People express their opinions about all kinds of events on prediction markets, from elections, crypto, sports, to the second coming of Jesus and if the earth is flat.

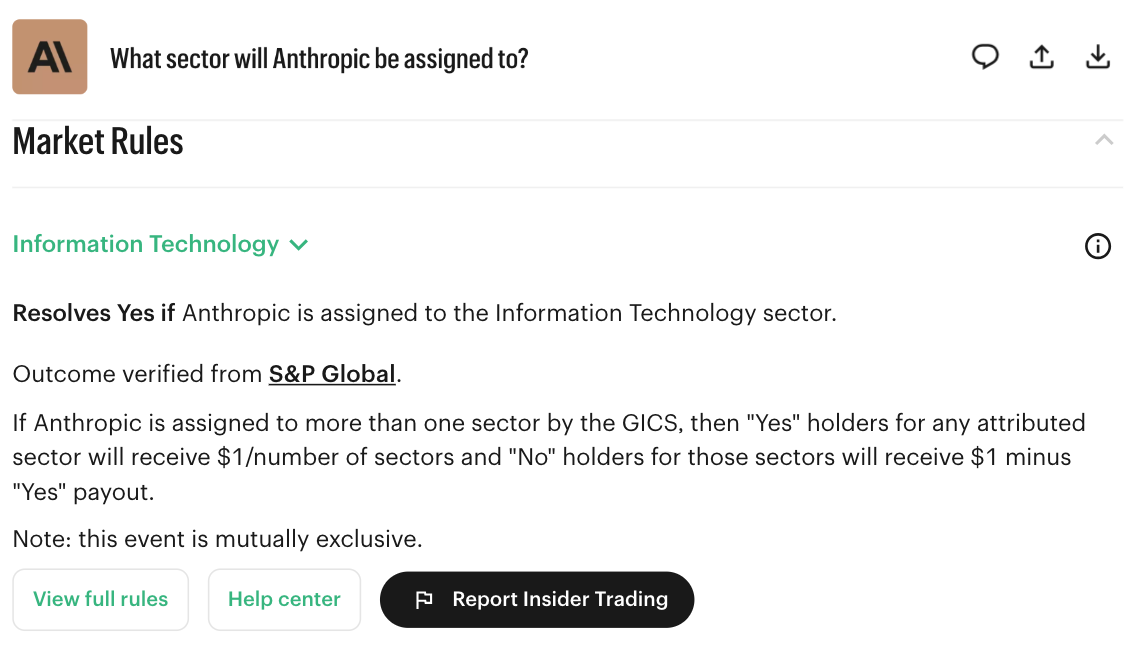

And now, apparently, people are trading on whether Anthropic is "Information Technology" on the market titled "What sector will Anthropic be assigned to?"

As of this writing, the "Information Technology" outcome is shown at 76% chance, together with "Unassigned" at 10% and "Communication Services" at 2%.

At first glance, this Anthropic sector market on Kalshi looks funny. Because the answer seems obvious to most people. Anthropic makes Claude. Claude is AI. AI is tech. So why is this even a market?

