Assembly, test, and the packaging revolution reshaping the back end

Executive summary

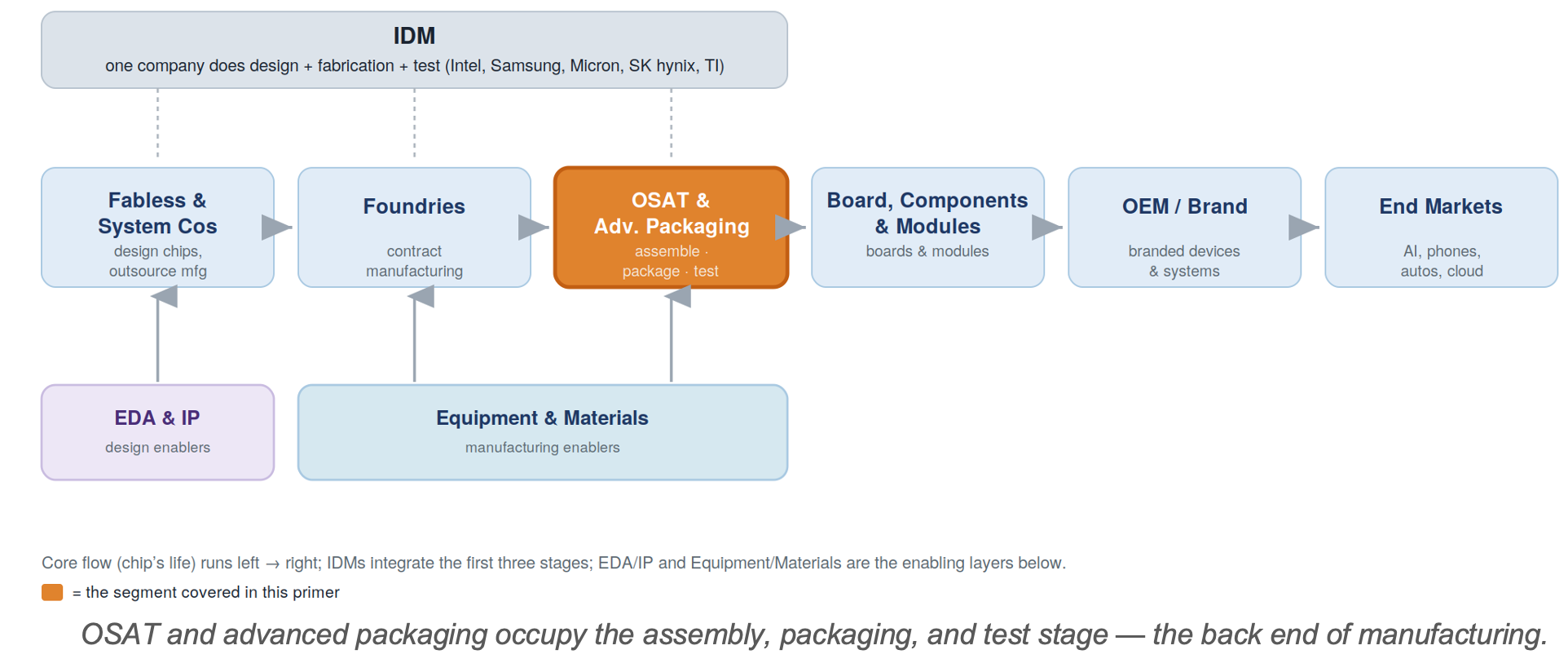

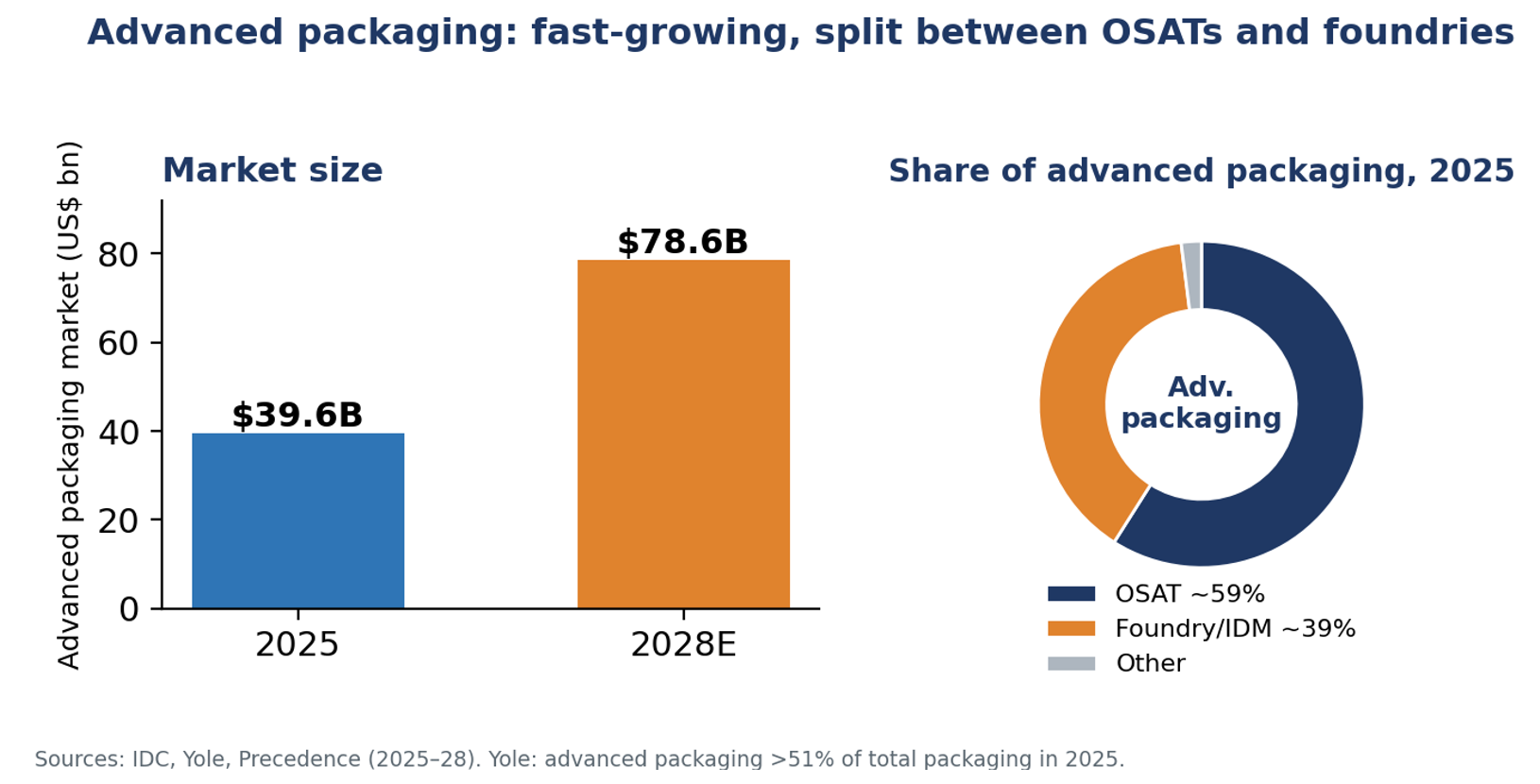

OSAT — outsourced semiconductor assembly and test — firms take finished wafers and turn them into packaged, tested chips. Historically the lowest-margin link in the chain, the back end has been transformed by advanced packaging: chiplets, 2.5D/3D stacking, hybrid bonding, and platforms like TSMC’s CoWoS that are essential to AI chips. The advanced-packaging market is growing from roughly $40 billion in 2025 toward ~$79 billion by 2028.

