Companies that design and manufacture their own chips — memory, analog, power, and Intel.

Executive summary

Integrated device manufacturers (IDMs) both design and manufacture their own chips — the original structure of the semiconductor industry, predating the split into fabless designers and contract foundries. IDMs own fabs, control their process technology, and sell finished products under their own brand. They persist because, in their domains, product and process are inseparable. Today they fall into three families: memory (Samsung, SK hynix, Micron), analog/power/embedded (Texas Instruments, Analog Devices, Infineon, ST, NXP, Microchip, Renesas), and logic (Intel, now pivoting toward a foundry model).

The defining dynamic of the current cycle is the AI-driven memory supercycle. High-bandwidth memory (HBM) has transformed DRAM from a boom-bust commodity into a constrained, premium, strategically vital product — so much so that in 2025 SK hynix overtook Samsung in both DRAM revenue and, for the first time ever, operating profit. The analog/power family, by contrast, offers steadier, less cyclical growth tied to automotive and industrial electronics, while Intel’s foundry transition is one of the industry’s biggest open questions.

1. Defining the sector and its strategic importance

An IDM performs the entire chip lifecycle in-house: design, wafer fabrication, and assembly/test. This is the opposite of the disaggregated model, in which a fabless company designs and a foundry manufactures. IDMs remain vertically integrated where manufacturing know-how is itself the competitive advantage — the recipe for a DRAM cell or a precision data converter lives in the process, not in a licensable design file.

Their strategic weight is large: IDMs own the memory that every AI accelerator needs, the analog and power chips in every car and factory, and — through Intel — a substantial share of Western leading-edge manufacturing capacity. They also carry the heaviest financial burden in the industry, funding both R&D and multi-billion-dollar fabs.

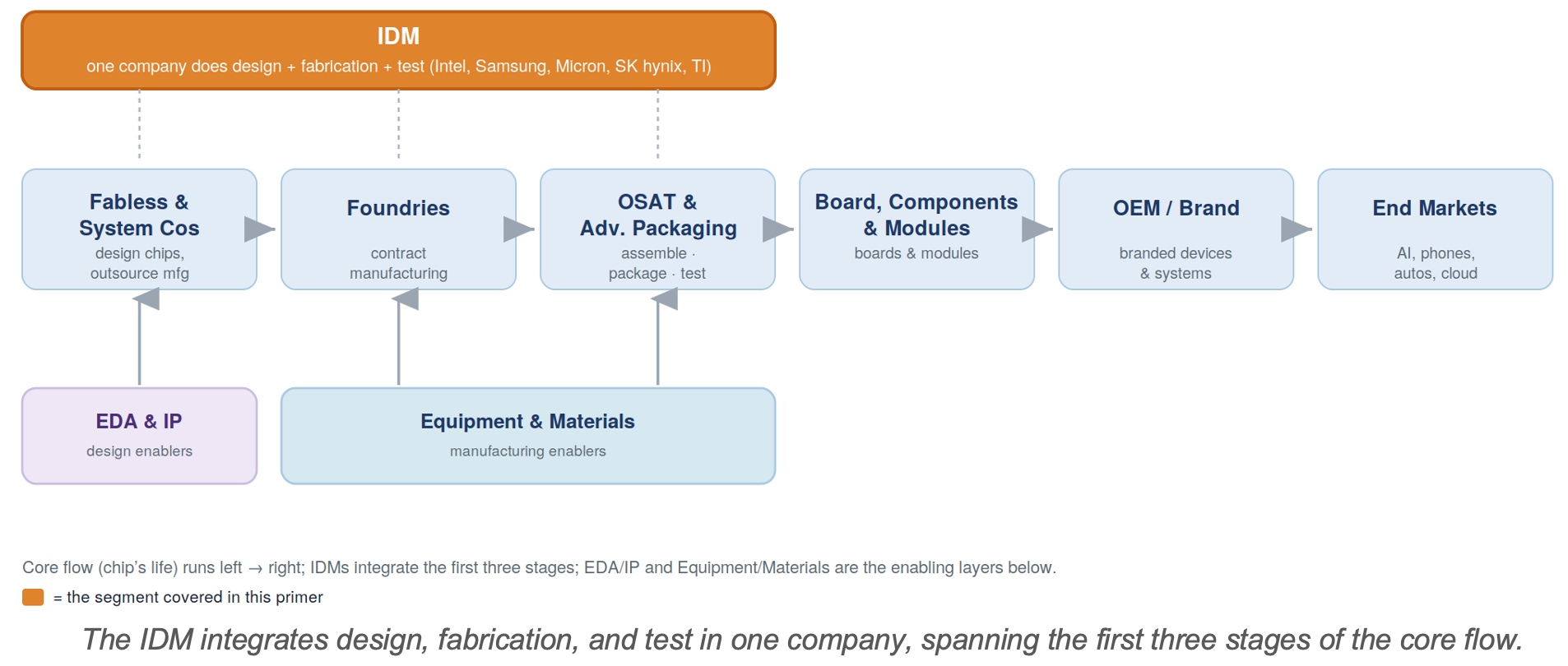

2. Position in the value chain

In the value-chain map, an IDM effectively spans the first three stages — design, fabrication, and test — within a single company, rather than handing the chip between specialist firms.

