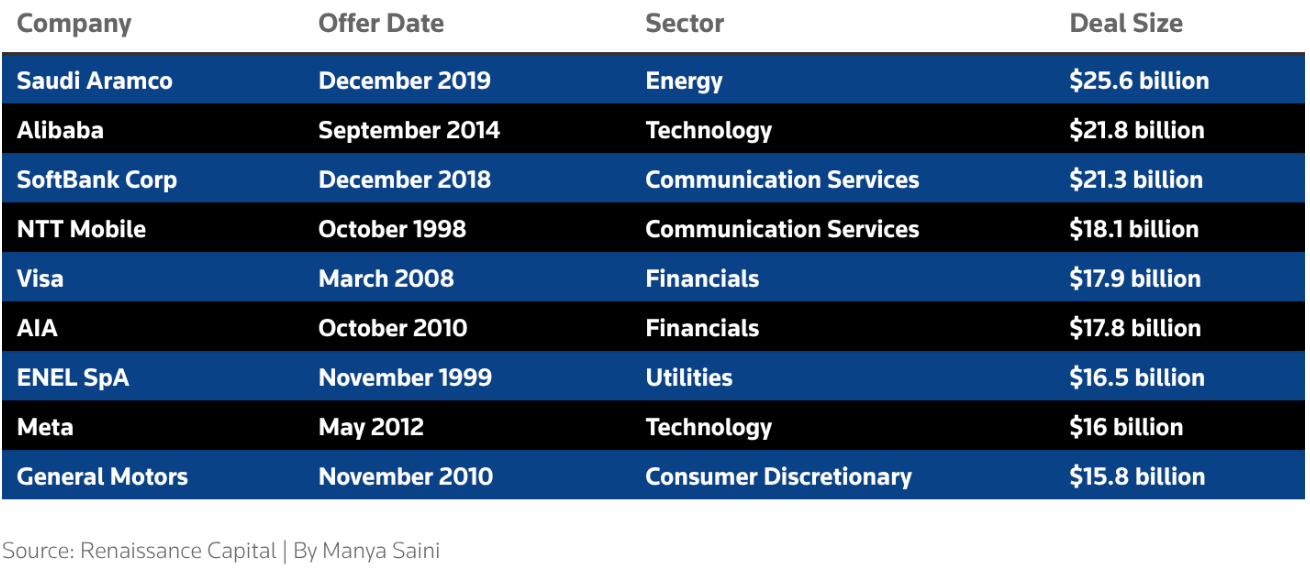

SpaceX is slated for its initial public offering in June, with the IPO expected to be the largest ever in history, crossing the Aramco IPO which was priced at $1.7 trillion.

SpaceX is now targeting a valuation of at least $1.7 trillion with the latest Polymarket predictions pricing the IPO to be closer to the $2.5 trillion mark.

The IPO numbers are a sight to behold – a fixed price of $135 per share for 555.6 million shares and a target to raise around $75 billion, according to Reuters reports.

Table 1: Largest U.S. IPO deals in history (Renaissance Capital sorted)

Meanwhile, 30% of the float has been reserved for retail investors, with Elon Musk expecting to walk away with around 82% of the voting power.

On the surface, the SpaceX IPO promises to be a crucial catalyst for the entire space industry, with its listing validating the varying paths other listed companies in the sector have taken.

And you can’t really argue against that as we approach June 12, the date when the stock begins trading.

Since SpaceX IPO reports surfaced back in March, space stocks have experienced an unprecedented rally. Rocket Lab’s stock has surged nearly 72% year-to-date, AST SpaceMobile is up over 47%, while carrying a market cap of $41 billion, while booking under $15 million in quarterly revenue, missing estimates by 60%.

Similarly, Stellogic is up over 335% YTD. It is a similar story across other stocks such as Intuitive Machines, Firefly Aerospace, York Space Systems and Planet Labs.

However, if we look at this closely, none of these stocks’ surge is driven by strong earnings.

These stocks appear to be flying high because investors who craved exposure to the SpaceX IPO story had no way to own the stock and decided to put their money in the closest alternatives.

That logic however, expires on June 12.

This is when as an investor, you would no longer need a SpaceX alternative when you can buy the stock.

A $75 Billion Raise

SpaceX is targeting to raise $75 billion upon IPO and has option for another $11 billion – making it the largest equity drain in the sector’s history.

SpaceX is likely to be the key stock that every institutional fund would want to get their hands on for space exposure.

This could have an impact on stocks such as Rocket Lab and AST SpaceMobile whose slice of the money is likely to be chased by SpaceX.