The competitive twist is that this lucrative new work is contested by three groups: the OSATs (ASE, Amkor, JCET), the foundries (TSMC), and the IDMs (Intel, Samsung). OSATs hold roughly 59% of advanced packaging and the foundry/IDM group about 39% — and the foundries are pushing in hard, because advanced packaging increasingly uses wafer-level, fab-style processes that blur the old front-end/back-end line.

1. Defining the sector and its strategic importance

After a wafer leaves the fab, it must be diced into individual dies, connected and protected within a package, and tested. OSATs provide these back-end services under contract, just as foundries provide front-end manufacturing. Once an afterthought, packaging is now a primary determinant of chip performance — which has turned the back end into a strategic battleground.

2. Position in the value chain

As noted in the Equipment primer, the OSAT service sits here in the chain, while the equipment used to perform it is upstream. Advanced packaging is now drawing front-end tools into the back end — the central structural shift in this segment.

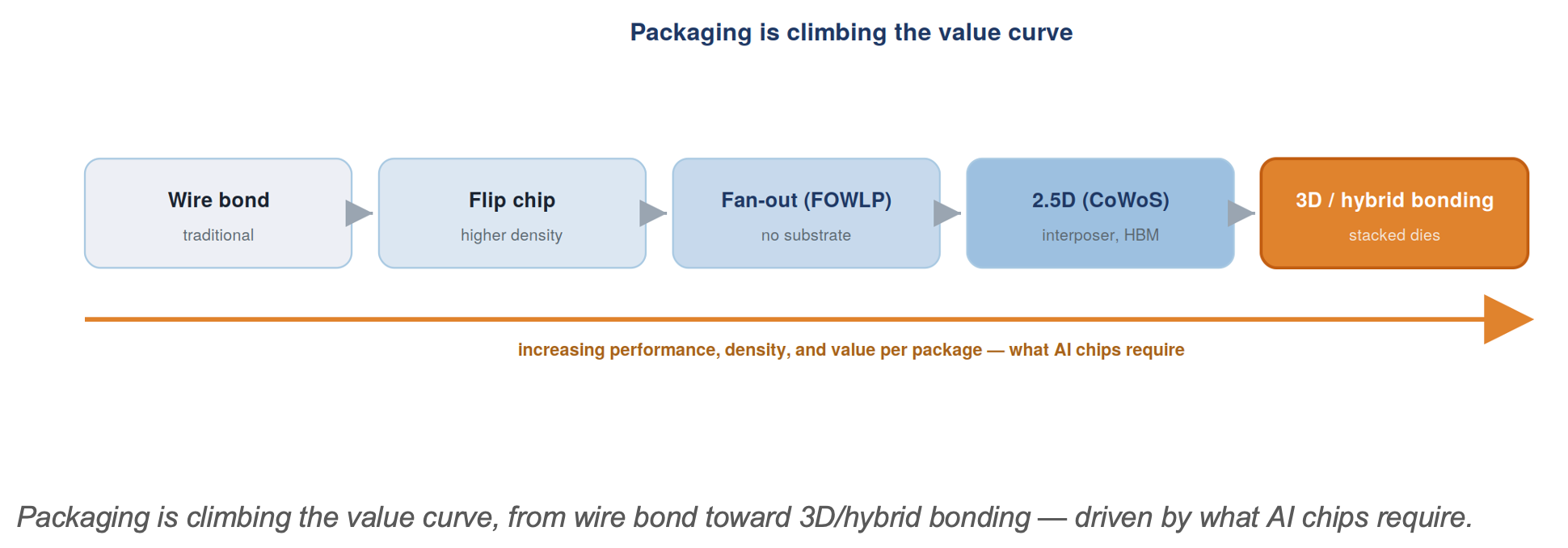

3. Structure: from traditional assembly to advanced packaging

Traditional OSAT. High-volume wire-bond and flip-chip assembly and test for the bulk of the world’s chips — a thin-margin, scale-and-cost business (Amkor’s gross margin runs around 15%, a world away from foundry economics).

