People used to predict a great future for prediction markets. In 2008, 22 economists, including the Nobel laureates Kenneth Arrow, Paul Milgrom, Thomas Schelling, Robert Shiller and Vernon Smith, wrote a two-page manifesto in the journal Science calling them a “potent research tool” that must be freed from “unnecessary government restrictions.”

They cited “mounting evidence” that such markets could produce more accurate forecasts than conventional methods:

“Prediction market prices can be used to increase the accuracy of poll-based forecasts of election outcomes, official corporate experts’ forecasts of printer sales, and statistical weather forecasts used by the National Weather Service.”

In 2004, the University of Michigan’s Justin Wolfers, one of the signatories, co-wrote what is still the most widely cited paper in the field, showing that betting markets persistently forecast presidential elections more accurately than pre-election polls. Such markets had been around for centuries — in 16th-century Rome there was even a flourishing market to identify the winner of papal conclaves — and were consistently successful. But at the time state gambling laws formed “significant barriers” to “vibrant, liquid prediction markets” in the US.

The manifesto said:

“The first step in helping prediction markets deliver on their promise is to clear away regulatory barriers that were never intended to inhibit socially productive innovation.”

Their idea went nowhere. In 2013, US regulators even closed off Americans’ access to Ireland-based Intrade, then the biggest prediction market operating in the US. Trading on political outcomes continued for small stakes on the non-profit exchanges run by universities and licensed by the Commodity Futures Trading Commission (CFTC).

Then came an October 2024 appeals court ruling that futures tied to the outcome of the following month’s congressional election offered by Kalshi Inc., a New York-based futures exchange, were not gambling, and that the CFTC should not block them. Prediction markets have boomed ever since, led by Kalshi and its chief rival Polymarket, also based in New York, which operates a blockchain-based betting platform from Panama.

But in the last few months, academic research has suggested the great experiment is not going as the manifesto writers had hoped. The good news is that the markets generate accurate political and economic forecasts. The bad news is that the costs — particularly the harms done by gambling — are sizable.

The economists wanted markets devoted to matters of public interest, with stakes limited to $2,000 ($3,000 in today’s dollars). The markets Kalshi and Polymarket have built to date look very different. Wolfers himself laments that “the future we are in isn’t the future I imagined.”