On top of that, Nasdaq’s expedited entry rules will make the company of SpaceX’s size eligible for the Nasdaq-100 after a 15-day period.

It is safe to say that SpaceX is not just a company that is competing for capital – it is a company that competes through its product line. The company’s S-1 already named Rocket Lab as a competitor and will be looking to diversify into medium-lift payload.

Until the IPO, AST SpaceMobile could trade at around 100 times estimated forward sales only because of the absence of a publicly-listed pure-play stock to keep a leash on it. Following SpaceX’s IPO, we can expect this metric to be contained.

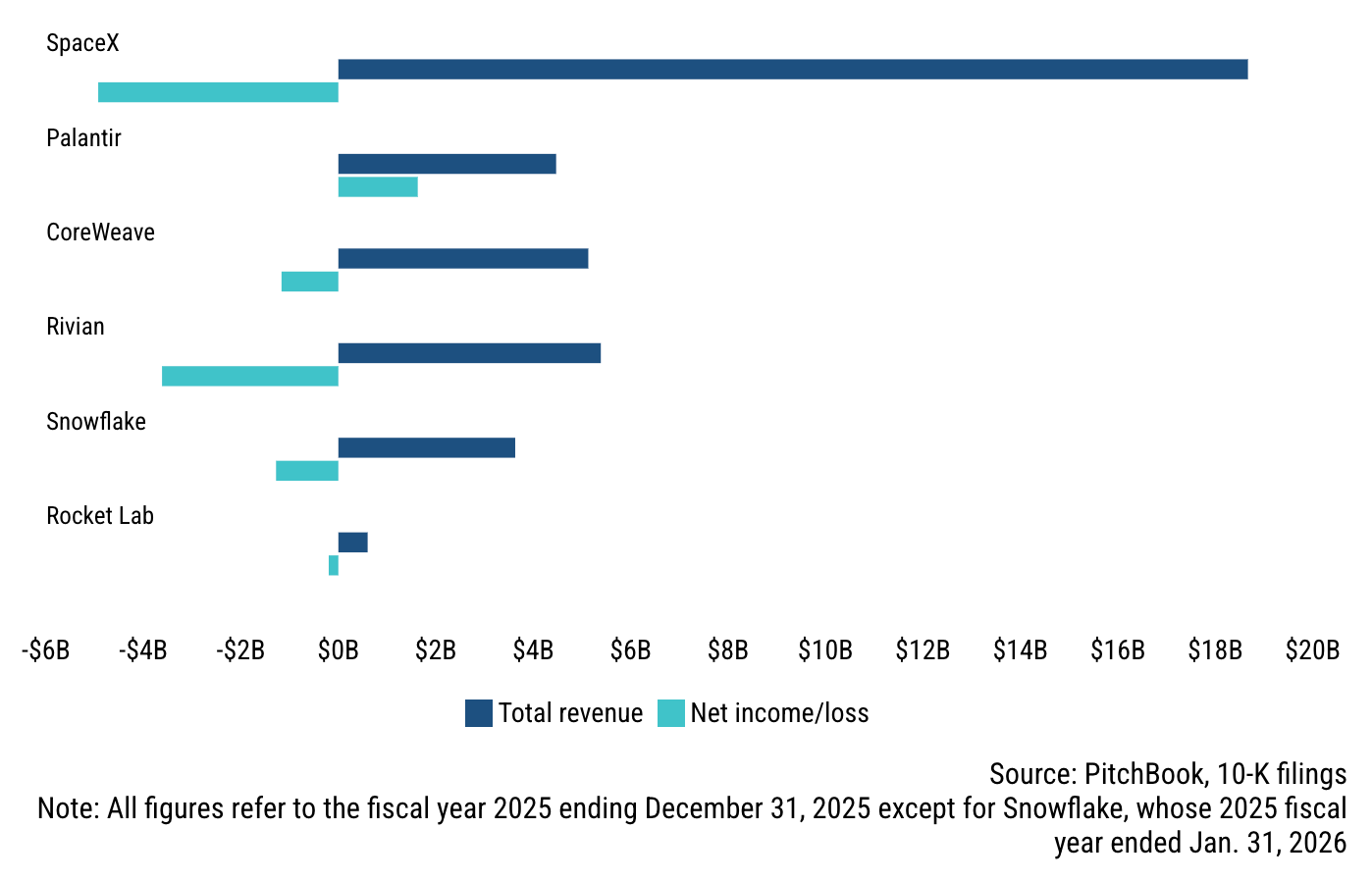

Figure 1: Financial Performance of Peers (Morningstar sorted)

How are Prediction Markets Seeing the IPO Event?