This integration is increasingly the exception rather than the rule. Leading-edge logic largely abandoned it (fabless + foundry), and even some IDMs now outsource their most advanced nodes to TSMC while keeping mature production in-house — a “fab-lite” hybrid. Memory and analog remain the strongholds of full integration.

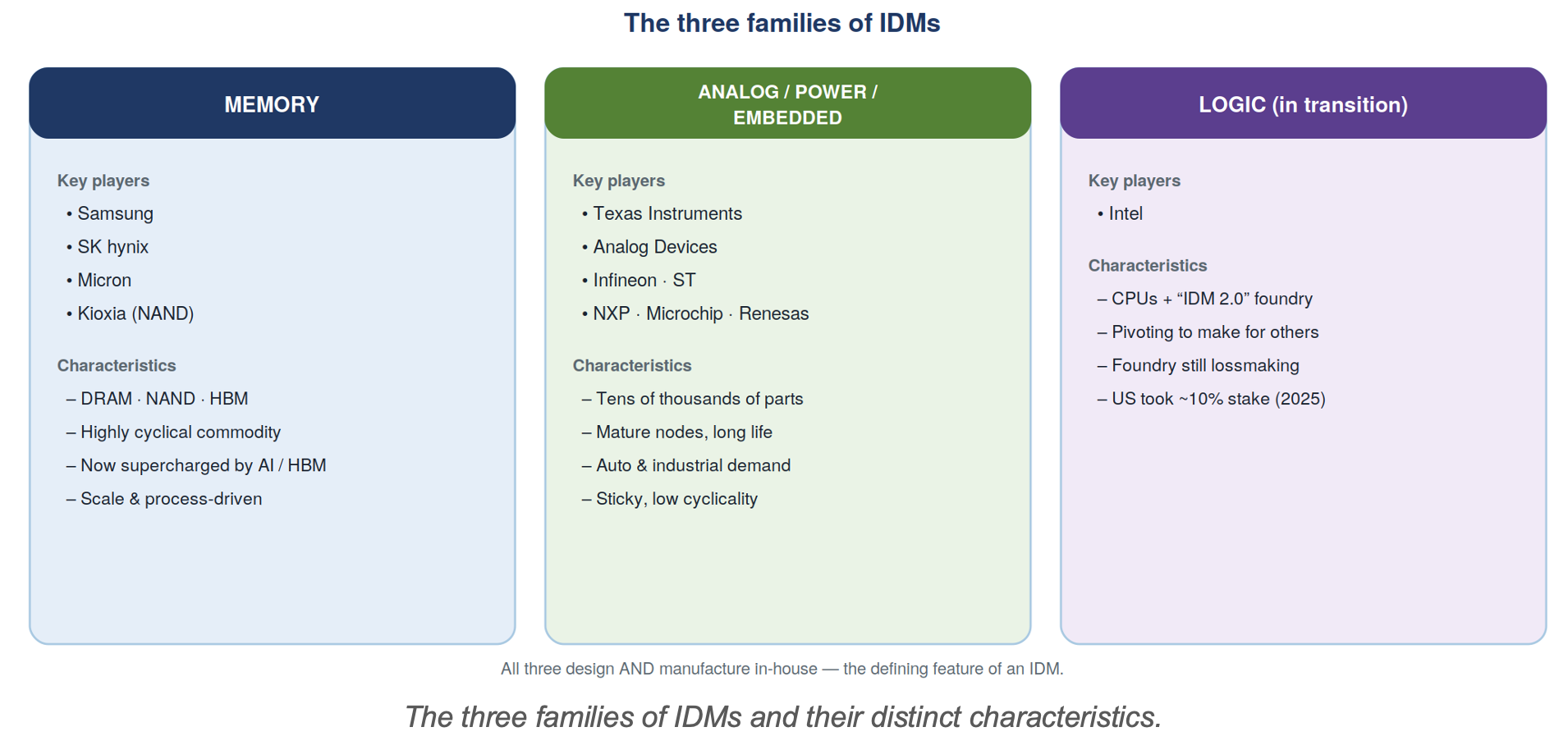

3. The three families of IDMs

IDMs are not one business but three, with very different economics. (This corrects a framing point: there are three families, not two — memory, analog/power/embedded, and logic.)

