In April 2025, Elon Musk revealed that Optimus production had stalled over a magnet problem: Tesla was waiting on a Chinese export license for the rare-earth magnets that drive one of the robot's arm actuators. It was an unusually specific admission, and it pointed at a dependency the rest of the industry shares but rarely names.

More than a year on, the production reality hasn't moved in the direction Tesla needs. The company had drawn up plans to build at least 5,000 Optimus units for internal use by the end of 2025; external estimates put actual output far lower — market researcher Omdia pegged 2025 humanoid shipments from Tesla, Figure, and Agility at roughly 150 units each. Against that backdrop, the 5,000 target reads less like a miss than a category error.

What Tesla once described as something it was "working through with China" is no longer a quarterly-earnings footnote. It has become a structural problem for an industry still in its infancy — and to see why, you have to look at the magnet itself.

How Soon Will the West Catch Up with China in Humanoid Market Share?

Why the Magnet Is the Chokepoint

Strip a humanoid down and you find dozens of actuators, nearly every one built around a permanent magnet. Morgan Stanley's teardown of Tesla's Optimus Gen 2 counts roughly 40 motors and about 3.5 kg of neodymium-iron-boron (NdFeB) per robot — twice what goes into an electric car. NdFeB dominates because it offers the highest torque and power density of any commercial magnet, and in a humanoid that density is everything: it sets how much the robot lifts, how nimbly it moves, and how long it runs per charge. The magnet-free alternatives are all heavier and weaker for the same output — a poor trade in a machine that carries its own power supply inside a human-scale frame.

The geopolitical wrinkle is heat. Motors crammed into tight joints run hot, and ordinary NdFeB loses its magnetism as temperature climbs, so manufacturers dope it with two heavy rare earths — dysprosium and terbium — to hold it stable under load. Those additives are exactly what China's April 2025 export controls targeted. Neodymium itself was never restricted; the regime instead covered seven medium and heavy elements — including terbium and dysprosium — plus any finished NdFeB magnet containing them. The high-temperature grade a humanoid actuator actually needs sits squarely inside the controlled category.

And there is no quick way around it. Rare earths aren't geologically rare, but separating them is difficult, and China has spent decades building a refining base almost no one else has: it mines well over half the world's supply, processes roughly 90%, and makes close to 90% of all high-performance magnets. New mines and separation plants take years to build. So when Beijing throttles dysprosium and terbium, there is no fast Western substitute — least of all for a humanoid program that needs the heat-resistant grade in volume.

