The chip designers — and the system makers now designing their own silicon.

Executive summary

Fabless companies design chips but outsource manufacturing to foundries. By shedding the fixed cost of a fab, they became the dominant model for leading-edge logic and the home of the AI era’s most valuable companies. The category spans classic merchant vendors (Nvidia, AMD, Qualcomm, Broadcom, MediaTek, Marvell) and a fast-growing set of system companies designing their own silicon (Apple; hyperscalers such as Google, Amazon, Microsoft, and Meta).

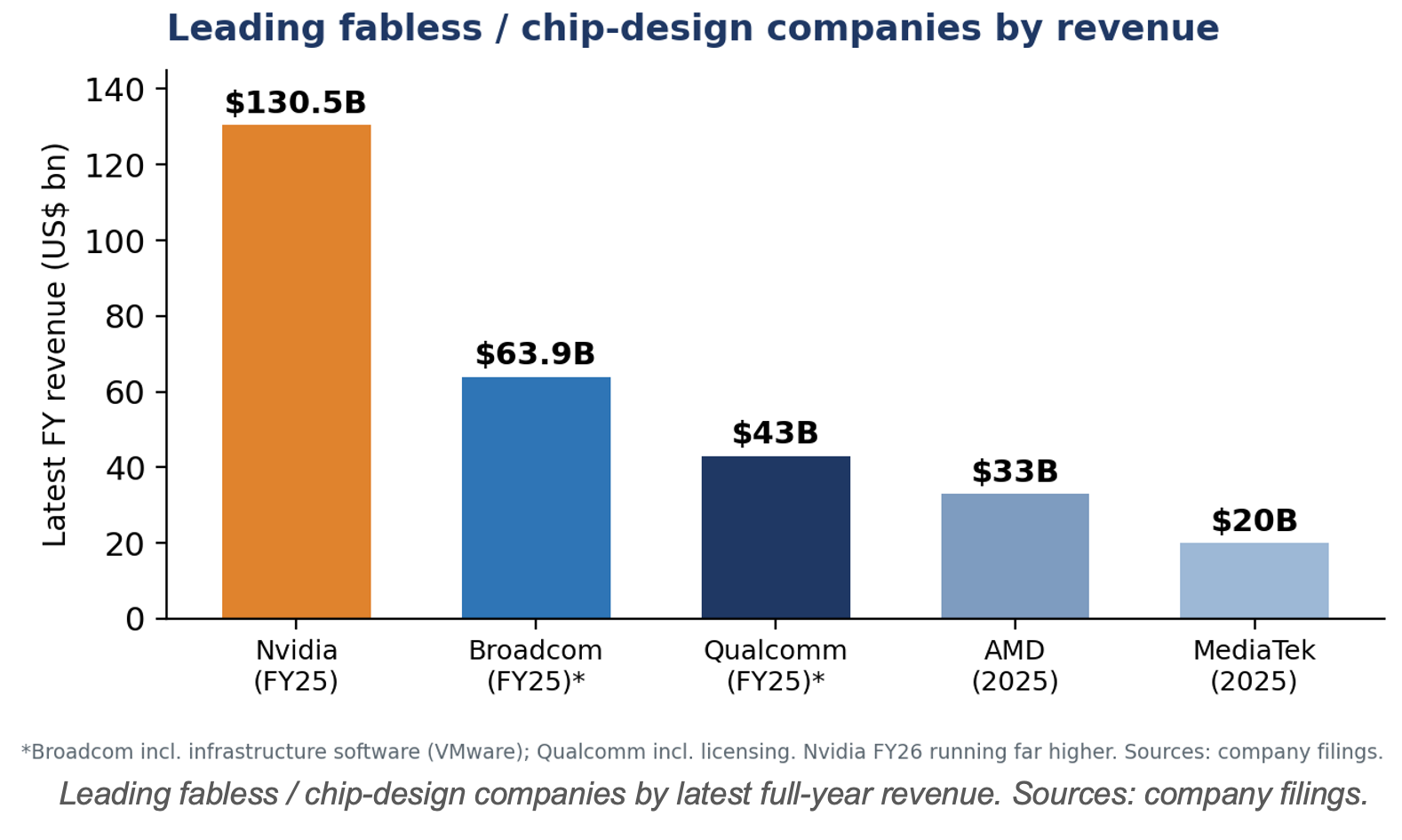

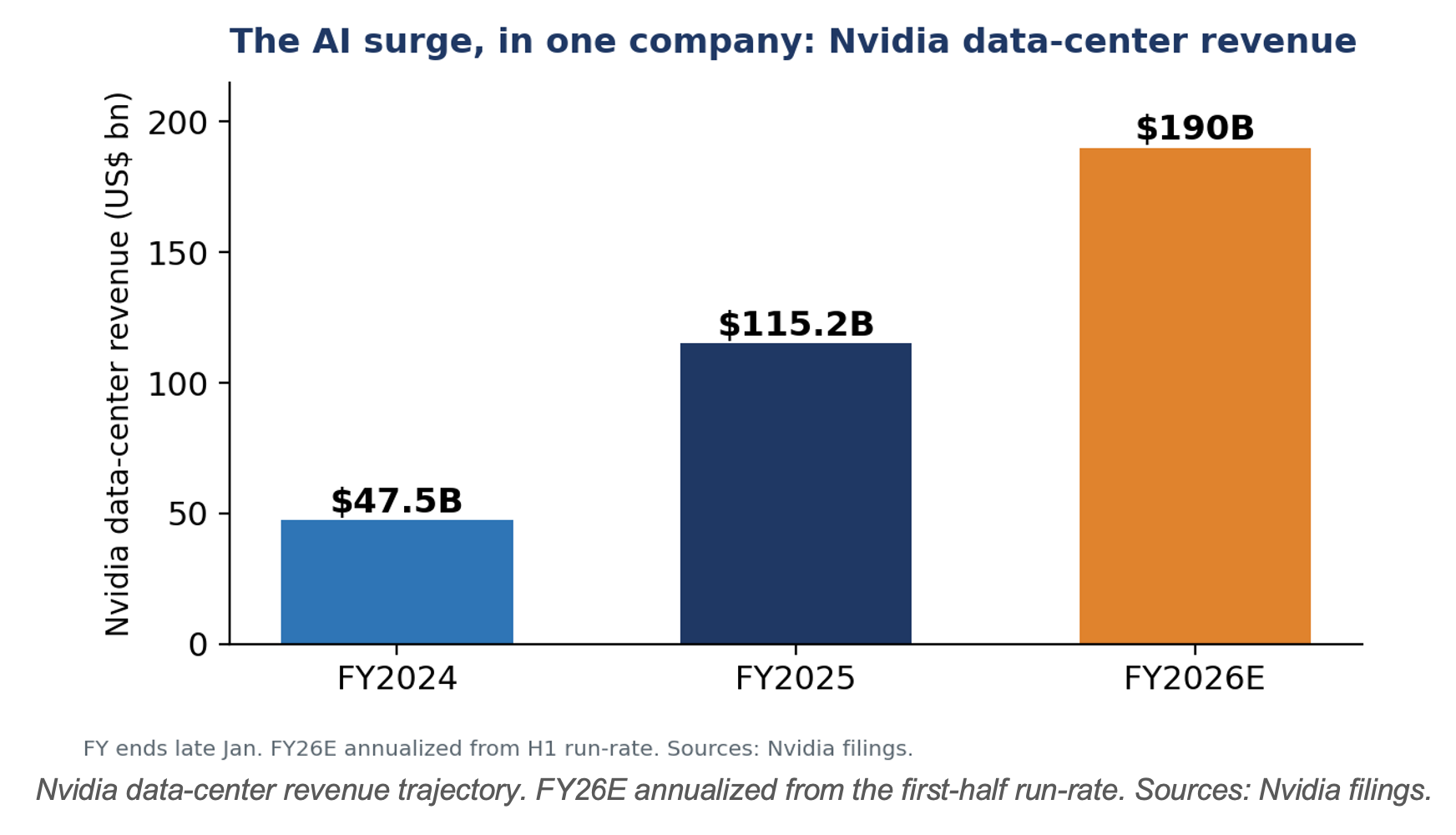

The economics are extraordinary — asset-light, software-like gross margins, innovation-led growth. Nvidia is the emblem: fiscal-2025 revenue of $130.5 billion, up 114%, with data-center revenue of $115.2 billion and gross margins above 70%, and fiscal 2026 running far higher still. The model’s defining dependency is its reliance on a single manufacturer, TSMC, for leading-edge production.

