Where chips become products — and the demand that pulls the whole chain

Executive summary

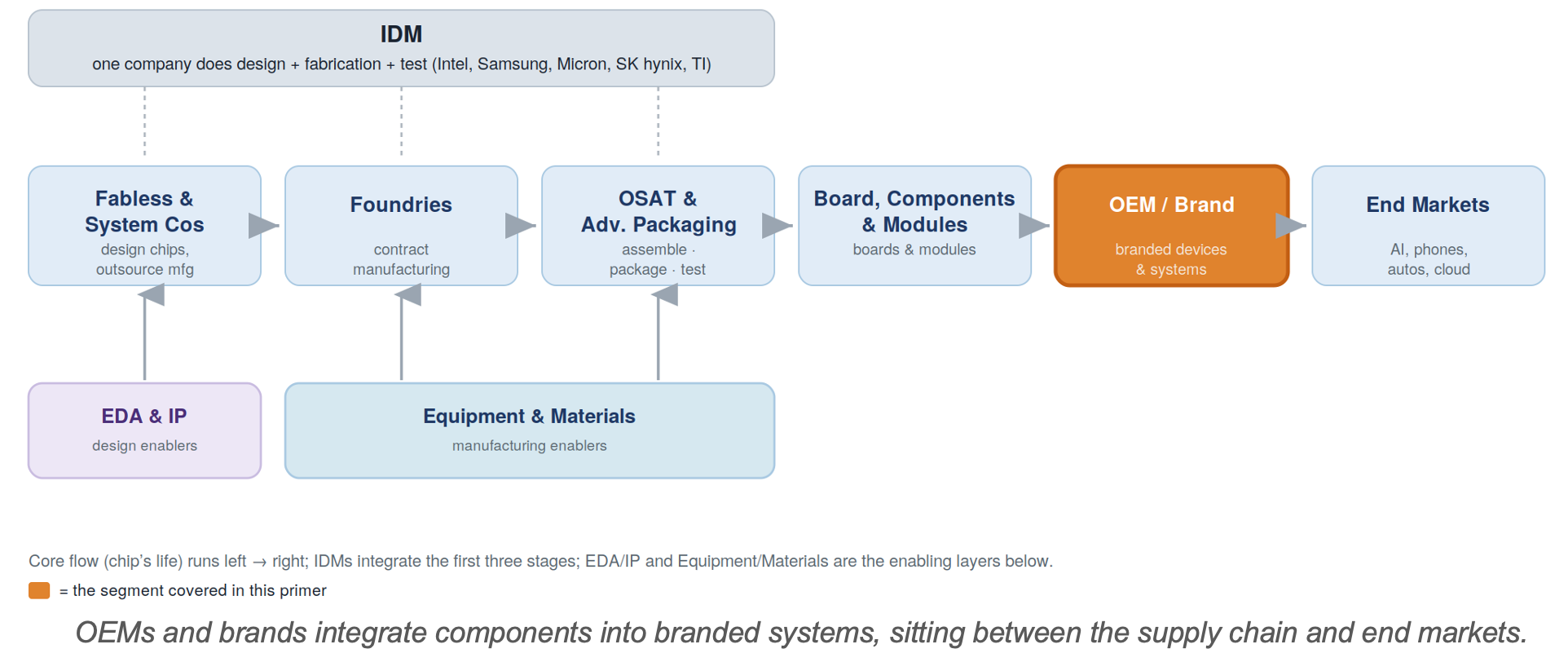

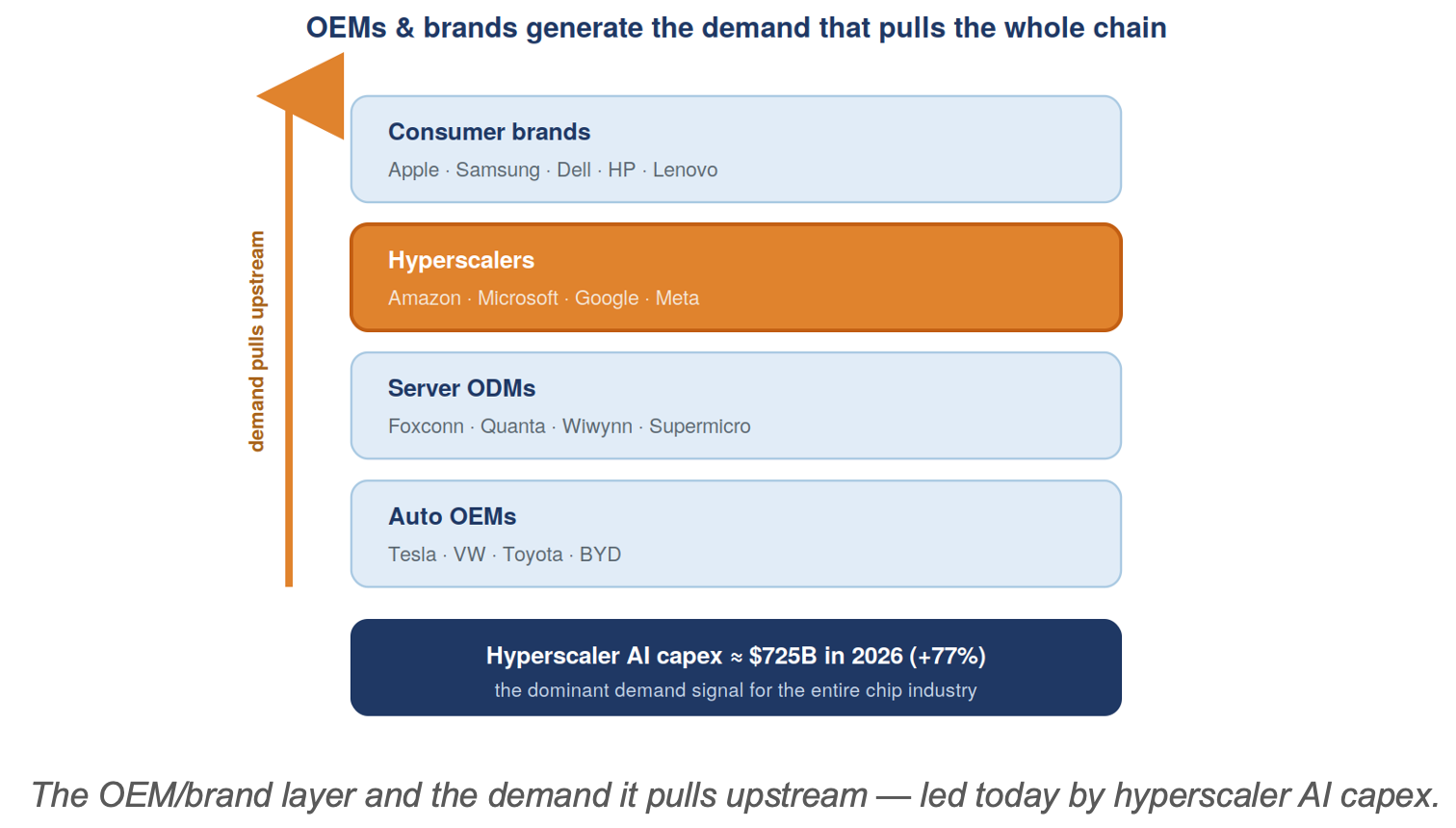

OEMs and brands are where chips become products — the device makers, server builders, and system companies that integrate semiconductors into things people and businesses buy. They are the origin of demand that pulls silicon through the entire value chain. The category spans consumer-device brands (Apple, Samsung, Dell, HP, Lenovo), data-center server ODMs (Foxconn, Quanta, Wiwynn, Supermicro), automakers, and — most importantly today — the hyperscalers whose AI-infrastructure spending now drives the cycle.