Advanced packaging. The high-value frontier: 2.5D/3D integration, chiplets, fan-out, and hybrid bonding that connect multiple dies and stacked HBM into one high-performance package. This is what AI accelerators require, and by some estimates it surpassed traditional packaging as a majority of total packaging value in 2025.

The players. ASE is the world’s largest OSAT (with a large electronics-manufacturing arm alongside assembly/test); Amkor is second and JCET is China’s leader, followed by Powertech, TFME, and test specialists such as KYEC. But TSMC (CoWoS, SoIC), Samsung (I-Cube, X-Cube), and Intel (Foveros, EMIB) now perform much of the cutting-edge packaging themselves.

4. Market size and segmentation

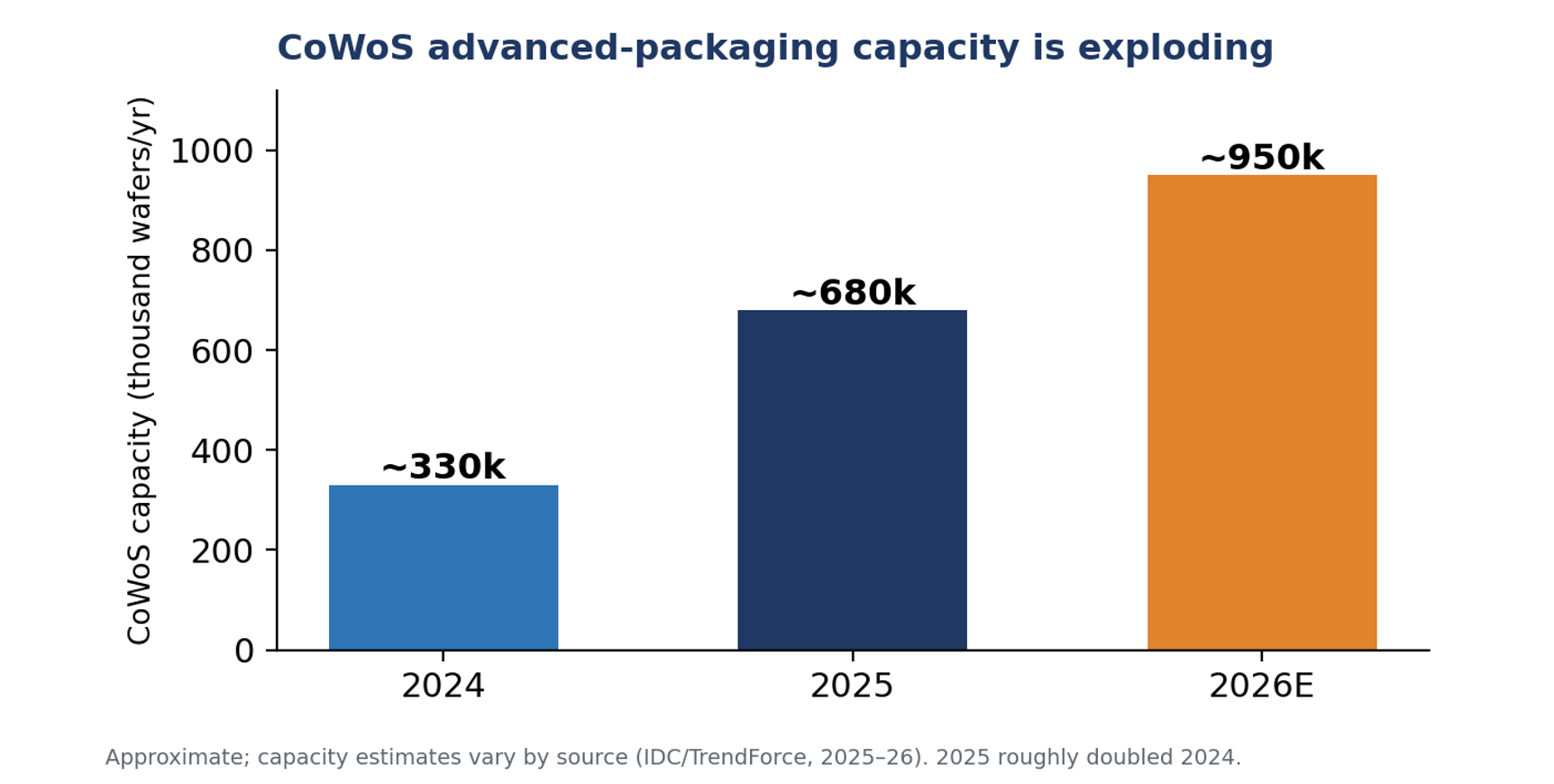

The growth is concentrated in AI-related advanced packaging, and the single most-watched capacity metric is TSMC’s CoWoS, which has roughly doubled year-on-year.

5. Competitive structure and company financials

OSATs are scaled but thin-margin; the foundry/IDM camp is capturing the most advanced (and most profitable) packaging.

|

Company |

Position |

Scale |

Note |

|

ASE Technology |

#1 OSAT |

~$20B group revenue |

Advanced-packaging sales

~$1B in 2025; includes SPIL and an EMS arm |

|

Amkor |

#2 OSAT |

~$6.3B (2024) |

~15% gross margin; Arizona plant; 10-year TSMC capacity agreement |

|

JCET |

China #1 OSAT |

~$5–6B |

Largest mainland-China

assembler |

|

TSMC (adv. pkg) |

Foundry-integrated |

CoWoS leader |

~680k CoWoS wafers in 2025; allocates to Nvidia, Google, others |

6. Business model and economics

Traditional OSAT is a high-volume, low-margin business: gross margins in the mid-teens, competing on cost, scale, and geographic footprint. Advanced packaging offers a path to better economics, but it requires heavy investment in wafer-level, fab-style equipment — which is precisely why the better-capitalized foundries can compete for it. The result is margin pressure from both ends: commodity assembly below, foundry encroachment above.

7. Demand drivers