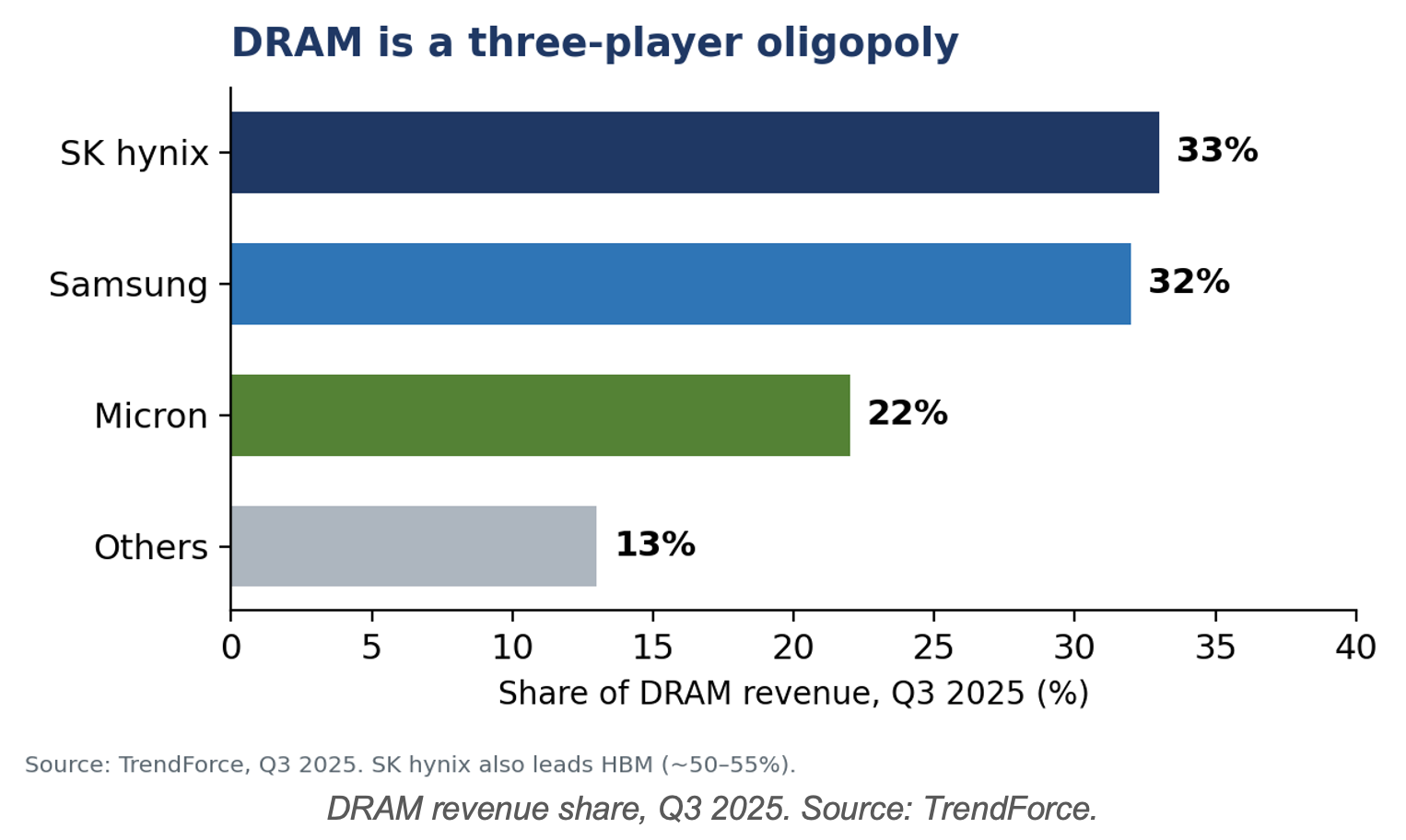

Memory — the cyclical, scale-driven world. DRAM is a tight oligopoly (Samsung, SK hynix, Micron); NAND flash adds Kioxia and others. Historically brutally cyclical, memory has been reshaped by HBM, which is now essential to AI accelerators and commands premium pricing. SK hynix’s early HBM lead and Nvidia relationship vaulted it past Samsung in 2025.