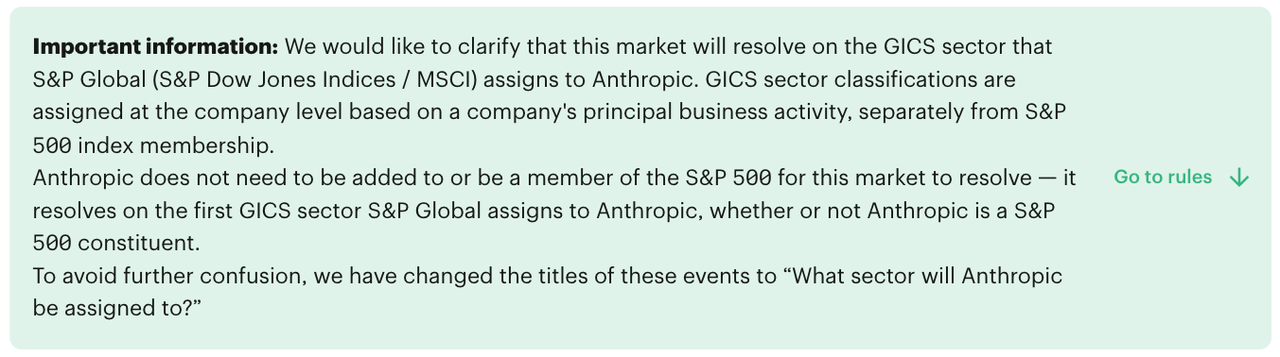

The answer is that prediction markets are not about what sounds obvious in normal language. They are about what the contract actually says. The real question is, "what GICS sector will S&P Global assign to Anthropic before the market deadline?"

Read the rules before having an opinion

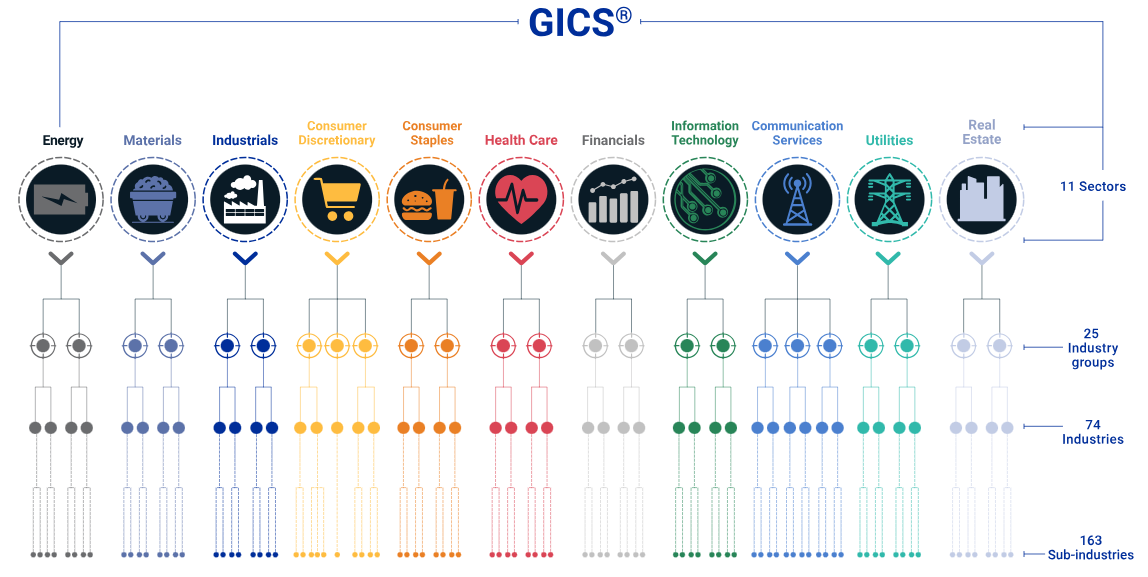

A GICS sector classification is basically Wall Street’s standardized way of putting a company into an industry bucket. GICS stands for Global Industry Classification Standard, a framework developed by S&P Dow Jones Indices and MSCI to help investors compare companies consistently across markets.

It has a hierarchy: a company is assigned to a sub-industry, then an industry, then an industry group, and finally one of the broad 11 sectors, such as Information Technology, Communication Services, Financials, Health Care, or Industrials.

The actual question of the contract is narrower and cleaner: Will Anthropic receive a GICS sector assignment by the deadline Jan. 11, 2028 at 10:00am EST, and if so, which sector will it be?

If Anthropic is assigned to more than one GICS sector, the payout is split across the sectors that receive an assignment. For example, if Anthropic were assigned to two sectors, YES holders in each assigned sector would receive $0.50 instead of the full $1. NO holders in those same sectors would receive the remaining amount, meaning $0.50. Therefore, the contract price should be read as the expected payout of that outcome after accounting for the possibility of split payouts, not simply as the probability that Anthropic receives only that sector label.

