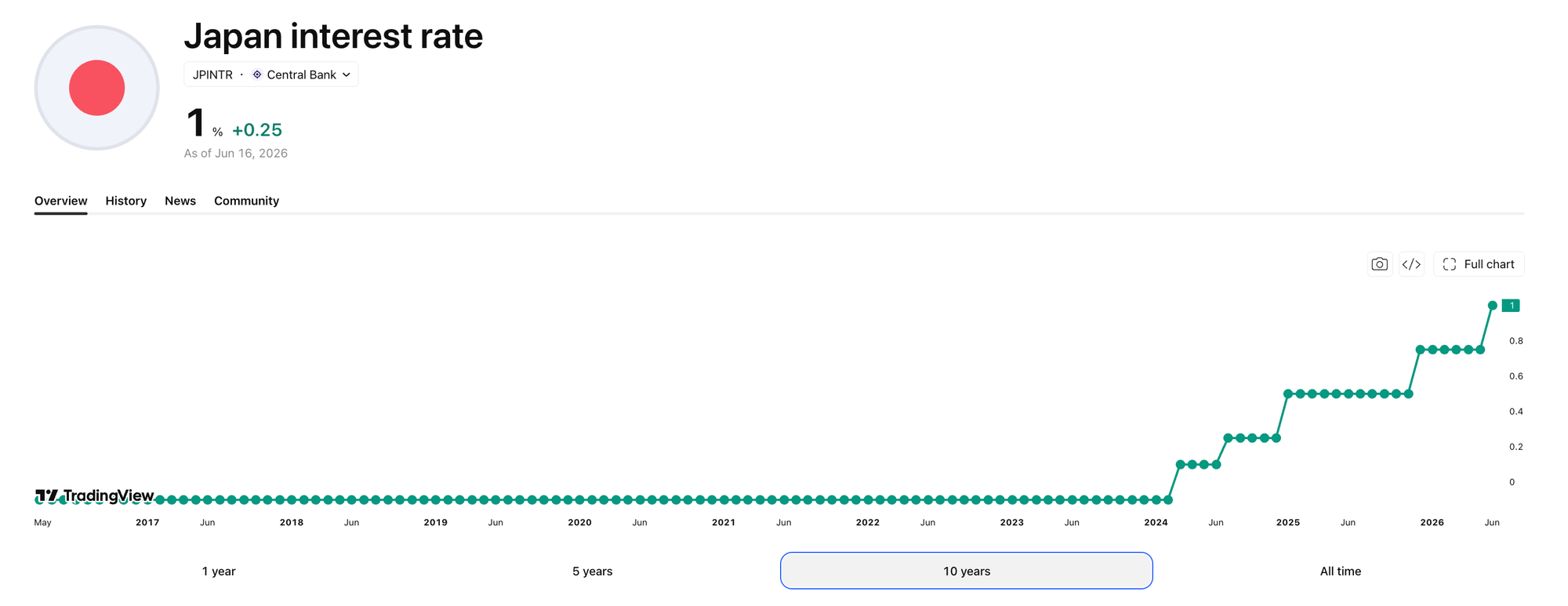

The Bank of Japan has raised its policy rate to around 1.0%, with the decision approved by a 7–1 majority. The complementary deposit facility rate will also rise to 1.0%, while the basic loan rate increases to 1.25%. The new guideline takes effect from June 17, 2026.

This is more than a routine rate hike. For decades, Japan was the global symbol of ultra-low rates, weak inflation and persistent monetary easing. Now the BOJ is moving further away from that old regime. The key question for investors and macro watchers is not simply whether Japan has tightened, but whether this is the beginning of a longer tightening cycle.

source: https://www.tradingview.com/symbols/ECONOMICS-JPINTR/

The BOJ’s own explanation shows why the decision matters. Japan’s headline inflation picture is mixed: CPI excluding fresh food has recently been below 2%, partly because government measures have reduced the household burden of higher energy prices. But the BOJ is worried that crude oil costs, business-to-business price pass-through and rising medium- to long-term inflation expectations could push underlying inflation above its 2% target.

Viewpoint: the BOJ is no longer reacting only to current inflation; it is trying to manage the risk that Japan’s wage-price cycle becomes durable.

That makes the next few months highly important for event-based forecasting. If inflation rebounds, wage growth remains firm and the yen stays weak, expectations for another rate hike could rise. A Reuters survey before the meeting showed economists broadly expected a move to 1.0%, with many also expecting the BOJ to raise rates again to 1.25% later in 2026.

But the BOJ is not tightening in a straight line. It also noted that Japan’s economy has recovered moderately, while some weakness remains due partly to the Middle East situation. Higher crude oil prices may hurt corporate profits and household real income, even as they raise inflation pressure. In other words, Japan faces a policy trade-off: raise rates too slowly and inflation expectations may drift higher; raise too fast and growth may weaken.