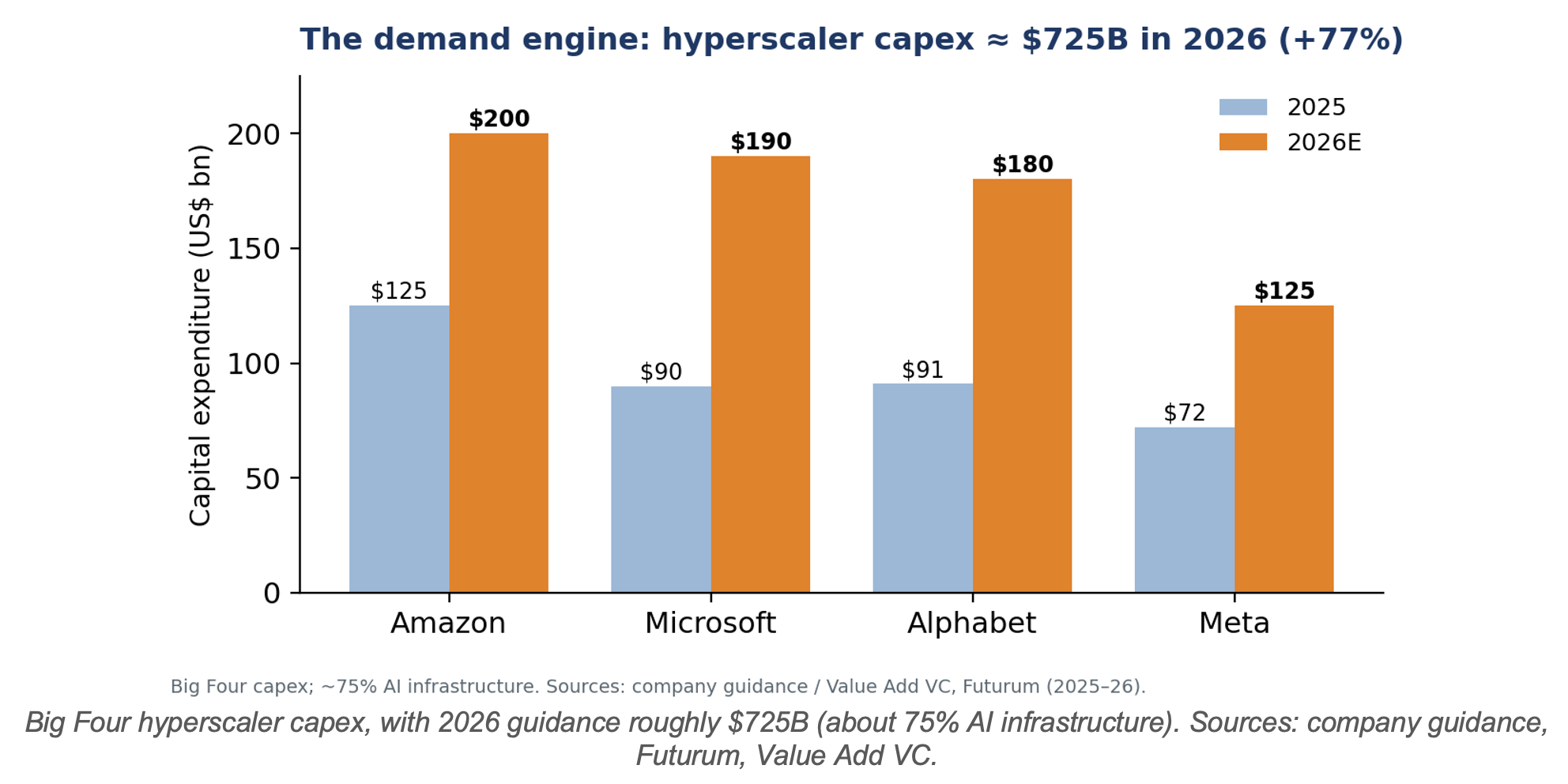

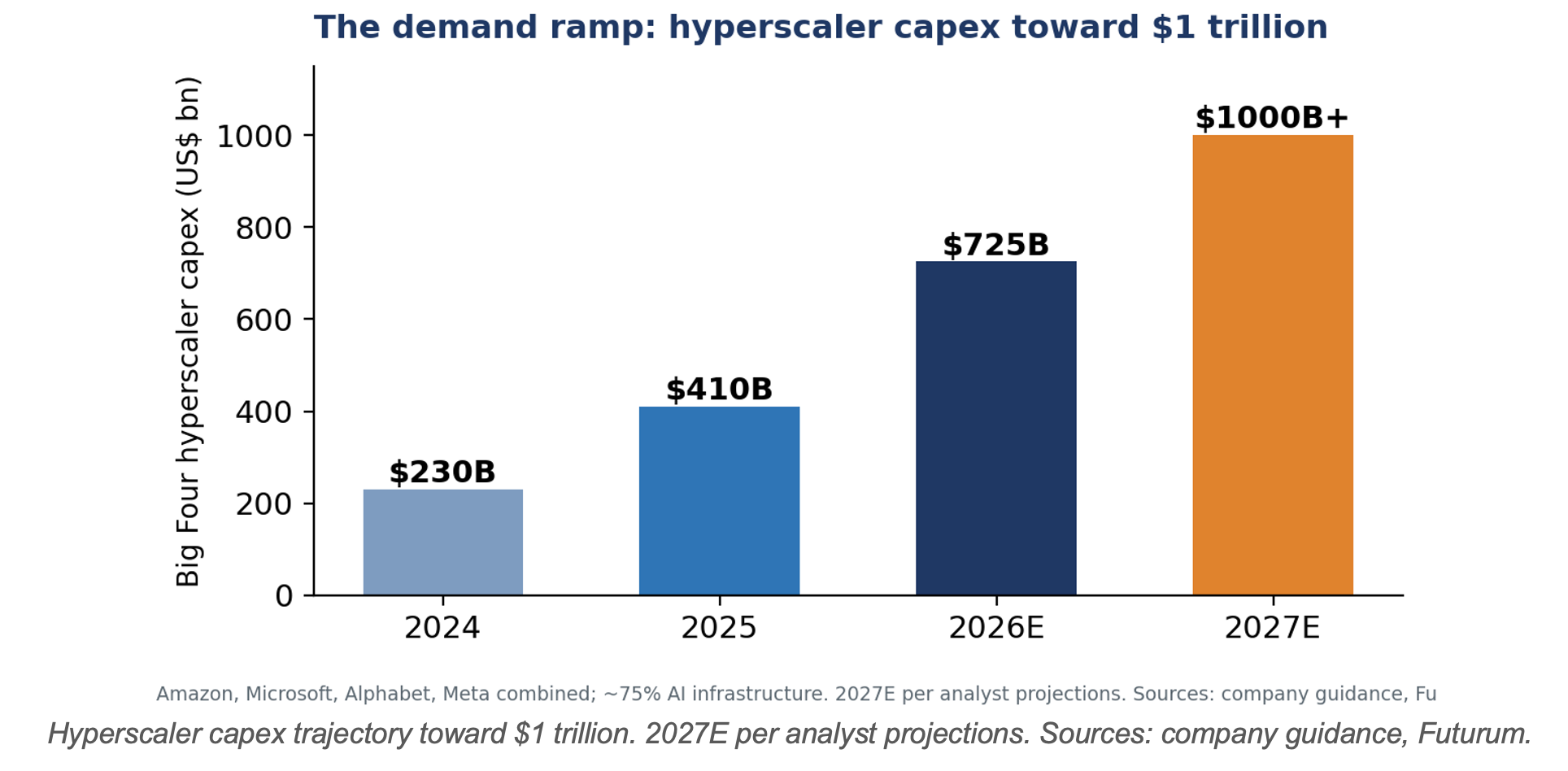

That demand signal is staggering: the four largest US hyperscalers are guiding to roughly $725 billion of capital expenditure in 2026, up about 77% from ~$410 billion in 2025, the overwhelming majority of it AI infrastructure, with analysts projecting big-tech capex above $1 trillion by 2027. This is the engine behind the foundry, fabless, memory, and packaging booms described in the companion primers.

1. Definition and strategic importance

OEMs (original equipment manufacturers) and brands sit at the downstream end of the chain, buying chips, boards, modules, and components and assembling them into finished systems sold under a brand to end markets. They matter because demand starts here — every wafer TSMC makes and every tool ASML sells exists ultimately to satisfy an order that originates with an OEM or a hyperscaler.

2. Position in the value chain

A key nuance: the line between “brand” and “chip designer” is blurring. Apple and the hyperscalers now design their own silicon (covered in the Fabless primer), making them simultaneously the demand origin and an upstream design participant — a vertical integration reshaping the industry’s balance of power.