The Prediction Market Boom

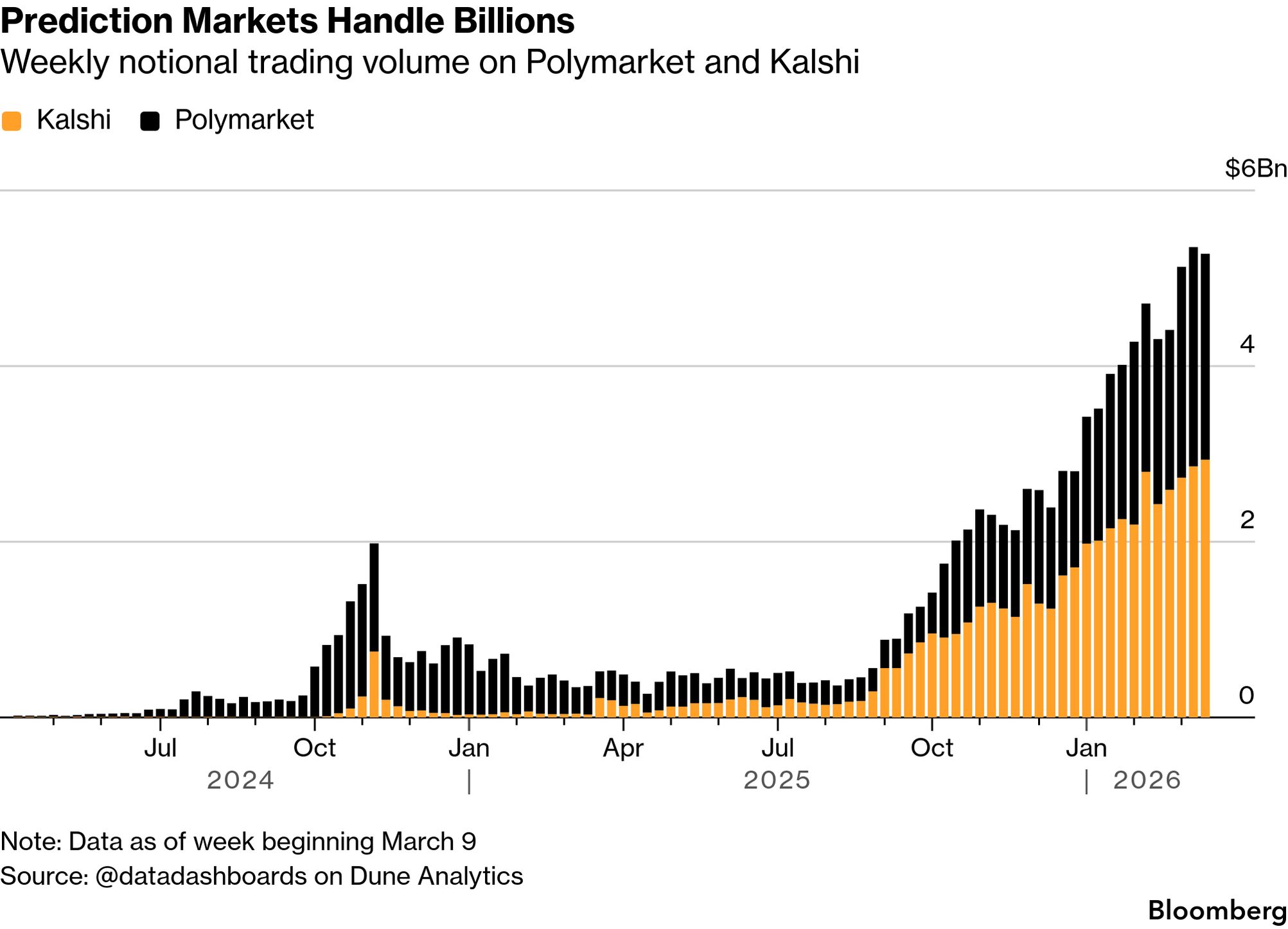

Since October 2024, Kalshi — slogan: “Trade on anything” — and Polymarket have enjoyed parabolic growth.

The crypto analytics group TRM Labs shows that monthly trading on these and other prediction markets rose from $1.2 billion in January 2025 to more than $20 billion a year later. The face value of bets is now close to $30 billion. According to Bank of America, Kalshi is the fastest growing non-AI company; in March 2026, it raised $1 billion at a $22 billion valuation. Polymarket is currently looking to raise funds at an implied value of $15 billion and is reportedly seeking regulatory approval to operate its main exchange in the US.

Removing regulatory barriers has sparked innovation, but not the kind the Nobelists had in mind. They proposed that CFTC-regulated markets would “presumably not include contracts on the outcomes of sports events” — but sports accounts for more than 80% of Kalshi’s trading. Dan Schwarz, who set up Google’s internal prediction market, describes Kalshi as “effectively a sports gambling website with a small prediction market attached.”

On any day, if you go to Kalshi or Polymarket’s home page, you are confronted with chances to bet (through a futures contract) on the results of sports games.

Kalshi, in an emailed statement, distinguished between games of pure chance — like roulette and blackjack — and activities where speculation has social value. Sports outcomes can have tangible effects on industries and local economies, and so sports contracts have, in the company’s estimation, “more than enough social utility.”

Kalshi also offers so-called “mention markets,” where contracts pay out if a public figure uses a particular word in a speech; this encourages young bettors to watch press conferences with the fervor of spectators at the Kentucky Derby. As the satirist John Oliver documented brilliantly, it’s hard to perceive social benefits.

To limit gambling’s social harms without obstructing political and economic predictions, the professors wanted Congress to set rules:

“Because Congress did not intend the CFTC to regulate gambling, it is important to design new regulations so that socially valuable prediction markets easily qualify for safe harbor but gambling markets do not.”

This didn’t happen. Instead, Kalshi, Polymarket and others have merged the two, and their future now rests on a turf battle between the states, who regulate gambling, and the CFTC, which oversees derivatives markets.

‘It’s Simply a Bet’

Like alcohol, tobacco or pornography, gambling is a vice that will never go away, and which consenting adults should be free to enjoy — within limits set by the public. Precedent is clear that the US Constitution gives states that right.

Prediction markets currently gain a huge advantage over sports betting groups by avoiding state regulation. They don’t pay gaming taxes, which according to Bank of America can reach 33%, and there are still 12 states — including California and Texas — that ban sports betting outright. Prediction markets also get to catch customers at 18, rather than waiting until they turn 21, as required by most states, including even Nevada, before they can legally bet.

