Following the June 17 signing at Versailles of the US and Iran memorandum of understanding, the market reaction was immediate: oil prices fell, Asian equities rallied, and traders began to price a partial reopening of the Strait of Hormuz.

Crude oil prices fell over 4%, while Asian benchmarks surged, responding positively to a conflict that had devastated supply chain through the Strait of Hormuz for over three months.

However, what is not being discussed enough is the fact that transit resumption across the Strait does not equate to normalization. There are a lot of factors at play here which alter the meaning of normalization in its current context.

Perhaps the biggest number that should be highlighted after June 18 was 25 - the total number of ships traversing the strategic passageway following the implementation of the US-Iran MoU.

That is the number of commercial crossings through the Strait of Hormuz on the first full day following the MoU at Versailles, France. While it does spell recovery at face value, putting things in context moves it somewhere between recovery or paralysis.

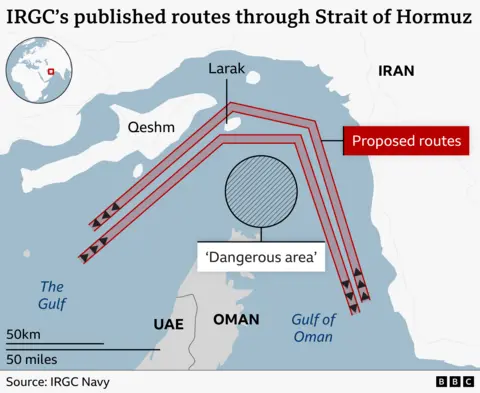

Before the war, around 125 commercial vessels navigated through the international route every day, carrying nearly a fifth of the world’s seaborne and a quarter of its LNG.

Of most of the crossings, a majority were Chinese-flagged tonnage, clearing a backlog – something that can hardly qualify as recovery. While the Strait is legally open, it does remain commercially constrained.

Honestly Pricing the Gap

The real story is the real gap between “open” and “normal” which Polymarket seems to be one of the few platforms correctly pricing. The mistake made by everyone or more precisely, the interpretation being in correct is based around a single diplomatic event which resulted in a signed deal, a lifted blockade and ships passing through like they were at the start of the year. However, the market isn’t actually doing that. There are at least three different definitions of normal floating at the moment, within a live forecast of which barrier is more restricting. Reading these contracts correctly will allow for a much clearer picture of what could potentially happen next.

The Market is Focused on Barriers, Not PR

Take for instance a contract that anchors everything – Strait of Hormuz Traffic Returns to Normal by End of June?

The near-term contract has traded at low odds, while later-dated markets have priced normalization materially higher. It is a yes only if IMF PortWatch’s seven-day moving average of transit calls comes in at 60 or higher, a threshold that matters more than the price. Bear in mind, that only figures reported by PortWatch count.

It is pertinent to mention here that 60 transit calls is still far lower than the baseline pre-war numbers.

Before the war began, throughput was between 90 to 120 a day. We can safely assume that the contract’s definition of “normal” reflects a major shift from what normal was considered before the war began. Even the most bullish bets on the board haven’t priced a return to previous baseline figures. All we can see is a partial recovery which seems to be the “new normal”.

We can also take a look at the structure the market has built across future events. The July 31 normalization contract for example, still has a fair chance of coming through even though it was opened on May 11 when there was a likelihood of the conflict not settling down following Trump's pessimistic views on a ceasefire deal with Tehran.

However, the most unfiltered or cleanest contract around this discourse is the one which delves into the mechanics of the normalization based on a critical regional player being convinced to play ball.

The contract currently has an extremely chance of going through and is highly dependent on Iran allowing unrestricted commercial navigation by June 30.

The most recurring them across these contracts is how the discourse has been about lifting of restrictions and tolls, along with permits to allow ships to move freely. Collapsing these elements into a single question linked with the Strait getting back to normal, makes for a skewed analysis.