Analog, power, and embedded — the diversified, sticky world. Texas Instruments, Analog Devices, Infineon, ST, NXP, Microchip, Renesas, and onsemi make tens of thousands of long-lived products on mature nodes for automotive and industrial systems. Long lifecycles, high switching costs, and broad catalogs make this far less cyclical; TI’s 300mm analog capacity is a structural cost advantage and Infineon leads in automotive and power.

Logic — Intel, in transition. Intel is pursuing “IDM 2.0,” manufacturing for external customers via Intel Foundry while still designing its own CPUs. The straddle is difficult: Intel Foundry remains lossmaking and behind TSMC, and in August 2025 the US government took an approximately 10% equity stake, underscoring Intel’s strategic importance to domestic manufacturing.

4. Market size and the memory supercycle

The single most important dynamic for IDMs today is the AI-driven memory upcycle. HBM revenue has roughly tripled in two years, dragging the whole DRAM market higher — conventional DRAM contract prices rose 45–55% quarter-on-quarter in late 2025.

Beyond memory, the analog and power market is large (well over $80 billion across the major suppliers) and growing steadily with vehicle electrification and industrial automation, providing ballast against memory’s volatility.

5. Competitive structure and company financials

Memory is a three-player oligopoly; analog is more fragmented but dominated by a handful of scaled incumbents.

|

Company |

Category |

Key 2025

status |

|

SK hynix |

Memory (DRAM/HBM) |

#1 in DRAM (~$49.6B) and HBM

(~50–55%); first-ever operating-profit lead over Samsung |

|

Samsung (DS) |

Memory + foundry + logic |

Regained memory revenue lead in Q4 2025; racing to catch up on

HBM4 |

|

Micron |

Memory (DRAM/NAND/HBM) |

#3 DRAM; reportedly sold out

of HBM for 2026; ~$20B FY26 capex |

|

Intel |

Logic IDM (+ foundry) |

~$53B revenue; Foundry lossmaking; US took ~10% stake (Aug 2025) |

|

Texas Instruments |

Analog & embedded |

~$17–18B revenue; 300mm cost

edge; industry-leading free cash flow |

6. Business model and economics

IDM economics swing with the family. Memory is a high-fixed-cost, capacity-led business: in upcycles, incremental volume drops almost entirely to profit; in downturns, the same leverage produces losses. Analog/power is the opposite — diversified, high-margin, cash-generative, with depreciation-light mature fabs and gross margins often above 60%. Intel’s logic business carries the dual cost of cutting-edge R&D and leading-edge fabs, the heaviest burden in the industry.

7. Demand drivers

• AI and HBM (memory). The dominant driver — HBM demand from AI accelerators has tightened the entire DRAM market and lifted pricing across the board.

• Automotive and industrial electrification (analog/power). Rising semiconductor content per vehicle and in factory automation steadily grows analog, power, and microcontroller demand.

• Strategic/sovereign manufacturing. Government support (US CHIPS Act, the Intel stake, EU and Asian programs) is reshaping where IDMs build capacity.

8. Geopolitics and strategic dimension

IDMs sit at the centre of technology policy. Memory sales to China and HBM export rules are politically sensitive; Intel’s manufacturing is treated as a strategic national asset (hence the US equity stake); and analog/power suppliers are exposed to automotive supply-chain and tariff dynamics. The memory makers’ fabs in Korea, the US (Micron, and new HBM-related facilities), and elsewhere are increasingly shaped by subsidy and security considerations.

9. A framework for financial analysis

• Separate the families. Never value a memory IDM like an analog one — the cyclicality, margin structure, and capital intensity are fundamentally different.

• For memory, watch the cycle indicators. DRAM/NAND contract prices, bit-shipment growth, inventory levels, and HBM mix are the key signals; HBM’s premium is now the main profit lever.

• For analog, watch breadth and free cash flow. Product-catalog diversity, end-market mix, and FCF conversion matter more than any single node.

For Intel, watch foundry execution. External-customer wins, node milestones (18A/14A), and foundry losses are the variables that decide the thesis.

10. Key debates

• How long does the memory supercycle last? Whether HBM keeps the market tight or an eventual capacity glut returns memory to its boom-bust pattern.

• Can Intel’s foundry pivot succeed? Arguably the single biggest open question in Western semiconductors.

• Does “fab-lite” spread? Whether more IDMs outsource leading-edge production to TSMC while keeping mature fabs.

11. Risk summary

• Memory cyclicality — the most volatile part of semiconductors despite the HBM tailwind.

• Capital intensity — IDMs fund both R&D and fabs, amplifying downside in downturns.

• Intel execution risk — a foundry stumble would have outsized strategic consequences.

• Geopolitics — memory/HBM export rules and strategic-asset status add policy risk.