One of the best ways to assess the SpaceX IPO event and its fallout is by gauging Polymarket traders sentiment.

Over 99% traders expect the IPO to close above $1.2 trillion, while 70% expect it to close over $2 trillion.

Meanwhile, a wide majority of traders expect the company’s market cap to cross $1.6 trillion by the end of June.

Embedded JavaScriptEmbedded iFrameWill SpaceX's market cap be less than $1.0T at market close on IPO day?

Yes 0% · No 100%

View full market & trade on Polymarket

The numbers are telling and validate the IPO mechanics. Rather than going for a conventional price range, SpaceX has gone for a fixed share price. Musk will be selling zero shares, thus constricting supply with expected frenzied demand of the stock.

To date, investor focus on prediction markets is on SpaceX, which means that a lot of industry peers are quietly going through a de-rating event after initially benefitting from the IPO announcement.

Will SpaceX Cross $2 Trillion In Market Cap in 2026?

All Eyes to Remain on SpaceX

One cannot deny that SpaceX IPO is going to be a key driver for the space economy. The World Economic Forum has already forecasted the sector to reach $1.8 trillion by 2035. SpaceX becoming a publicly-listed company further legitimizes the projections.

However, the WEF report, when studied in detail, focuses on growth areas that a lot of SpaceX peers aren’t venturing into yet.

Around 60% of space industry expansion will come from segments such as logistics, agriculture, insurance and defense data and not launchers and satellite – two segments that a lot of listed space stocks call their bread and butter.