The explosion of sports betting, since a Supreme Court ruling in 2018 gave states the right to regulate it, is already causing serious social harm. The New York Federal Reserve found that the number of people under 40 whose loans were delinquent has risen by a full percentage point more in states that legalized gambling than those that didn’t. Among bettors, the number who are more than 90 days late with loan repayments has doubled.

Now both red and blue states want to block what they see as a loophole to addict teenagers to gambling. Utah’s Republican governor says flatly that prediction markets are “illegal” in the state, and its attorney general, Derek Brown, rubbished the notion that they’re not gambling: “It’s simply a bet, dressed up in different clothing.”

However, the federal CFTC is tasked with regulating speculative futures markets, and its new chairman Michael Selig has aggressively asserted jurisdiction. Launching a consultation on new rules for prediction markets, he said:

that these markets… have the integrity and resilience and vibrancy that our derivatives markets deserve. To those who seek to challenge our authority in this space, let me be clear: We will see you in court.”

Now that Congress has missed the chance to draw the line, courts are doing so. The Third Circuit appeals court on April 6 ruled in Kalshi’s favor against a New Jersey attempt to regulate its contracts as sports betting, on the basis that the law gives the CFTC the job of regulating contracts that hedge economic outcomes. On its face, it would seem impossible for anyone to hedge a sports result without athletes betting against their own team, which has been prohibited in US life since at least the 1919 World Series. But over a strong dissent, the appeals judges argued that sports outcomes can have “financial, economic, or commercial consequences” for people such as “sponsors, advertisers, television networks, franchises, and local and national communities.” The ruling means that it will now almost certainly fall to the Supreme Court to define gambling.

Defining Gambling

The boundary where investment and speculation cease and gambling begins is notoriously difficult to define. Few can improve on Justice Potter Stewart’s infamous statement in a 1964 opinion that he could not define hard-core pornography “but I know it when I see it.” And to quote the Better Markets advocacy group, which steadfastly opposes liberalizing the sector: “Everyone should go on Kalshi and see for themselves whether it looks like sports betting or derivatives trading.” Kalshi’s advertising makes it almost impossible to distinguish its offering from sports gambling sites like DraftKings and FanDuel.

The first retort is that Kalshi, Polymarket and the others are structured as futures markets, with different traders taking either side of the trade. No house is guaranteed to win overall as in a casino.

But academics are chipping away at that claim. Kalshi and Polymarket need market makers to offer contracts and provide liquidity. In stocks, market makers protect themselves with the bid-offer spread, or gap between the prices at which they buy and sell. But in prediction markets every contract ends at either zero or 100 cents on the dollar, and the massive move when the contract settles will swamp the bid-offer spread. In particular, it should be impossible to get markets in contracts where some bettors may have inside information off the ground.

Research by Stanford University analyzing 41.6 million trades on Kalshi explained this conundrum by finding that the supply of optimists — Stanford’s Robert Bartlett, who led the research along with Maureen O’Hara of Cornell, told me that the words “mugs” or “suckers” would also be appropriate — is so great that market makers do as well as the house would in a casino.

“If you didn’t have the optimists subsidizing it, you wouldn’t have a market as market makers wouldn’t be able to make money,” Bartlett says. This is particularly true of the most contentious “single name” contracts, where some must have better information than others. These are distinct from “broad” contracts on which nobody has decisive private knowledge, such as where the S&P 500 will close or what the next CPI print will be.

On single-name contracts, makers win 63.4% of the time according to their study, more than making up for the bigger losses they suffer when they lose. Winners are confident, possibly because of inside knowledge — but so many mugs bet against them that it’s still possible to make a market. The gap is much narrower in broader contracts, which Bartlett views as “more of a fair bet.”

That looks like potent evidence that current regulation is insufficient. The political risk consultant Ian Bremmer, who founded the Eurasia Group, puts this in trenchant terms:

“Every dollar won by an insider comes directly from the pocket of a schmuck who’s under the impression they’re participating in a forecasting exercise. If a few insiders dominate a market, the suckers taking the other side of their trades will keep losing and eventually run out of money.”

What Bartlett calls the “optimism tax” allows insiders to profit. “These people derive a lot of utility from this betting, just as they do from horse-racing, but this isn’t the market that Wolfers and the others had in mind,” he says.

