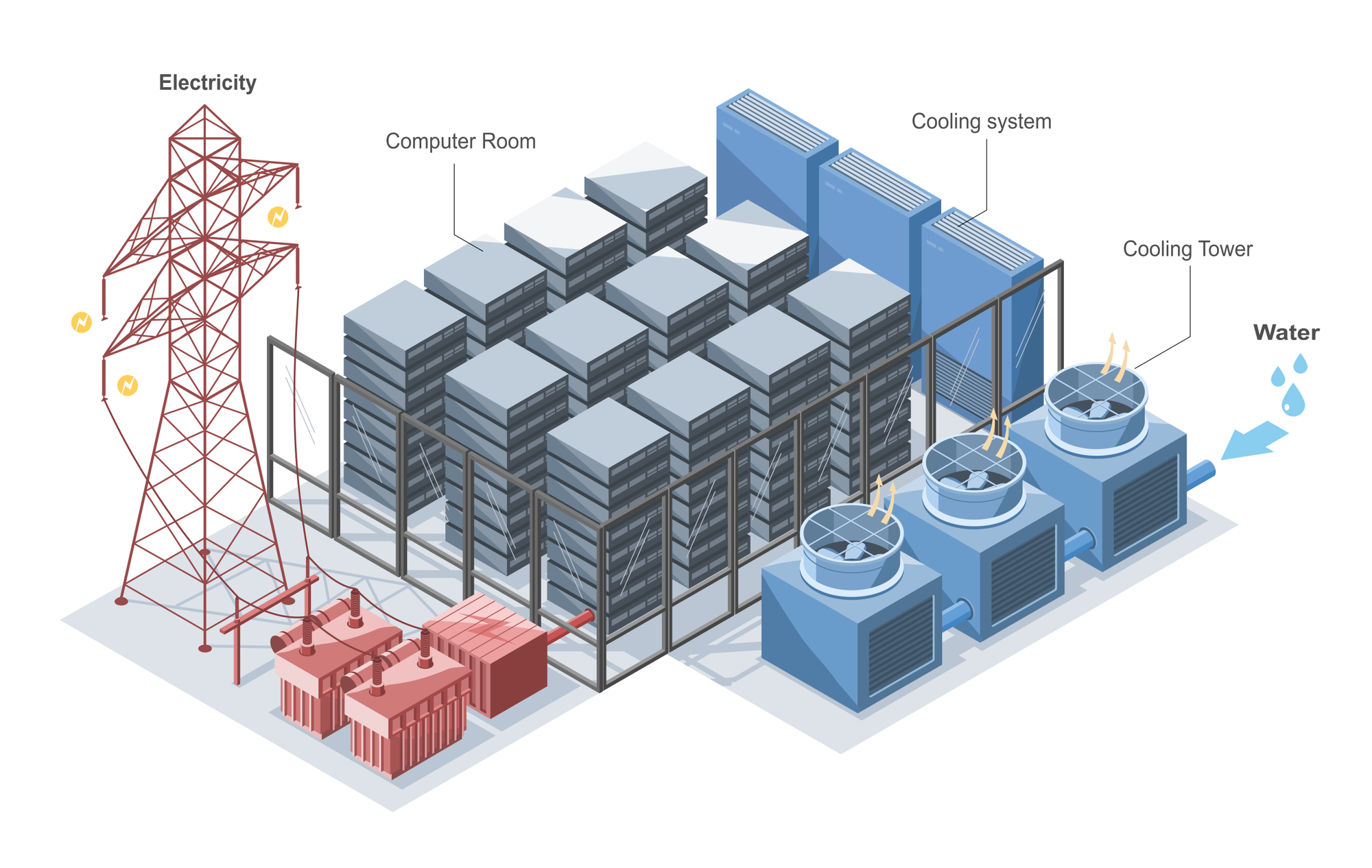

June 24 (World Economic Forum) argued that AI data centers should not be treated just as a electricity drains, but also a flexible energy system asset. It may reshape power price, grid investment, battery demand and even AI infrastructure evaluation.

The market debate around AI energy demand is moving from “Can the grid supply enough electricity?” to “Who pays for the grid, storage and flexibility needed to make AI growth possible?” This matters to utilities, battery makers, natural gas producer, clean energy developer and any investor pricing the next phase of AI capital expenditures.

By 2030, what will matter more for AI companies? (select all that apply)

Robin Zeng, Founder, Chairman and CEO of Contemporary Amperex Technology (CATL) claimed that data center energy demand is not large enough to overwhelm a mature grid, at least in China. In his view, the harder question is not absolute power supply, but how that power is sourced, stored and managed. Also a broader idea has been highlighted: data centers may eventually become flexible grid assets. Buying power when prices are low, using storage to smooth demand and may returning power or flexibility back to the system.