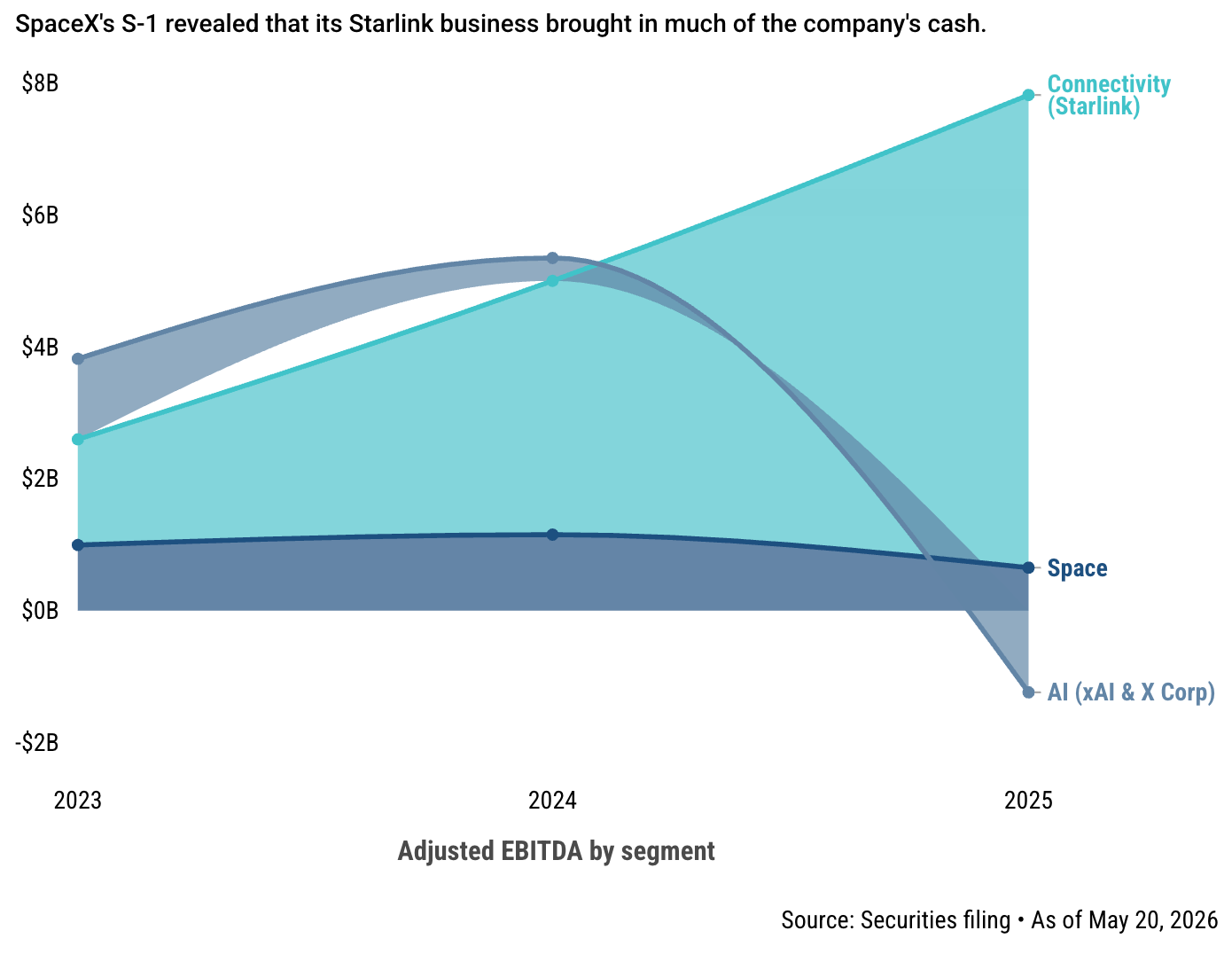

The same can be said about SpaceX whose only profitable segment is Connectivity through Starlink, which posted a quarterly profit of $1.19 billion.

Space launch segment on the other hand, booked a loss of $619 million.

SpaceX has been tagged as a satellite-broadband-and-AI company which also owns the best rocket technology in the world. And this is the dangling carrot that investors are chasing.

What also needs to be analyzed is that the company booked $4.94 billion GAAP net loss in 2025, capital expenditure of $10.1 billion in a single quarter and a $41.3 billion accumulated deficit.

A company with a potential market cap of $1.77 trillion cannot afford execution shortcomings on projects such as Starship, Starlink or burning cash on AI.

Figure 2: SpaceX Adjusted EBITDA by Segment (Morningstar sorted)

A Sum-of-Its-Parts Valuation

Taking away the glamor and spectacle that we’ve come to see from anything carried out by Musk, SpaceX is promoting itself as a potential $1.77 trillion company which relies on three distinctly different businesses, thus making the valuation a sum of its parts.

Connectivity is expected to remain the best performing segment and helps justify the current valuation, especially if Starship continues to refine its tech stack.

The launch business on the other hand, appears to be more of a strategic presence rather than a profit making tool.

Meanwhile, the company is burning cash on its AI unit, which means that in the long run, SpaceX will either “normalize” as either a highly niche space innovation company or an AI company with several space-related clusters with long-term strategic goals.

