Hours before the Bank of England(BoE) published its July Financial Stability Report, we framed the leverage rule debate around three possible outcomes.

The first was a full exemption for gilts from the leverage calculation, which is the most aggressive and market-friendly option. The second was a narrower technical adjustment that would give banks more balance sheet flexibility without dismantling the broader safeguard. The third was no meaningful easing at all.

The Bank has now answered.

The outcome landed closest to option two.

The BoE did move to ease leverage constrains, but not through the full gilt exemption that banks had been discussing before the report. Instead, the Financial Policy Committee and Prudential Regulation Authority plan to consult on a broader redesign of the leverage framework.

What the BoE actually proposed

The package has three main elements.

The Bank plans to remove the Countercyclical Leverage Buffer from leverage requirements; change the calibration of the Additional Leverage Ratio Buffer for systemically important firms; make the framework more releasable during stress. It also proposes reducing the Tier 1 leverage minimum from 3.25% to 3%, while introducing a 25 basis point general leverage buffer. (Page 118 of the report)

Overall, the BoE estimated large UK banks subject to the regime would need to maintain leverage ratios around 20 basis points lower in aggregate, although the impact would vary by bank. Reuters(July 7) noted that the current framework has become binding for three of seven major British banks.

That is easing but it's not the same as removing gilts from the leverage exposure measure.

Before the report, Reuters(July 6) highlighted industry arguments that a gilt exemption could directly expand banks’ capacity to hold UK government debt. Barclays estimated that such a move might enable banks to hold up to £150 billion more in gilts with potentially significant effects on government borrowing costs. Our pre-release News Flash identified that as the most aggressive scenario.

The BoE chose a different route.

Did the BoE go far enough in easing bank leverage rules?

The effect of gilt market is harder to predict now

This is where the subsequent story becomes more interesting than a simple “BoE loosens regulation” headline.

A full gilt exemption will create a relatively direct mechanism: holding more government bonds would no longer expand the relevant leverage exposure measure in the same way, which makes it easier for banks with limited balance sheet capacity to hold more gilts.

But the BoE’s actual plan does not specifically encourage banks to buy more gilts.

The requirement of lower aggregate leverage may still create additional balance sheet capacity. But it does not follow automatically that banks will use that capacity to buy gilts. They could deploy it across lending, market making or other assets instead. That means the large gilt demand estimates discussed before the report should not simply be transferred to the policy package the BoE actually proposed. This is an inference from the difference between the pre gilt exemption scenario and the published reform plan.

In other words, the Bank has loosened the constraint without directly dictating where the newly available capacity goes.

There is also a deeper contradiction inside the report

While easing the leverage pressure on banks, the BoE is also warning of leverage risks in other areas of the financial system.

