A recession market should be simple: buy “Yes” if you think the economy breaks, buy “No” if you think it doesn’t. But this one is not so simple.

A slowdown can be real before it is formal. It can hit households, stocks, and confidence before it shows up in the exact data points a prediction market needs. If this gap holds, traders may be paying for the right fear through the wrong contract.

Consumers are spending, but not with much swagger because inflation is doing too much of the work. And bears have fresh material: Gary Shilling is warning that a downturn is almost inevitable, pointing to households paying more to get less, housing still pinned down by high rates, weaker capital spending outside the AI buildout, and stock valuations with little room for disappointment.

The economy may be vulnerable, but the market may be buying the wrong version of the recession trade. Here’s why!

The market is betting on a crack, but the clock matters

For prediction markets contracts to resolve “Yes,” bad vibes are not enough. This Polymarket market is not paying out because the US economy looks weak, consumers feel squeezed, or traders get nervous. The window runs from Q2 2025 through Q4 2026, and it needs one of two things before the deadline: either two straight negative quarters of real GDP between Q2 2025 and Q4 2026, or an official NBER recession call before the BEA publishes its advance estimate for Q4 2026.

The 25% implied probability is a much narrower bet than it first appears. This is more of a timing bet because the slowdown has to show up in the right data, in the right order, before the deadline.

That is the first thing the market may be underpricing, not the recession risk itself, but the friction between economic weakness and contract resolution.

The economy is not booming, but it is not breaking either

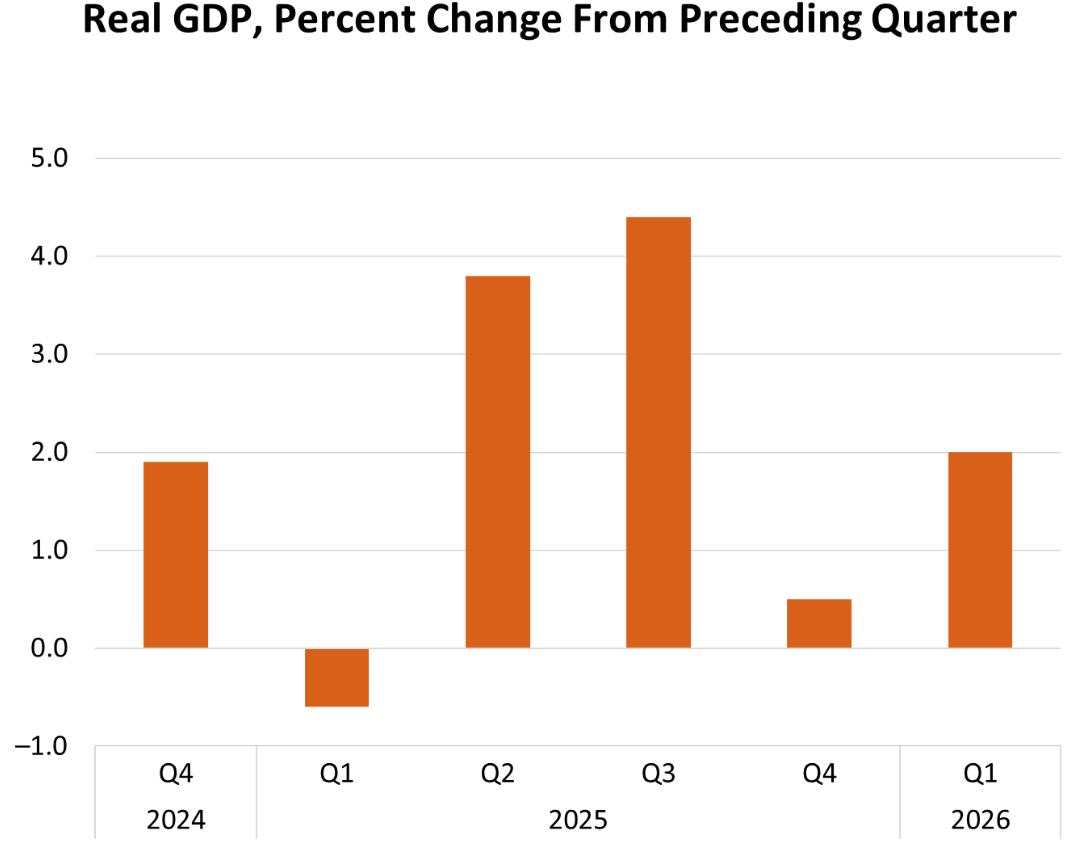

Right now, Q1 made the “Yes” case harder because real GDP grew 2.0% annualized after a weak 0.5% in Q4 2025, so there is no negative-quarter chain for the contract to build on. This is easy to miss if you are focused on recession headlines rather than the settlement path. If this market resolves through GDP alone, the bad prints now have to come in pairs: Q2 and Q3, or Q3 and Q4.

