCs may remain in service longer than expected

The central supply assumption behind the newbuilding cycle is that a meaningful number of older vessels will leave mainstream trading as new ships arrive. Yet fleet age indicates only scrapping potential, not actual scrapping.

The shadow market creates the opposite effect from the one described in the investment case. It reduces the pool of vessels acceptable to mainstream charterers, but it also provides an alternative buyer for ageing VLCCs that might otherwise be recycled. A sale into sanctioned trading changes the vessel’s commercial market without removing its physical capacity.

Delays or flexibility in emissions regulation can extend the viable life of older vessels. The IMO Net-Zero Framework, which would introduce a global marine-fuel standard and greenhouse-gas pricing mechanism, was approved in draft form in April 2025. If carbon pricing and fuel-intensity requirements are implemented more slowly than expected, owners may postpone both retrofits and demolition.

The marine-fuel transition creates stranded-asset risk

A VLCC delivered in 2030 may remain in service into the 2050s. Its commercial life will therefore extend well beyond the period for which marine-fuel regulations and technology are currently visible.

The first risk is technological lock-in. LNG, methanol, ammonia, biofuels, synthetic fuels and onboard carbon capture are all being considered, but no clear VLCC standard has emerged. A conventional vessel ordered today could face expensive retrofits, reduced cargo space or limited access to low-carbon fuel.

The second risk is regulatory cost. The IMO Net-Zero Framework has been delayed, leaving carbon prices, fuel-intensity thresholds and implementation dates uncertain. If stricter rules are later introduced quickly, however, conventionally fuelled newbuildings could face higher fuel costs, carbon charges or premature modification. Regulation can therefore hurt the investment in either direction: slow implementation extends competing supply, while rapid implementation raises compliance cost.