1. Defining the sector and its strategic importance

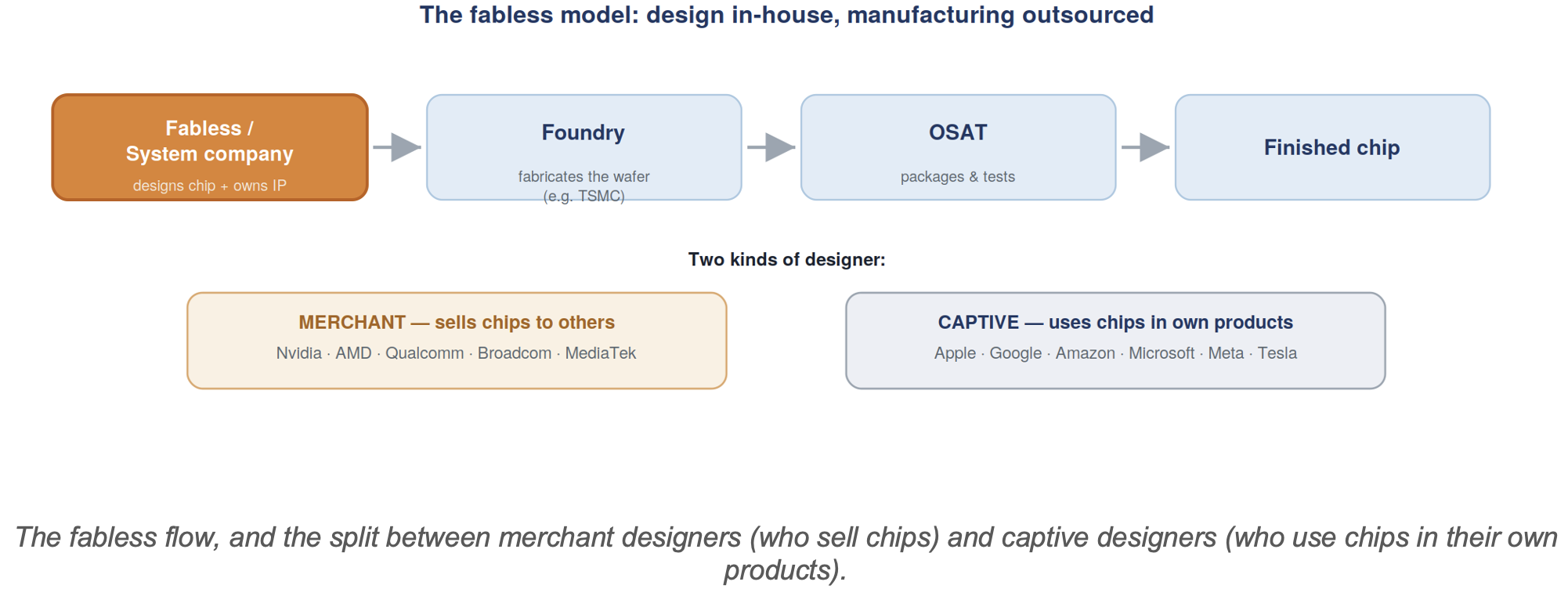

A fabless company owns the design, the intellectual property, and the customer relationship — but not the factory. It hands a finished design to a foundry for fabrication and to an OSAT (or the foundry) for packaging and test. This let design specialists compete on architecture and time-to-market while manufacturing specialists competed on process and scale.