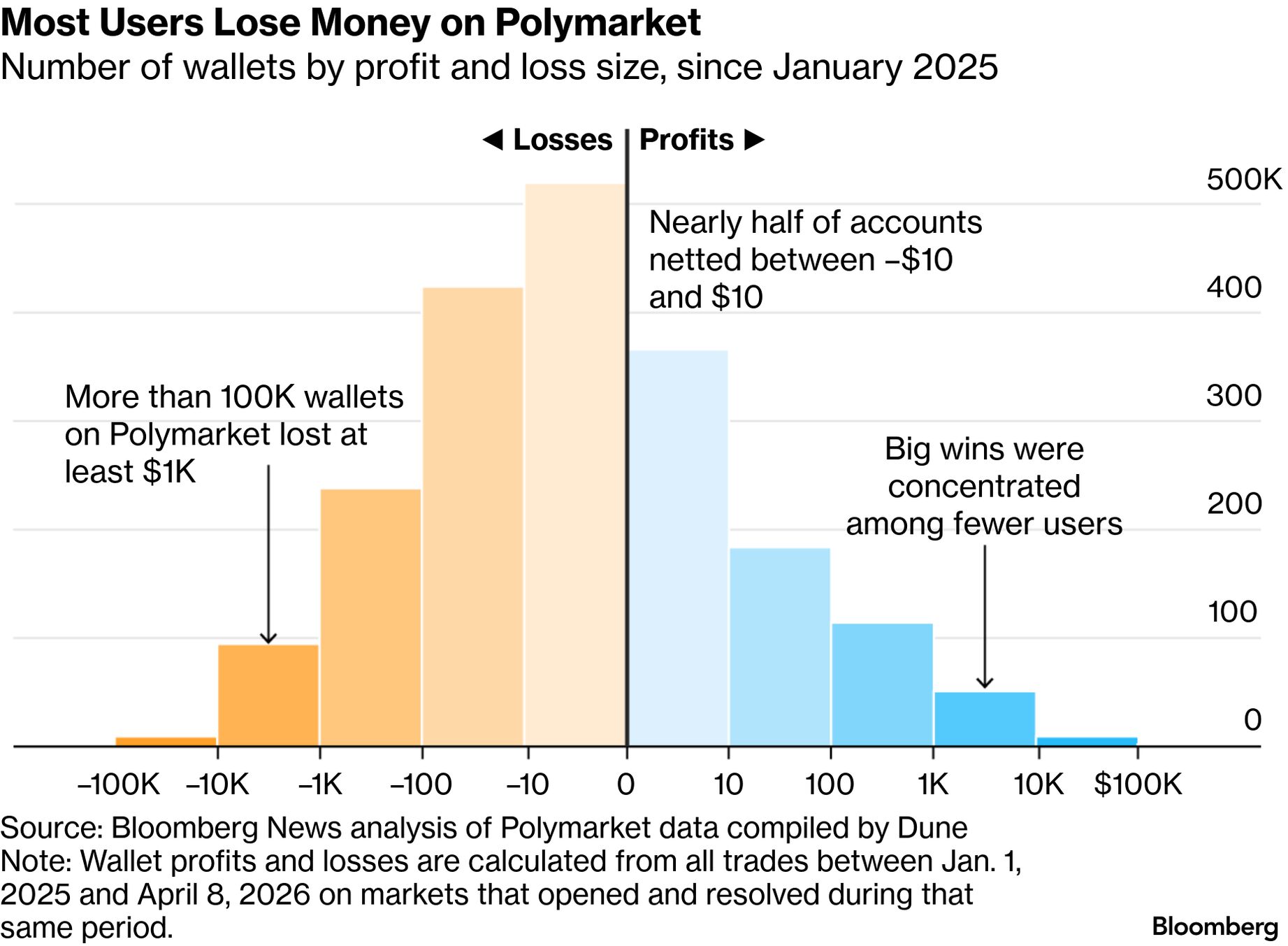

Researchers are now confirming that a great majority of accounts are losing money. Analysis of Polymarket returns by Bloomberg News found that more than 100,000 accounts lost at least $1,000 since the start of last year, almost twice the number that made that much. Most profits were made by “a small group of automated bots, with everyone else losing $131 million in aggregate,” according to Bloomberg’s analysis. Similar analysis of Kalshi by The Wall Street Journal found that “everyone loses — except a few sharks.”