Therefore the AI energy debate is shifting from whether data centers can get enough electricity to whether companies can turn that electricity into measurable productivity, lower operating costs and durable economic value.

Before, the basic logic underlying the demand of AI energy is: more models then more data centers equal more electricity. But the phase next will be around yield. Because if every new megawatt of AI power only produces more experiments, duplicated workflows and higher cloud bills, investors or even the whole marker will query weather the AI CapEx cycle is being mispriced.

Regulation in China dictates that all new data centres must employ 80% renewable energy, a situation that is accelerating research into grid stability and battery technology, with energy storage a key issue.

Thus, AI’s energy cost is no longer just a utility bill. It is becoming part of operating strategy. Robin Zeng said CATL is already using AI systems to buy electricity that generating electricity-bill savings of about 30%.

According to Asia’s Human-led AI Opportunity(June 2026) – 77% of organizations in Asia have adopted advanced AI, but fewer than one-third report achieving widespread and sustained value. Only 20% have reconfigured end-to-end processes around AI, and just 8% have adjusted job roles or decision responsibilities accordingly.

That means Asia is not lacking AI enthusiasm. It is lacking conversion. Many organizations are buying AI capability before they have redesigned workflows, accountability structures and decision rights. In other words, AI adoption is moving faster than the business systems needed to make AI productive.

This is a strong market signal, as it makes the energy debate more financial than it first appears. If AI infrastructure keeps expanding but companies fail to redesign their workflowsIf AI infrastructure keeps expanding but companies fail to redesign their workflows, electricity demand will rise faster than AI returns. That would make data center power a cost center not a productivity engine.

In the past several years, market is pricing the physical AI stack: semiconductor, data center, cooling, storage, grid connection etc. But the next evaluation gap may come from operational stack, which company can redesign work quickly enough to run AI infrastructure into AI operational leverage.

WEF’s separate analysis of AI investment points in the same direction. It argues that many large organizations have not yet seen the returns as they expected from AI spending, not because the technology failed, but because investments often went to the wrong layer. When AI used as a simple productivity assistant may increase efficiency of individual workers but hard to compress the entire workflow. The real value is in redesigning multi-step processes across operations, risk, supply chains and regulated decision-making.

That distinction is crucial for markets. If AI remains a tool layered on top of old processes, companies may face rising energy, software and cloud bills without corresponding productivity gains. If AI is embedded into core workflows, the same electricity cost can support lower cycle times, fewer errors, faster risk review and higher operating margins.

Asia is a particularly important test case because it combines industrial scale, dense digital adoption, large labour markets and very different national AI strategies. WEF notes that China is pushing AI into industrial transformation; Japan is emphasizing reliability and institutional assurance; Singapore is pairing AI investment with governance innovation; India is building momentum through digital public infrastructure and sector-level applications.

Which country will be the first to turn AI adoption into measurable productivity gains successfully?

That diversity creates a useful market map. China may test whether AI, batteries and industrial systems can be integrated at scale. Japan may test whether trust and reliability become competitive advantages in high-stakes AI deployment. Singapore may test whether governance can accelerate rather than slow adoption. India may test whether public digital infrastructure can help AI scale across services, finance, healthcare and government delivery.

The energy aspect runs through it all. And the victory condition may not depend on who uses the most electricity for AI but who turns AI electricity into the most useful output.

This means battery, flexible demand and storage are part of the AI productivity stack. If AI can forecast power prices, shift workloads, optimize storage and reduce electricity costs, then energy management becomes a source of margin improvement. If not, data-center expansion risks becoming a race to build expensive infrastructure before the business case is fully proven.

Therefore the AI trade should be judged not only by CapEx growth but also by operating conversion. Are companies reducing workflow bottlenecks? Are they changing decision rights? Are they using AI to improve energy procurement? Are they redesigning processes around AI, or merely adding AI tools to unchanged organizations?

Will AI energy management become a major source of enterprises margin improvement?

The next phase of the AI market may be less about “how much power does AI need?” and more about “who can produce the most value per watt?”

That is a harder question to price. But it may be the one that separates the real AI winners from the companies simply paying higher electricity bills.

source:

- Why the world's biggest battery maker isn't worried about AI's energy demand, June 24,2026 https://www.weforum.org/stories/2026/06/how-and-why-we-should-be-rethinking-ai-s-energy-usage/

- Asia’s Human-led AI Opportunity: A Framework for Transformation, June 22, 2026 https://reports.weforum.org/docs/WEF_Human_Centric_AI_Transformation_in_Asia_2026.pdf

- Why human roles matter for Asia's AI transformation, June 24,2026 https://www.weforum.org/stories/2026/06/why-human-roles-matter-asia-ai-transformation/