The strategic significance today is concentration of value: a handful of fabless designers capture much of the profit of the AI build-out, and they increasingly include the largest technology companies in the world, which now design chips for their own use.

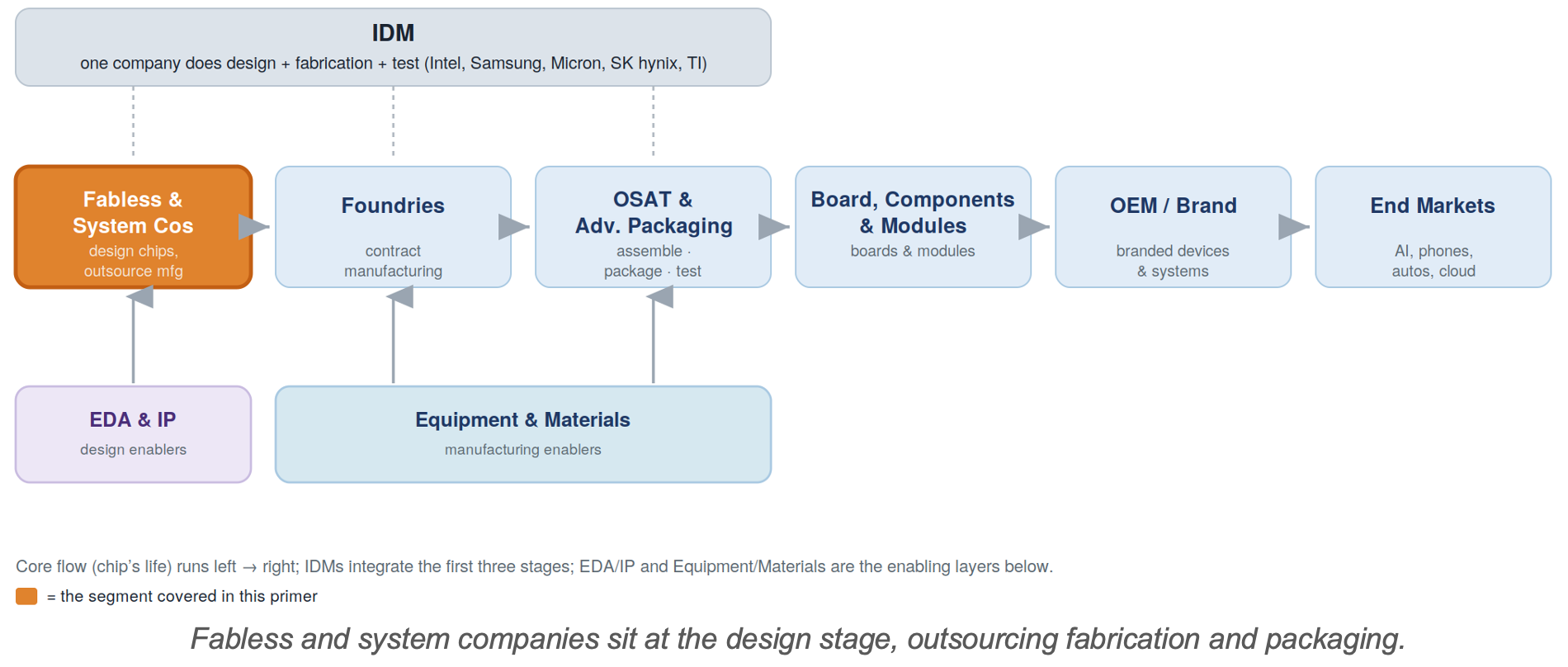

2. Position in the value chain

Fabless and system companies occupy the design stage, outsourcing everything downstream.

The model succeeded because leading-edge fabs became too expensive for most firms to own. Separating design from manufacturing created the foundry industry as its mirror image — the two are economically in-separable.

3. How the model works: merchant versus captive

Merchant fabless. Nvidia (GPUs/AI accelerators), AMD (CPUs and GPUs), Qualcomm (mobile, automotive, and a data-center push), Broadcom (networking and custom AI accelerators), MediaTek (mobile/edge SoCs), and Marvell (data-center connectivity). They design chips and sell them to others.