Shoring Up the Reserves

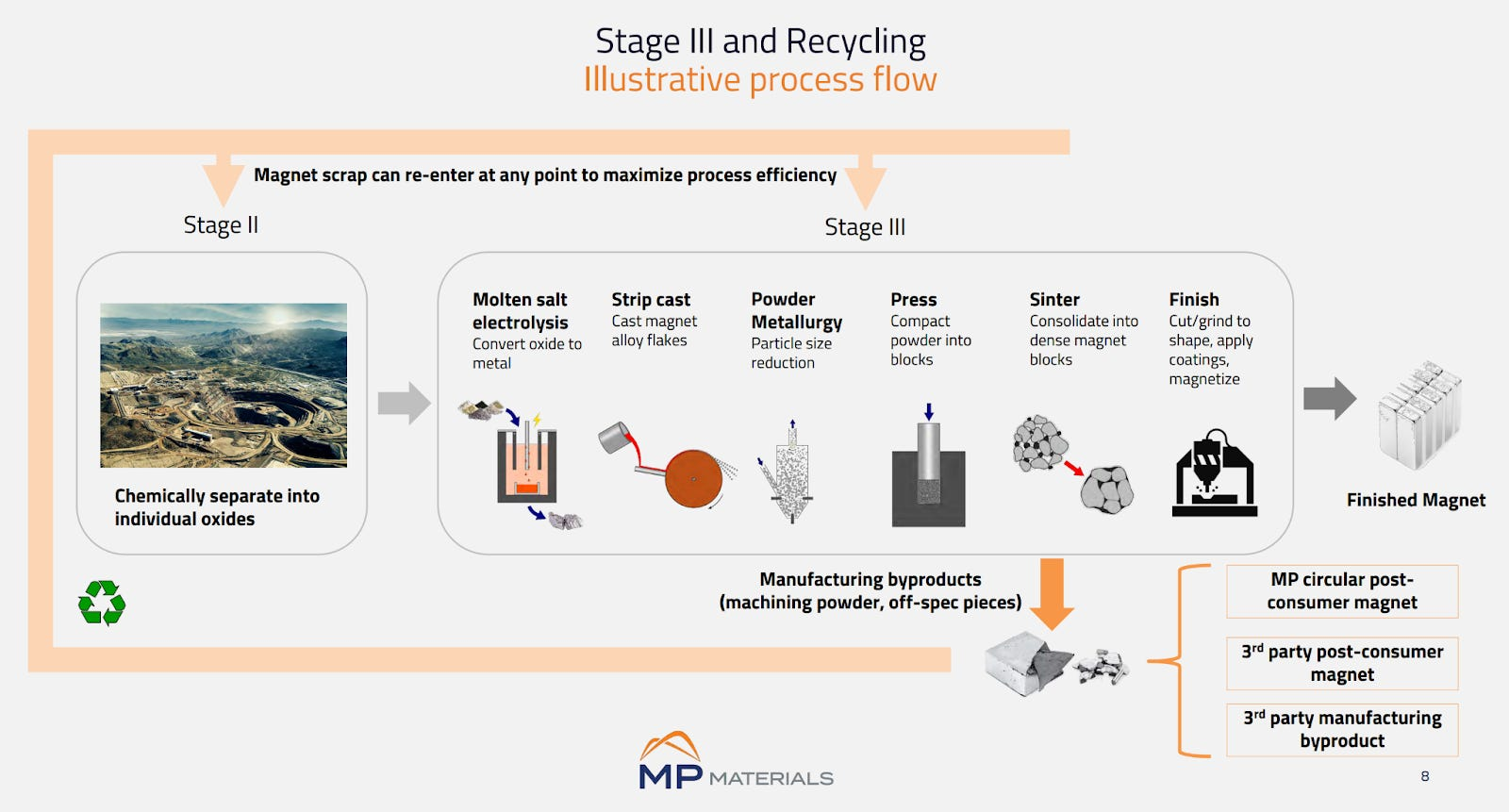

Washington's response has been to try to build the missing supply chain more or less from scratch. In July 2025, the U.S. Department of Defense committed $400 million to MP Materials in convertible preferred stock and warrants — enough to make the Pentagon the company's largest shareholder, with a stake that can reach 15% — alongside a price floor on domestic output and a loan to expand heavy-rare-earth separation. Days later, Apple added a $500 million partnership to produce recycled magnets at MP's Fort Worth plant, using feedstock refined at Mountain Pass in California.

It is a serious pair of commitments, but the timing is the catch. Magnet shipments under the Apple deal aren't expected to begin until 2027, and that initial capacity is earmarked for Apple's own devices — hundreds of millions of them. The Pentagon's motive, meanwhile, is defense-supply resilience, not humanoid robots. For the robotics industry specifically, the practical takeaway is that domestic, robot-grade magnet supply is still years away, while Chinese producers keep scaling with no equivalent constraint. The fix is real; it simply arrives after the gap it was meant to close has had more time to widen.

The Shortage Is Asymmetric — and So Is the Market

The defining feature of this shortage is that it isn't global. If it were, Chinese robot makers would be struggling too — and they aren't. They draw on a domestic supply that isn't subject to China's own export controls, so the constraint that pins down Tesla simply doesn't apply to them. (Even after a late-2025 de-escalation and a general-license mechanism that resumed some shipments, exports of the key heavy rare earths have stayed well below their pre-restriction baseline, and defense uses remain off-limits — the asymmetry has eased at the edges, not closed.)