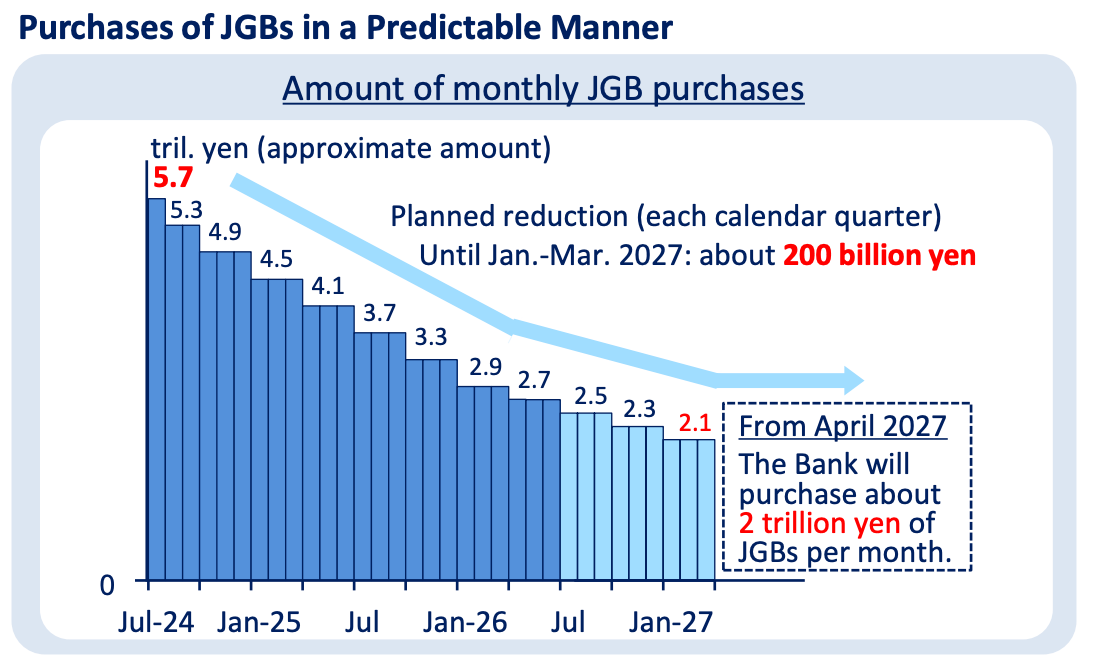

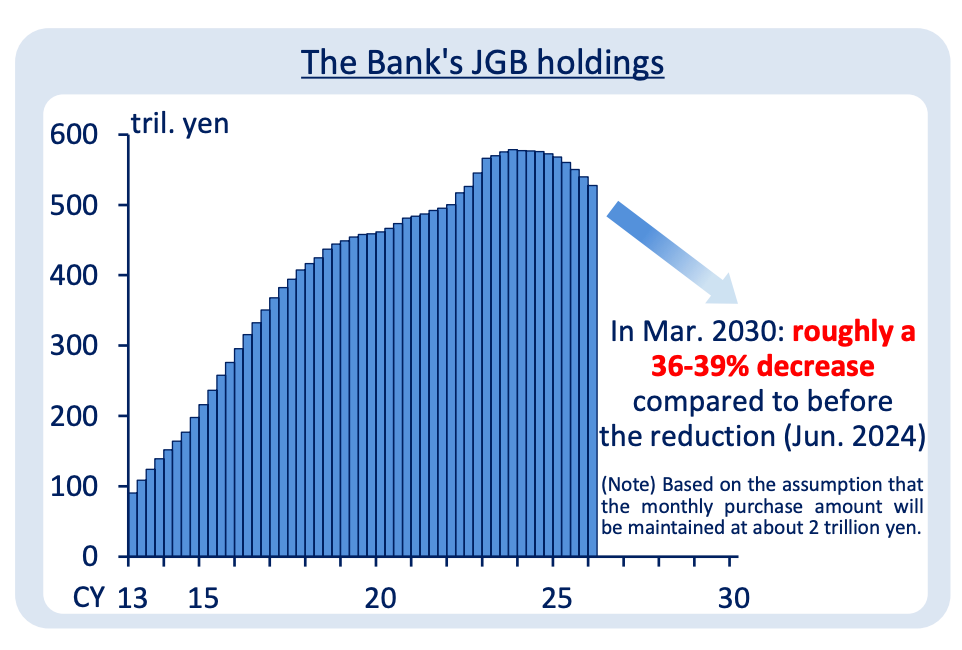

The central bank’s bond policy adds another layer. The BOJ will continue reducing monthly JGB purchases by about ¥200 billion each calendar quarter until January–March 2027, then hold monthly purchases at about ¥2 trillion from April 2027. The BOJ estimates its JGB holdings could fall by roughly 36–39% by March 2030 compared with before the reduction began in June 2024.

Still, the BOJ is keeping a safety valve. It says long-term rates should generally be formed in markets, but it is prepared to respond flexibly if long-term rates rise rapidly, including by increasing JGB purchases.

This creates several clean forecasting questions: Will Japan hike again by year-end? Will core CPI return above 2%? Will the yen strengthen after the hike, or will rate differentials and energy import costs keep it under pressure? Will the BOJ slow its JGB purchase reduction if bond yields spike?

The BOJ’s message is clear: Japan’s era of emergency monetary policy is fading. The open question now is whether this normalization stays gradual, gets interrupted, or accelerates.

Original BOJ Links:

- Bank of Japan policy decision, June 16, 2026:

https://www.boj.or.jp/en/mopo/mpmdeci/mpr_2026/k260616a.pdf - BOJ plan for outright purchases of JGBs:

https://www.boj.or.jp/en/mopo/mpmdeci/mpr_2026/k260616d.pdf - BOJ quarterly JGB purchase schedule for July–September 2026:

https://www.boj.or.jp/en/mopo/mpmdeci/mpr_2026/mpr260616a.pdf