Captive (system) silicon. Apple, Google (TPU), Amazon (Graviton, Trainium), Microsoft (Maia), Meta (MTIA), and Tesla design chips for internal use rather than sale. They are fabless in method but monetize through their products and services — and are now major foundry and IP customers, reshaping the competitive map.

4. Market size and segmentation

The AI boom has concentrated enormous value in a few designers, with Nvidia far ahead and Broadcom rising fast on custom accelerators (“XPUs”) for hyperscalers.

Nvidia’s data-center business alone illustrates the scale of the shift — it has more than doubled in a single year and dwarfs the rest of the company.

5. Competitive structure and company financials

The merchant tier is concentrated and highly profitable; the captive designers do not sell chips but are now decisive buyers.

|

Company |

Focus |

Latest FY

revenue |

Note |

|

Nvidia |

GPUs / AI accelerators |

$130.5B (FY25, +114%) |

~73% gross margin; data

center $115.2B; FY26 far higher |

|

Broadcom |

Networking + custom AI XPUs (+ software) |

$63.9B (FY25) |

AI-semi revenue surging; ~66% adj. EBITDA |

|

Qualcomm |

Mobile + automotive/IoT +

data center |

$44.3B (FY25) |

Non-Apple QCT +18%;

diversifying |

|

AMD |

CPUs / GPUs |

~$35B (2025) |

Data center $16.6B (+32%); client & gaming $14.6B |

|

MediaTek |

Mobile & edge SoCs |

~$20B (2025) |

Largest non-US mobile chip

designer |

6. Business model and economics

The fabless model is capital-light: no fab to build means high returns on capital and the freedom to redirect spending into R&D and design talent. The flip side is that manufacturing power — and the associated bargaining leverage and risk — sits with the foundry. Gross margins range from Nvidia’s ~73% to lower levels for commoditized mobile parts; the AI leaders combine high margins with explosive volume.

7. Demand drivers

• AI accelerators. By far the largest driver — GPUs and custom ASICs for training and inference, sold into the hyperscaler build-out.

• The custom-silicon boom. Hyperscalers designing their own chips multiply design starts and reshape competition (merchant GPUs versus custom XPUs).

• Mobile, PC, and automotive. Smartphone, AI-PC, and automotive SoCs provide a large, steadier volume base beneath the AI surge.

8. Geopolitics and strategic dimension

Export controls bite the fabless leaders directly. Nvidia took a $4.5 billion charge in early fiscal 2026 on restricted H20 sales to China, and access to the Chinese market for advanced accelerators remains a live policy variable. The model’s reliance on TSMC also concentrates geopolitical risk in Taiwan — a single point of failure for nearly all leading-edge fabless production.

9. A framework for financial analysis

• Separate AI from the rest. Data-center/AI revenue and gross-margin trajectory dominate the leaders’ valuations; track design wins and supply (CoWoS, HBM) as much as demand.

• Watch customer concentration. A handful of hyperscalers drive a large share of AI-chip demand — powerful but concentrated.

• Mind the foundry dependency. Leading-edge capacity and pricing at TSMC are an external constraint on fabless growth and margins.

• Value the moat, not just growth. Software ecosystems (e.g., CUDA) and IP can be more durable than any single product generation.

10. Key debates

• GPU versus custom ASIC. Whether merchant GPUs (Nvidia/AMD) or hyperscaler custom XPUs (via Broadcom/Marvell) capture more of the AI-accelerator market — the sector’s central question.

• Durability of Nvidia’s dominance. How long its hardware-plus-software lead persists against custom silicon and rivals.

• Vertical integration. How far hyperscalers and device brands take in-house silicon, and what that does to the merchant market.

11. Risk summary

• TSMC / Taiwan concentration — a single manufacturing dependency for leading-edge production.

• Geopolitics — export controls can remove market access quickly (the H20 charge).

• AI-cycle risk — valuations embed sustained AI capex; a slowdown would hit hard.

• Customer concentration — dependence on a few hyperscaler buyers.