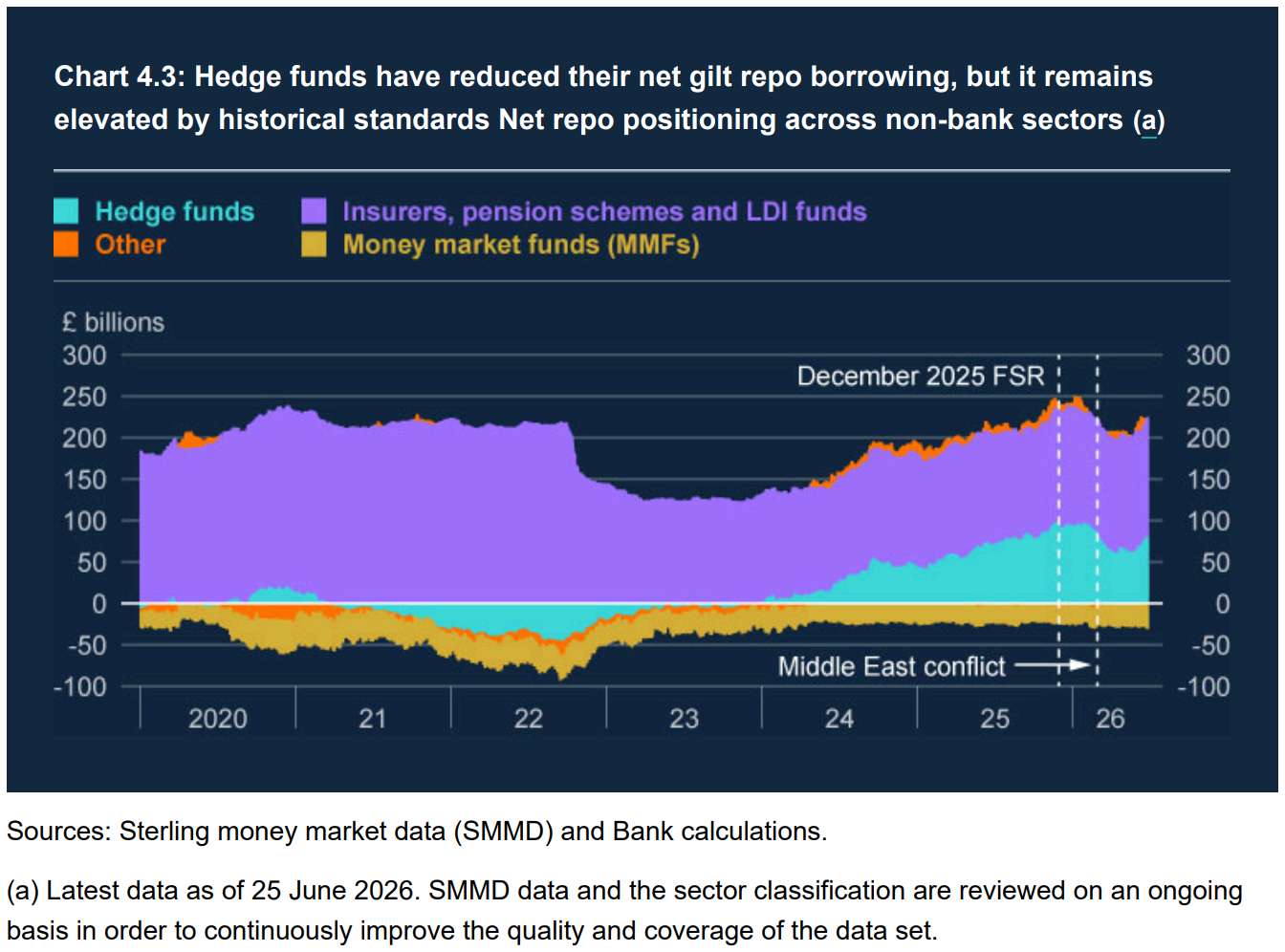

The report says net hedge fund borrowing in the gilt repo market fell roughly 40% from £100 billion by mid-April, but then rose again to around £85 billion from the end of May. The BoE says those positions remain elevated by historical standards and are still heavily associated with leveraged relative value strategies.

That tension did not escape from the notice of policymakers. Reuters(July 7) reported that some FPC members worried the proposed leverage changes could contribute to an unwanted increase in market based leverage, with implications for the resilience of core UK markets.

So the real policy question has changed. Before the report, it was: Will the BoE loosen leverage rules? Now the more important question is: Can the BoE give banks more room to operate without adding to the leverage risks already building in the gilt market?

The Bank itself has not treated that question as settled. It says further analysis will examine whether the proposed reforms create financial stability gaps, including their interaction with gilt repo resilience and market functioning. That work is due to be considered at the FPC’s Q3 meeting, ahead of any potential consultation on this part of the package.

What is the most likely next step in the BoE’s leverage reform?

The first prediction has now been answered: the BoE was prepared to move.

But it chose the middle path: easing leverage requirements while keeping the broader backstop intact.

The next prediction is harder: whether the BoE’s current plan will remain unchanged once it completes its review of wider gilt market risks.

Source:

- Bank of Englan: Financial Stability Report, July, 2026 https://www.bankofengland.co.uk/-/media/boe/files/financial-stability-report/2026/financial-stability-report-july-2026.pdf

- Bank of England sets out plan to ease bank leverage rules, July 7, 2026 https://www.reuters.com/business/finance/bank-england-sets-out-plan-ease-bank-leverage-rules-2026-07-07/