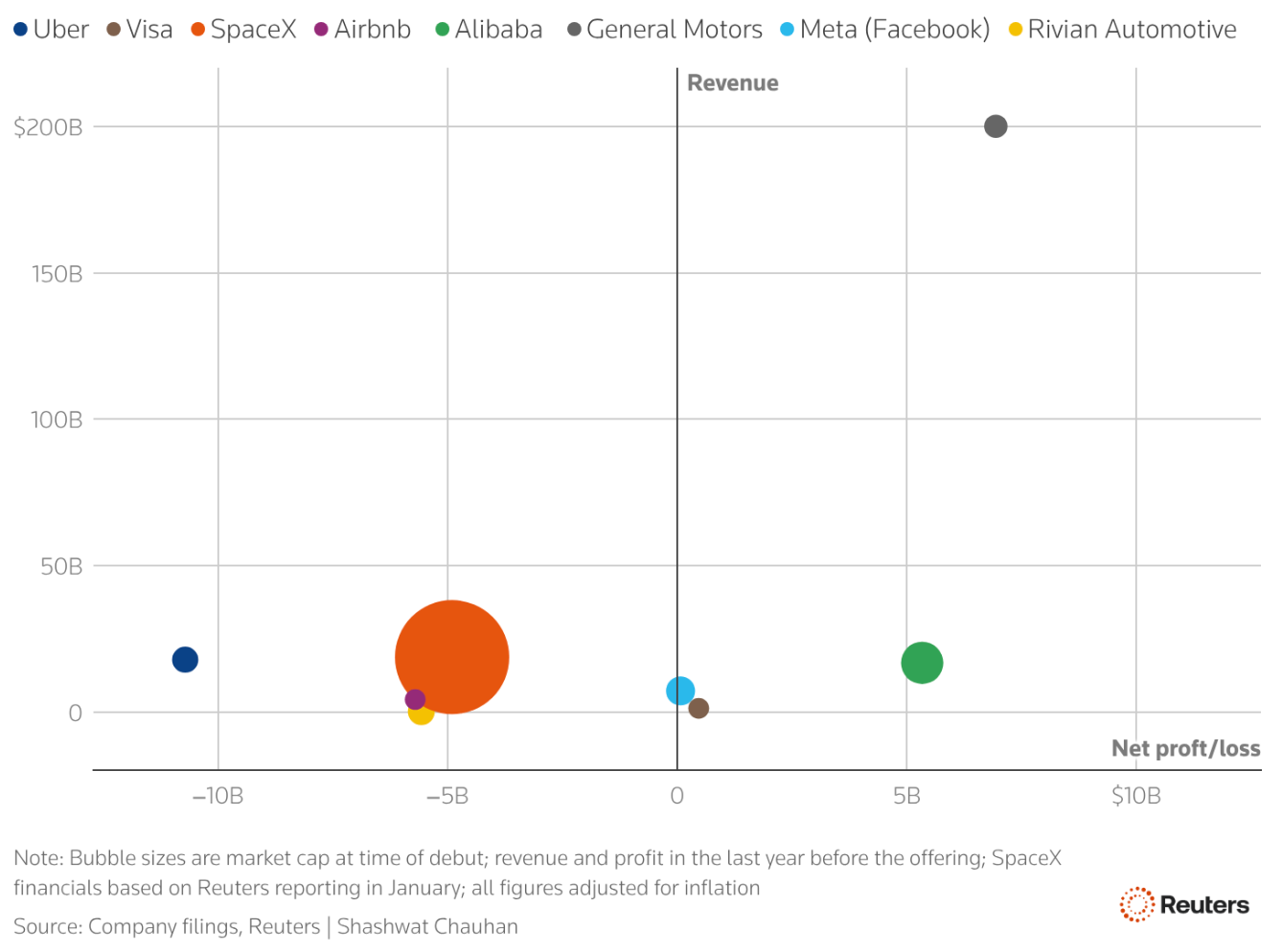

Figure 3: Valuation of Major Offering on Record (Reuters sorted)

The Liquidity Siphon Effect

Naturally, the $75 billion fund raising target seems like an apocalyptic scenario for its peers. However, this amount represents only a fraction of the total US money-market funds which is about $7.89 trillion.

And while it may appear that the IPO could potentially impact other space stocks, we need to understand SpaceX as a business.

The company is very unusual if we look at it purely from a space industry point of view. It is a space stock, a satellite-broadband and telecommunications stock and it is also an AI-infrastructure stock following the xAI merger.

In the US, IPO funds are mostly raised from institutional investors and large brokerages through the recalibration of existing equity and portfolio positions.

Therefore, upon its IPO, SpaceX will be siphoning the $75 billion from multiple sources – from space allocations to the telecom sector to the AI-infrastructure bucket, meaning that no single source is going to be drained.

However, one siphoning scenario that could unfold in the coming days could be the stock’s entry in the Nasdaq-100, which could result in several funds selling a slice of every niche stock they hold to acquire the SPCX stock.

This could expose several space stocks but the event would not be confined to them, with the likes of Nvidia, Microsoft, Alphabet and even Nebius, likely to be exposed.

SpaceX IPO – A Catalyst of Differentiation

June 12, the day when SpaceX IPO takes place, should be seen as a sorting mechanism, not just a cataclysmic event for the space industry.

While the IPO is definitely a catalyst, what it actually catalyzes is market differentiation.

In the first couple of weeks of the IPO, we could see SpaceX experiencing a rally, while other space stocks lose a chunk of their respective market caps.

By the end of the 15th day, the time when the company could be eligible for the Nasdaq-100 entry, we could see a weight dilution event with constituents shrinking their weight proportionally to make room for funds to add SPCX into their portfolios.

The largest constituents such as Nvidia, Apple, Microsoft, Alphabet and Amazon could be the key stocks in what is likely to be a modest dilution event, simply because they have the biggest positions.

A very crucial point to be mentioned here is that an index fund doesn’t buy a stock based on the company’s full size, it makes a buy based on float. SpaceX is only selling around $75 billion worth of stock, while the rest will be locked up by Musk and insiders.

Now Nasdaq’s rule explicitly cap the index weight at around 3x the float, not the market cap.

Since there will be very few shares trading at the start, index fund could struggle to find enough which could lead to a short-term increase in the stock price. Under Nasdaq-100 IPO lockup regulations, insiders are restricted from selling their shares for 180 days. Once the lockup period ends, insiders could start selling their shares, thus creating a secondary market distribution.

Therefore, it is safe to assume that the share buying will be spread out and not aggressive on day 15.

Will SpaceX Gain Entry into the Nasdaq-100 After Day 15 of its IPO?

On top of that, Nasdaq-100 will remain the only major index buying the SpaceX stock. The S&P 500 is closed for now because the company lost around $4.9 billion last year, making it unqualified.

The overall effect of the SpaceX IPO on the big stocks, based on our research, is likely to be small and mechanical. However, what should be looked at in the long run would be the company’s own share dynamics and how the smaller space stocks behave immediately and a while after the IPO.