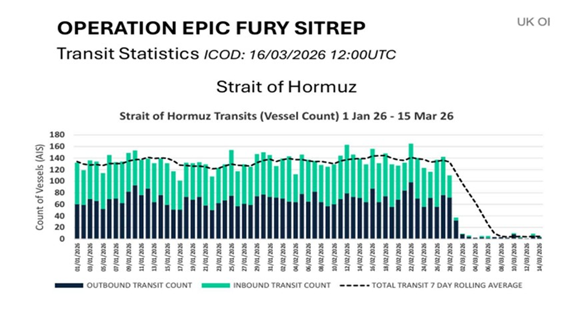

The near-term “no” on most of these contracts can’t be simply filed under pessimism. It is basic math. With commercial transits barely running at around 5% to 10% of pre-February levels, chances of moving a seven-day average to 60 within days seems impossible.

But another interesting question here is why this number can’t be reached fast enough?

To begin with, an early surge of traffic should be attributed to backlog and not categorized as recovery. During the blockade, around 230 tankers were trapped inside the Gulf. By March 2, around 247 vessels, representing around 5% of global tanker dead-weight tonnage (DWT) capacity, remained stranded in the Middle East.

The first thing that has been happening and will probably continue to happen in the next few weeks is a backlog event where previously stranded tankers will be making the crossing. If we inspect this in more granularity, that number shouldn’t really be counted under “recovery or normalization”.