In practice, this rule reduces the value of a YES contract if multiple sectors are recognized, even if your chosen sector is technically correct.

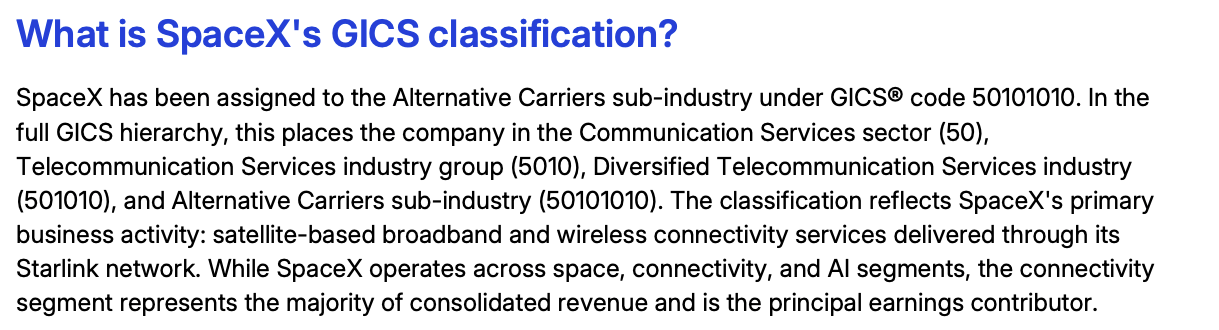

However, GICS is designed as a single-classification system. Each company is assigned one GICS classification at each of the four levels: sub-industry, industry, industry group, and sector. The classification is based on the company’s principal business activity, with revenue usually being the most important factor, while earnings and market perception can also matter.

So even highly diversified companies usually still get only one sector. For example, Amazon has cloud computing, advertising, logistics, streaming, and retail, but GICS still classifies it as Consumer Discretionary, NOT both Consumer Discretionary and Information Technology.

Since the probability of multiple GICS sector assignments appears close to zero, I treat each contract price as approximately equal to the probability that Anthropic receives that sector as its sole GICS sector label.

Does Anthropic need to IPO before getting a sector assignment?

A quick but important answer: strictly, no. Practically, probably yes.

The Kalshi contract does not require Anthropic to IPO. The rules explicitly separates sector assignment from S&P 500 membership.

But in practice, the most likely path to sector assignment is an IPO or another public-market event. For a private company, there is much less public financial information. For a company going public, the prospectus gives the classification providers a clean description of the business, revenue model, risk factors, and financial profile. So IPO is not a legal condition of the Kalshi contract, but it is probably the most important practical trigger.

Thereofre, related IPO markets prices are useful inputs.

The probability tree hiding inside the market

The clean way to price the Information Technology contract is: P(Anthropic Under IT) = P(Anthropic Assigned) × P(Under IT | Assigned).

That looks simple, but it changes the whole analysis.

Kalshi shows: P(Anthropic Under IT) = 76% and P(Anthropic Unassigned) = 10%.

So the market is implying: P(Anthropic Assigned) = 1 - 10% = 90%.

Then the conditional probability is: P(Under IT | Assigned) = 76%/90% = 84.4%.

Then the real market-implied statement is: If Anthropic receives any GICS sector assignment, the market is still giving about a 15.6% chance that the sector is NOT Information Technology.

That is the interesting part. The market is not just pricing IPO timing. It is also pricing a meaningful non-tech classification tail.

Now the job is to ask whether that 15.6% non-IT conditional probability makes sense.

Use related markets instead of vibes

Kalshi has a separate market on when Anthropic will officially announce an IPO, which defines IPO confirmation as one of three things: the SEC declares the S-1 effective, the IPO is priced, or a securities exchange assigns a ticker.