• AI and HBM. Stacking logic with high-bandwidth memory and integrating chiplets is the core of advanced-packaging demand.

• The end of easy scaling. As transistor shrinks get harder, more performance comes from packaging — structurally favouring this segment.

• CoWoS allocation. TSMC’s packaging capacity gates AI-GPU supply, with 2026 allocations reportedly reserved for Google’s TPU, Meta, OpenAI, and others.

8. Geopolitics and strategic dimension

Packaging has become a reshoring priority: the US CHIPS Act funds back-end capacity (Amkor’s ~$2 billion Arizona plant, with a 10-year TSMC agreement), and Europe is supporting its own. The US-China contest is also reshaping OSAT customer allocation, with Western firms diversifying away from China-based assemblers toward Vietnam, Taiwan, and the US. JCET and other Chinese OSATs, meanwhile, anchor a parallel domestic supply chain.

9. A framework for financial analysis

• Distinguish traditional from advanced. Advanced-packaging mix and growth are the value drivers; traditional assembly is a thin-margin base.

• Watch capex and utilization. A back-end capacity race raises overbuild risk; utilization is the cyclical signal.

• Track foundry encroachment. How much advanced packaging TSMC and Samsung keep in-house caps the OSAT opportunity.

• Mind margins. OSAT returns are structurally lower than foundries’ — advanced packaging is the path up, not a guarantee.

10. Key debates

• Who captures advanced-packaging value? OSATs versus foundries (TSMC) versus IDMs — the segment’s defining contest.

• Overbuild risk. Whether the simultaneous capacity race produces a glut in 2026–27.

• Hybrid bonding leadership. Which players master sub-10-micron hybrid bonding at high yield.

11. Risk summary

• Thin margins — structural, especially in traditional assembly.

• Foundry encroachment — TSMC capturing the most profitable packaging in-house.

• Capex / overbuild — a coordinated back-end build-out risks overcapacity.

• Customer & geographic concentration — AI demand and reshoring politics both concentrate risk.