Physical Constraints Transcending Diplomacy

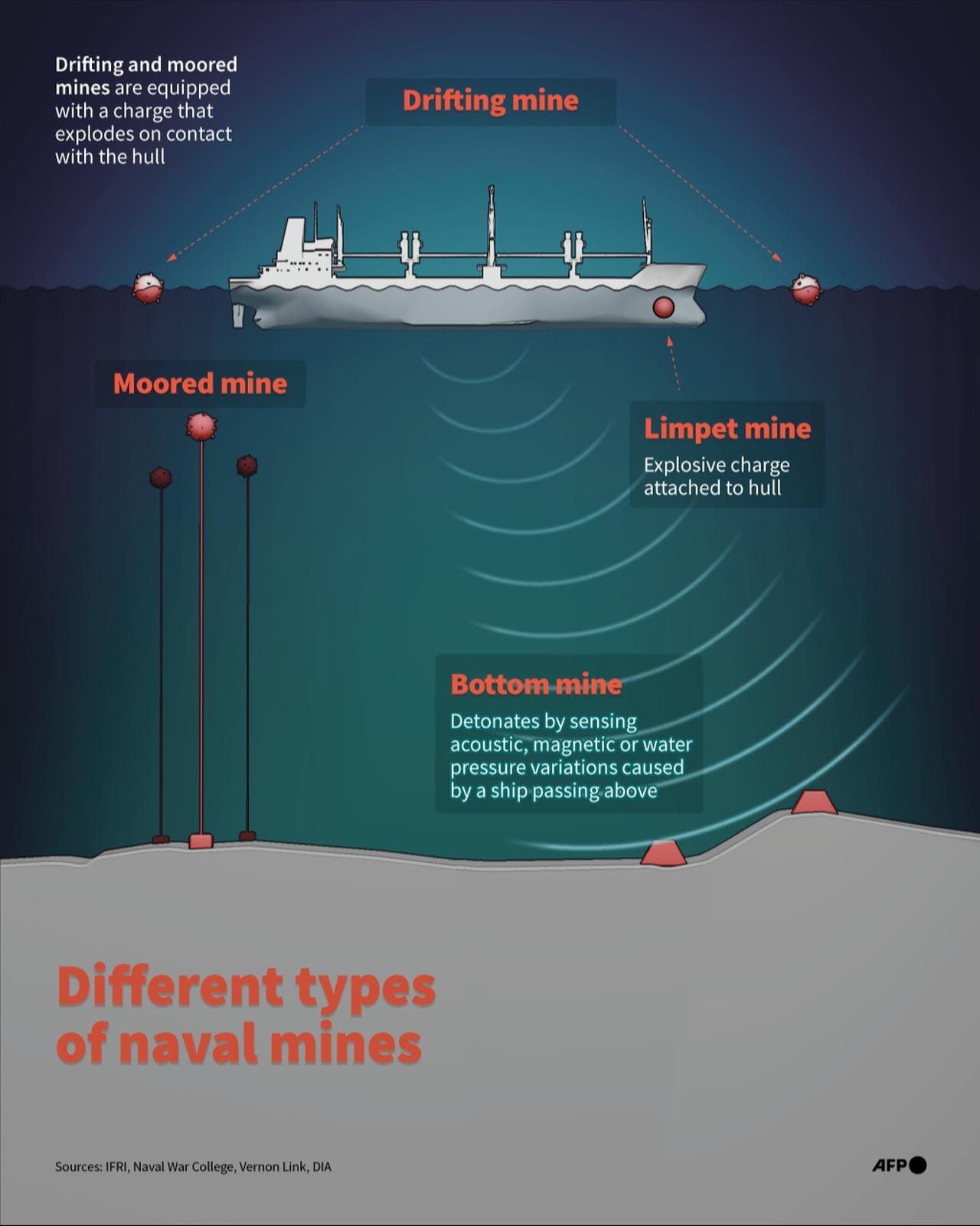

One critically binding constraint at the moment is something that is completely agnostic of diplomacy. The physical element of this is hard to ignore. During the war, Iran dropped several mines along the Strait, which further impacted an already-disrupted supply chain situation. To date, these mines have not been fully cleared, thus making transit risky. While markets can always reprice MoU signings in minutes, it can’t do the same for a minesweeping operation that requires time and resources.

Another key element here is insurance and war-risk premiums. Before the conflict began, war-risk premiums were around 0.15% to 0.25% of hull value, or at least $150,000 for a large crude carrier. At the peak, they even reached 8%, meaning that for a single transit, a tanker had to pay at least $3 million. Premiums do not drop off once a deal is signed, they only fall once there is a sustained record of risk-free and incident-free passage, dictating an underwriter’s sentiment. And with the IRGC firing warning shots on June 19, everything was reset on that front.

Will the US and its Allies Clear the Mines by July 31?

A Barrier Currently Not Priced

Another constraint that outweighs diplomatic wins and agreements is the flags under which stranded and not stranded tankers are sailing.

Iran’s newly-crated Persian Gulf Strait Authority has become a compliance issue because it is tied to permission, routing, fees, and safe-passage arrangements. Even if ships can physically transit, U.S.-linked or sanctions-exposed operators may face legal and compliance risks if passage requires dealing with a sanctioned Iranian authority.

The measure effectively fences out US-linked or affiliated entities who would want to avoid sanctions, which is also why the early “recovery” is dominated and represented mostly by Chinese-affiliated tankers.

While the market can measure recovery, it cannot measure the composition of the recovery, which is where the real normalization question exists.

On top of that, there’s a serious challenge of data accuracy as well. IMF PortWatch has explicitly revealed how its data has been impacted by GPS jamming, AIS spoofing and vessels going dark around the Strait. The instrument, which is the actual data, is being degraded by the conflict it is measuring.

Looking for a Cleaner Bet

An contract resolving positively by December is essentially taking stock from two events; physical recovery and the viability of an interim deal. The MOU window closes around August 17, with nuclear terms considered a key sticking point, along with the Lebanon ceasefire clause which has already been violated a few times. The collapsing of the deal could likely re-close the Strait.

Thinking beyond the normalization markets is a much cleaner route. The possibility of Trump restarting Project Freedom at a specific date is another great contract that could signal whether the deal has failed or not. It carries more weightage since it resolves on a political decision rather than relying on a potentially inaccurate shipping metric.

Tracing the Mispricing

The July normalization event appears to be too high, with Kpler projecting only 40 transits a day within 30 days, almost half of the pre-war numbers. Moreover, the projections are conditioned by no setbacks during the negotiations between the two parties. We’ve already see quite a few of those already so the supply-chain principles are tilted towards the No side.

While the contracts resolving by December seem much more practical, they don’t take into account the potential of things going south by August 17.

Will the Strait of Hormuz Daily Transit Increase to Pre-War Levels by Aug. 18?

What to Watch Out for in the Coming Days?

There are a few catalysts that will have a bearing on all contracts relevant to the Strait of Hormuz normalcy plan. A mine-clearance milestone will have a bearing on everything. Meanwhile, a Western-flagged tanker in transit with no fee will define resolution. However, anything that goes against the Lebanon clause is likely to cause friction.

The actuarial events here are the reopening of different chokepoints, not the diplomatic overtures. While presidents can announce the opening of the passage, it is the underwriters who decide whether the situation has normalized or not.

At present, Polymarket’s spread if observing the underwriters and for now, it seems the latter side isn’t convinced yet.