As of this writing, the odds were:

- Before Oct. 1, 2026: 47%

- Before Nov. 1, 2026: 60%

- Before Jan. 1, 2027: 72%

- Before Mar. 1, 2027: 84%

Polymarket has a company IPO market as well. The odds retrieved were:

- Before Sep. 30, 2026: 9%

- Before Oct. 31, 2026: 37%

- Before Dec. 31, 2026: 76%

This gives us a useful timing curve. The market is putting meaningful probability on confirmation or IPO completion within the next few months.

In other words, the market is already treating an Anthropic public listing path as highly plausible before the sector market’s Jan. 2028 deadline on Kalshi.

That view also has a fundamental catalyst. Reuters reported on June 1, 2026 that Anthropic had confidentially filed for a U.S. IPO, calling it a move that put Anthropic ahead of OpenAI in the race to public markets. Reuters describes the typical timeline from initial filing to market debut as roughly 3 to 6 months, depending on SEC review and market conditions.

What sector should Anthropic actually get?

GICS has 11 sectors. The top 2 most likely outcomes here are Information Technology and Communication Services.

S&P describes Information Technology as companies offering software and IT services, plus technology hardware, communications equipment, computers, semiconductors, and related equipment.

S&P describes Communication Services as companies that facilitate communication and offer related content and information through various mediums. That sector includes telecom, media and entertainment, interactive gaming, and companies engaged in content and information creation or distribution through proprietary platforms.

The strongest case for Information Technology is the business model. Anthropic sells Claude access, API usage, enterprise plans, developer tools, and workplace AI products. Claude’s Enterprise plan is designed for organizations that need security, compliance controls, and scalable AI across teams. It includes usage-based pricing, with usage billed separately at API rates, and it supports workplace-tool connectors such as Google Drive, Gmail, Google Calendar, GitHub, Microsoft 365, and Slack.

Anthropic’s product list also includes Claude, Claude Code, Claude Code Enterprise, Claude Cowork, Claude for Microsoft 365, Skills, and other software products.

That sounds much more like AI software + API access + developer tools + enterprise workflow infrastructure than media + advertising + telecom + entertainment.

There is a Communication Services tail, but it is not the base case. The tail argument is that Claude is an interactive information platform. Users ask questions, receive information, generate text, and interact with a proprietary platform. That could make someone squint and compare it to internet platforms inside Communication Services.

But that argument seems weaker than the software argument. Anthropic’s monetization is not primarily advertising. It is not a social network or media distributor or telecom provider. It is selling model access and software-like productivity tools.

This is why the 15.6% conditional non-IT probability looks potentially too high.

In comparison with the OpenAI market

A good way to test a market is to compare it with a similar market.

Kalshi has the same sector market for OpenAI. As of this writing, OpenAI’s Information Technology outcome is shown at 84%. OpenAI’s Unassigned outcome is shown at 13%, and Industrials is shown at 1%.

Now apply the same conditional math.

For OpenAI, P(OpenAI Unassigned) = 13%;

So, P(OpenAI Assigned) = 1-P(OpenAI Unassigned) = 87%;

And, P(OpenAI Under IT) = 84%;

Therefore, P(OpenAI Under IT | Assigned) = 84%/87% = 96.6%.

Compare that with Anthropic: P(Anthropic Under IT | Assigned) = 76%/90% = 84.4%

So the market is implying that, conditional on assignment, OpenAI is almost automatically Information Technology, while Anthropic has a much larger chance of being put somewhere else.

SIGN UP FOR NEWSLETTER

Takeaways

The lesson is simple: read the rules, separate the probability paths, use related markets, and compare similar contracts. The real trade is whether the market is overpricing the chance that S&P calls Anthropic something else from a tech company.

The main thing to watch next is Anthropic’s IPO process. A public S-1, ticker assignment, IPO pricing, or SEC effectiveness would reduce the “Unassigned” risk. After that, the most important evidence will be how Anthropic describes itself in its prospectus: enterprise software, API access, coding tools, and productivity infrastructure would support the IT case.

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.