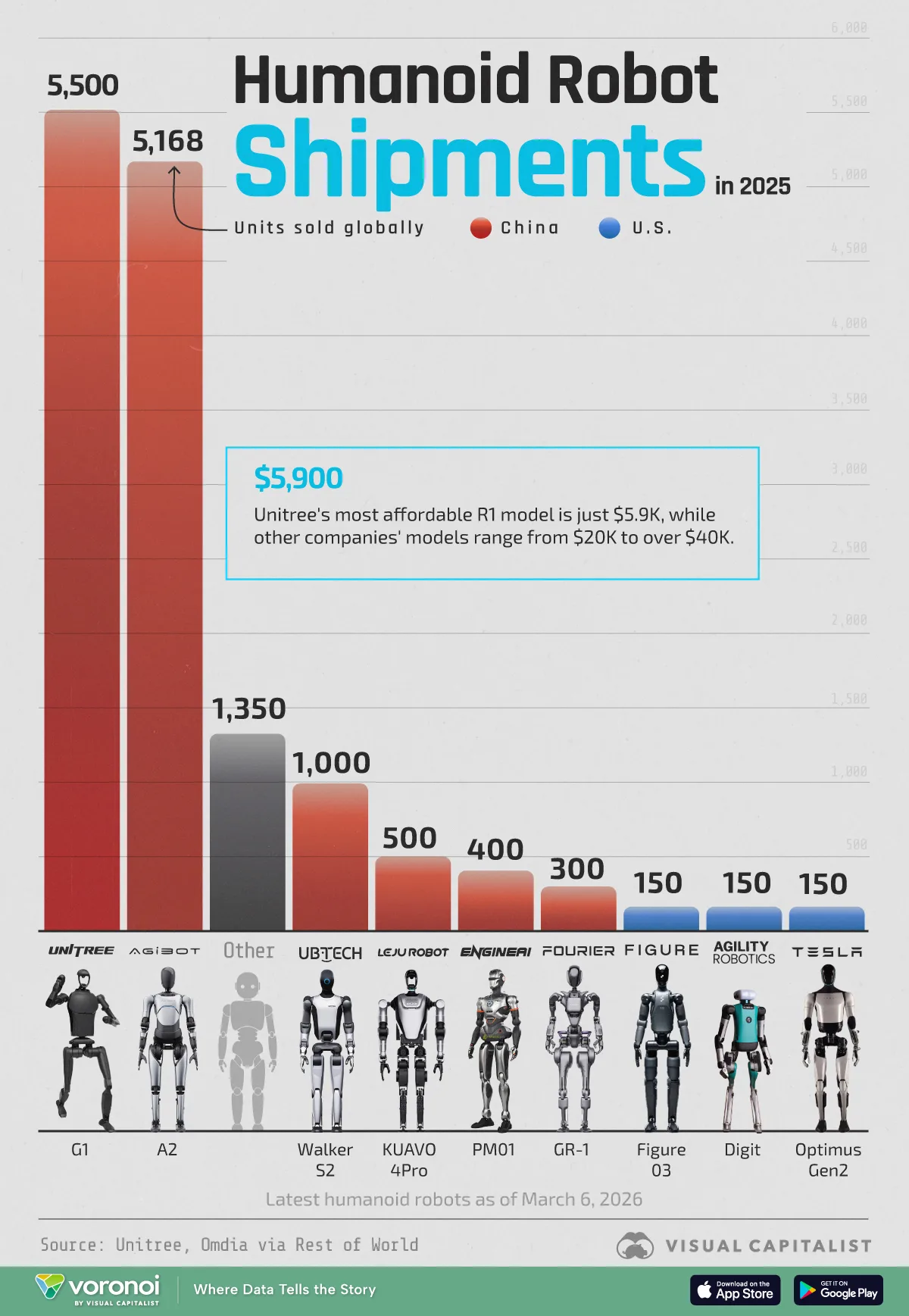

The market reflects that split. Chinese firms account for around 80% of global humanoid shipments. Unitree alone shipped more than 5,500 units in 2025 and is targeting as many as 20,000 in 2026; Tesla is still straining to reach four figures.

Price is the other axis, and it isn't close. Unitree's G1 starts in the $13,000–$16,000 range, and its R1 launched at under $6,000. Tesla's units aren't for sale to outside buyers at all, and even Musk's long-run target of roughly $20,000–$30,000 sits above what Unitree already charges — with near-term build costs estimated far higher. That isn't a pricing disadvantage so much as a different market.

The momentum shows up even where the West is supposed to be strongest. When Nvidia built its first open humanoid reference design on the Isaac GR00T platform, the body it chose was Unitree's H2. An American AI leader is pairing its software stack with a Chinese chassis for the plain reason that the chassis is what ships at scale.

SIGN UP FOR NEWSLETTER

Focusing on the Wrong Catalyst?

Most coverage treats the magnet shortage as the problem. It's better read as an accelerant: an export squeeze doesn't just deny one side a component, it hands the other a head start — and head starts in manufacturing don't rewind.

Chinese makers have spent two years building at volume, and volume is what drives cost down the learning curve — a descent that doesn't reverse. Tesla won't close the cost gap just because magnets start flowing again; by the time it can mass-produce Optimus, Unitree and its peers will be further down the curve still.

The obvious rejoinder is that the West's edge was never hardware but AI — where the value will ultimately sit. It's the strongest case for optimism, but a shakier one than it looks. Software is maturing on the Chinese side too (Unitree trained its autonomous routines on the same foundation-model tooling now spreading everywhere), and if the reference hardware everyone builds on is Chinese, the "brain" advantage has to be large and durable to outweigh a body that's cheaper, better understood, and already deployed. Betting that software rescues a hardware deficit is a real bet, not a foregone conclusion.

What to Watch

Spot prices for neodymium-praseodymium will get plenty of attention, but on their own they don't diagnose much. The more telling signals are downstream:

- Whether MP Materials' output ever reaches robotics customers beyond Apple once shipping begins in 2027.

- Whether Optimus can hit its 2026 targets once the magnet constraint eases — or whether the shortfalls persist, revealing that magnets were never the binding limit.

- Whether other Western players follow Nvidia's lead and simply build on Chinese hardware.

Resolving the magnet problem is necessary but not sufficient. The real question is whether Western makers can close a two-year scaling gap that Chinese manufacturers have already opened — and scaling gaps, unlike export licenses, don't get resolved with a signature.