3. Structure: brands, ODMs, and hyperscalers

Consumer-device brands. Apple, Samsung, Dell, HP, Lenovo, Xiaomi and others design and sell branded phones, PCs, and electronics, capturing brand margin and owning the customer — often outsourcing physical assembly to contract manufacturers (e.g., Foxconn for Apple).

Server and data-center ODMs. The AI build-out is physically assembled by original design manufacturers — Foxconn (Hon Hai), Quanta, Wiwynn, Wistron, and Supermicro — which build the servers and racks that house GPUs and accelerators. These are high-volume, thin-margin businesses booming on AI orders.

Hyperscalers. Amazon, Microsoft, Google, and Meta are both the largest buyers of AI hardware and increasingly the designers of their own chips. Their capital spending is the dominant demand variable for the entire semiconductor industry today.

4. The demand engine: hyperscaler capital spending

The trajectory matters as much as the level: spending has roughly doubled each year and is projected to approach $1 trillion in 2027, with the five largest US hyperscalers reportedly planning to add around $2 trillion of AI-related assets by 2030.

5. Competitive structure and key players

The layer divides by role rather than by a single revenue ranking; margins differ sharply between brand owners and contract builders.

|

Category |

Examples |

Role in the

chain |

|

Device brands |

Apple, Samsung, Dell, HP,

Lenovo |

Design/sell branded devices;

own the end customer; rich margins |

|

Hyperscalers |

Amazon, Microsoft, Google, Meta |

Largest AI-hardware buyers; also design custom silicon |

|

Server ODMs |

Foxconn, Quanta, Wiwynn,

Supermicro |

Build AI servers and racks

(thin-margin, high-volume) |

|

Auto OEMs |

Tesla, VW, Toyota, BYD |

Rising semiconductor content per vehicle |

6. Business model and economics

Economics vary enormously by role. Brand owners like Apple capture high margins by owning design, software, and the customer relationship, while contract ODMs (Foxconn, Quanta) run on razor-thin margins despite enormous revenue. Hyperscalers are not selling hardware at all — their chip and server spending is a cost of delivering cloud and AI services, which is why the return on that capex is so closely scrutinized.

7. Demand drivers

• AI infrastructure build-out. Hyperscaler capex (~$725B in 2026) is the single largest pull on advanced logic, memory, and packaging.

• Device refresh cycles. AI PCs and AI smartphones, plus normal replacement of the ~1.2 billion phones and ~250 million PCs shipped each year, provide a large volume base.

• Automotive content. Electrification and ADAS keep raising the dollar value of chips per vehicle.

8. Geopolitics and strategic dimension

OEMs sit atop globally distributed supply chains exposed to tariffs, export controls, and reshoring pressure. Device assembly is shifting (e.g., toward India and Vietnam); AI-server supply chains concentrate in Taiwan-linked ODMs; and the hyperscalers’ build-out is increasingly constrained not by chips but by power and data-center construction — the emerging physical bottleneck of the AI era.

9. A framework for financial analysis

• Follow the capex guidance. Hyperscaler capital-spending guidance is the leading indicator for the whole semiconductor cycle — watch it above almost anything else.

• Separate brand from contract economics. Apple’s margins and a server ODM’s are not comparable despite both being “OEMs.”

• Watch the ROI question. Whether AI revenue justifies the capex is the debate that could move the entire chain.

• Track the physical constraints. Power availability and data-center construction timelines increasingly gate demand.

10. Key debates

• Is the AI capex sustainable? Whether ~$725B+ of annual investment generates adequate returns — the industry’s biggest open question; a pullback would ripple through every upstream segment.

• Vertical integration. How far OEMs and hyperscalers take in-house silicon, eroding the merchant-chip market.

• Demand concentration. Whether reliance on a handful of hyperscalers makes the cycle more fragile.

11. Risk summary

• AI-capex sustainability — the dominant risk; valuations across the chain embed continued spending.

• Demand concentration — a few hyperscalers drive much of leading-edge demand.

• Margin asymmetry — contract ODMs are structurally low-margin and exposed.

• Physical constraints — power and construction bottlenecks; supply-chain and tariff exposure.