Research led by the University of Toronto shows that since 2022 around 69% of traders on Polymarket lost money, with three quarters of the profits going to the top 1%. Researchers at Columbia University and the University of Haifa amplified this by crunching through 93,000 distinct markets on Polymarket looking for anomalies where insider trading appeared to be in play — and found approximately $143 million in “aggregate anomalous profit” in two years.

Polymarket disputes the idea that most of its users lose money. Eighty percent of users have a profit or loss within plus-or-minus $100, it said in an emailed statement. Those returns “split roughly evenly between gains and losses,” the company said, with “materially more large winners than large losers” and “with fewer than 2% of users recording losses greater than $1,000 compared to more than 5% posting winnings above $1,000.”

Still: If this isn’t gambling, it sounds a lot like it. The odds are stacked against the public just as much as they are in a casino. Why not, then, regulate them as casinos?

Both Kalshi and Polymarket argue that prediction markets are more accessible than traditional financial markets, allowing everyday users to participate in subjects that matter to them rather than esoteric asset classes dominated by professionals. Kalshi said that a “skill gap among participants” exists in all financial asset classes, while Polymarket said that “every competitive market rewards participants with greater experience, skill, and faster execution.”

The best defense of these markets, however, lies in the benefits the economists laid out in 2008.

Hedging

Hedging is a public good that justifies extremely speculative behavior. For example, many traders in oil futures have no direct stake in oil. They are placing bets much as Kalshi bettors bet on the World Series. But their presence allows exporters and oil producers to manage risks and lock in prices. The hope is for big, liquid prediction markets to allow a company that stands to be harmed if Candidate X wins an election to buy insurance.

This remains largely theoretical, and blatantly doesn’t apply to many, if not most Kalshi and Polymarket contracts. Nobody needs to hedge against the risk that the broadcasters say “Alley-oop” at the next Timberwolves vs. Spurs basketball game (a Kalshi market on which $25,000 is at stake at the time of writing).

But the appeals courts judges ruled that sports were economically relevant, and in its statement Kalshi says that institutions are hedging commercial risks related to sports outcomes on its platform:

“For example, via sports insurer Game Point Capital, teams are hedging against contract incentive payouts. In the contracts of many coaches, there are bonuses that trigger depending on the stage of the post-season the team is able to reach. Teams that do not want to suffer the full impact of the bonus, or simply do not want to deal with the volatility, are hedging these outcomes via Kalshi.”

Skepticism remains. “They are not taking out insurance,” Wolfers told Australia’s Financial Review, of the typical market participant. “They’re taking a bet.” He sees little sign that many people are using these markets to hedge. But there are possibilities for the future. Koleman Strumpf, an economist at Wake Forest University, laid out the potential of real estate contracts:

“A homeowner who plans to sell their home at a future date could use a prediction market contract linked to local real-estate conditions to reduce their uncertainty and lock in a price. This is distinctive from pure gambling, such as state-run lotteries, which do not provide such social benefits.”

Such contracts are already traded on both Kalshi and Polymarket but remain embryonic and lack the volume to hedge even the price of one house (the volume on Kalshi’s contract to predict April US existing home sales is $3,600). It’s hard to imagine them ever reaching the scale to allow large companies to hedge big macroeconomic risks.

Macro-Accuracy

The Nobel laureates’ other critical argument concerned accuracy, built on a rich tradition of free-market theory dating back at least to Friedrich Hayek. Markets, where people have skin in the game, concentrate minds and synthesize the existing wisdom better than anything else. Tarek Mansour, CEO of Kalshi, summons Hayek in arguing for his company’s services:

“[Hayek] argues that information is fragmented, local, dynamic, and often hidden. No government or central planner can ever fully possess it, which makes them inefficient resource allocators. He proposes markets as the solution: knowledge is decentralized and prices are how society aggregates it. This idea is the intellectual foundation of modern prediction markets.”

The accuracy of Kalshi and Polymarket forecasts has improved still further as they’ve grown. Barclays equity researchers analyzed the Polymarket contracts quoted on Bloomberg to mature so far this year, and found those with higher trading volume indeed produced more accurate final predictions. “Higher volume does not guarantee correctness,” they said, “but it increases the likelihood that a contract’s price reflects genuine collective beliefs from the broader market rather than noise.”

On big macro-forecasting issues, the Fed found that Kalshi contracts improve on consensus surveys of experts (confirming research by Wolfers and others two decades ago). Kalshi-implied probabilities on inflation and rates are “well-behaved, responsive to news, and comparable in forecasting accuracy to established benchmarks such as the Survey of Market Expectations and the Bloomberg consensus.”

No existing financial markets create forecasts on vital measures like GDP growth and unemployment, so Kalshi now offers a unique and valuable service. The Fed even intends to offer daily Kalshi data on the web, to “enable policymakers to easily monitor shifts in investors’ belief in real-time.” This is exactly what the laureates recommended.

Prediction Laundering

There are caveats. Market-based predictions look more solid and absolute than they are, and exist only within the market itself. Unlike oil futures, for example, they don’t allow you to lock in a price to buy a commodity in the real world. This leads to the fear that Kalshi and Polymarket numbers, rather than clarifying diffuse information, could distort perceptions. Academics call this “prediction laundering.”

University of Toronto computer scientist Yasaman Rohanifar coined the term to describe the process by which forecasts are “laundered” into a final prediction. She says this happens in four stages: First, complex situations become yes-or-no outcomes (determined by market administrators, who in structuring real-life complexity to make it tradable arguably behave like Hayek’s dreaded socialist planners). Second, different perspectives are flattened into a single probability. Third, the sway of large traders — “whales” — is presented as “a collective, neutral consensus.” Finally, disputes are ignored — or thrashed out in private on Discord.

A trader Rohanifar interviewed for the research explains the effects:

“It’s funny because once I see a number attached to a possible outcome, it stops feeling like an opinion and more like... real truth. It doesn’t matter who is betting or why. You just see 72% and it feels like that is the truth, even though I know it is coming from... just a mess of guesses and incentives!”

Markets can only be as accurate as the data fed into them. Psychologists have found that when people can measure something and give it a value, this often becomes a belief that they can control it. This was a critique of the widely used Value at Risk models that appeared to reduce traders’ risks to one fixed number, bred overconfidence, and failed spectacularly in the Global Financial Crisis.

Treating prediction market outcomes as revealed truth might similarly lure people into bad decisions. Rohanifar’s remedies include “whale alerts” or “concentration metrics” to flag when a probability is being driven by only two or three traders; displaying a “sentiment map” or confidence intervals rather than a single percentage (Kalshi said in its statement that it is indeed considering rolling out sentiment maps and similar visual displays); and leaving a permanent record of all disputes that happened before a market was resolved.

Drawing the Line

The challenge is to draw a line that allows markets to gauge probabilities on important issues not otherwise traded directly (like the widely cited contracts on when the Strait of Hormuz will reopen) without distorting perceptions or luring the unwary into gambling.

Sports betting might yet provide the funding and scale to allow more worthwhile prediction markets to flourish, much as porn fueled the early internet. Kalshi says there is cross-pollination “from sports markets to other categories like politics,” which it is intentionally fostering. Wolfers, who now argues for ringfencing contracts where there is value in price discovery or fundamental hedging discovery and regulating the rest as gambling (or banning it), concedes that corporate internal prediction markets needed sports to get people interested. “You need that honey to get the bees to come,” he says. “Then the question is how much honey and how many bees do we really need?”

Robin Hanson of George Mason University, another manifesto signatory and a committed libertarian, isn’t bothered by sports bets but fears “a new prudish temperance movement may shut them down, and as a side effect shut down the more promising markets that I’ve envisioned.”

That looks unlikely. With a Supreme Court ruling likely a year or two away, Wall Street is betting the incumbents have enough time to dig themselves in, thanks to the popularity of the sports platform they have already built. “Sports were the catalyst for Kalshi to get to this point, but now it may increasingly have the active users, brand recognition, relationships and financial wherewithal to diversify its growth from here,” says BofA. Bloomberg Intelligence sees prediction-market volume “potentially exceeding $1 trillion annually by 2030,” and reaching $300 billion this year — compared to just $51 billion in 2025.

David Hoppe, founder of San Francisco media law group GammaLaw, draws an analogy with Uber and ride-hailing services. By the time regulation catches up, the services have had “enough time to develop and grow a constituency of people that really liked their service.”

Wolfers agrees that this may already have happened for prediction markets, even though most of their trading “has no redeeming social value beyond entertainment.” He’s left to regret that his research “turned out to be the cover that Kalshi and Polymarket are using in order to buy respectability from the regulators.”