Source: BEA

This is a problem for bears because Q2 does not look broken yet. Atlanta Fed GDPNow had growth running at 3.5% as of May 1. It can move, of course, but that is still a long way from contraction.

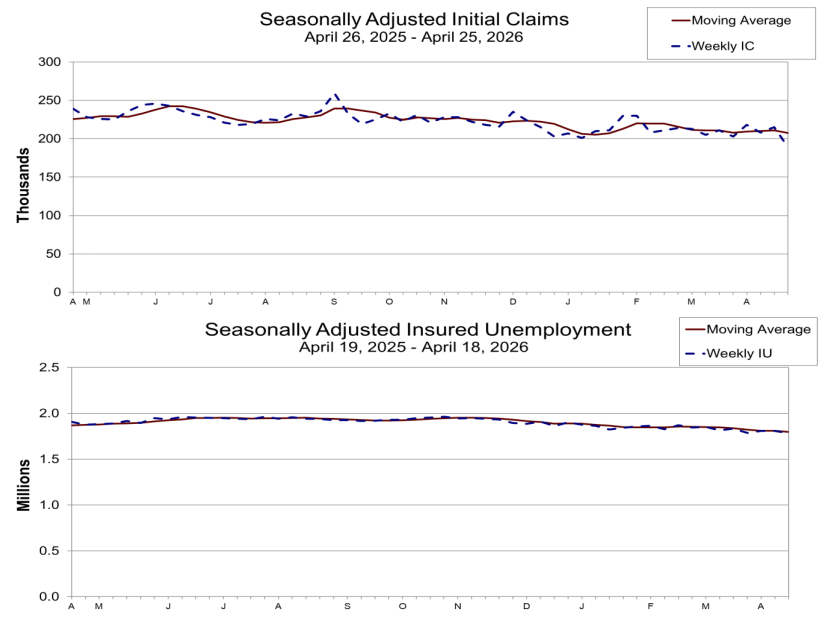

Labor is not helping the recession case either. Payrolls are still rising, unemployment is not flashing a crisis, and jobless claims recently fell to 189,000. This does not erase recession risk, because labor often cracks late, but it does expose the gap in the trade. The economy can weaken before the labor market gives the contract enough proof, so it does put the “Yes” side on a tighter clock.

Source: Department of Labor

The economy can feel worse before it officially breaks. Still, for now, the hard data is keeping the 25% odds on a tight leash.

The case for “Yes”: A slow squeeze?

The economy must get trapped between inflation that will not cool and growth that cannot accelerate.

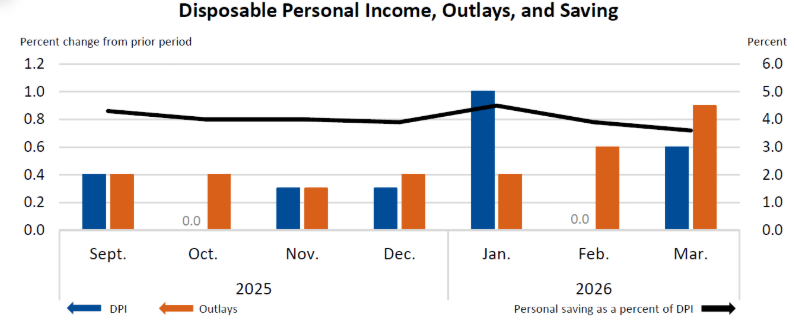

March PCE data gives the shape of it all: consumers spent 0.9% more in nominal terms, which sounds healthy enough. But while spending looked solid on paper, all of that disappeared once prices were accounted for, so households did spend more, but they just did not get much more for it.

Source: BEA

This is the weak spot Gary Shilling is pointing at, and it is the part many can miss until late. His recession call rests on a more basic problem: consumer spending, the ballast of the U.S. economy, has been holding the economy together, and this support looks thinner when real income is slowing and savings are weakening.

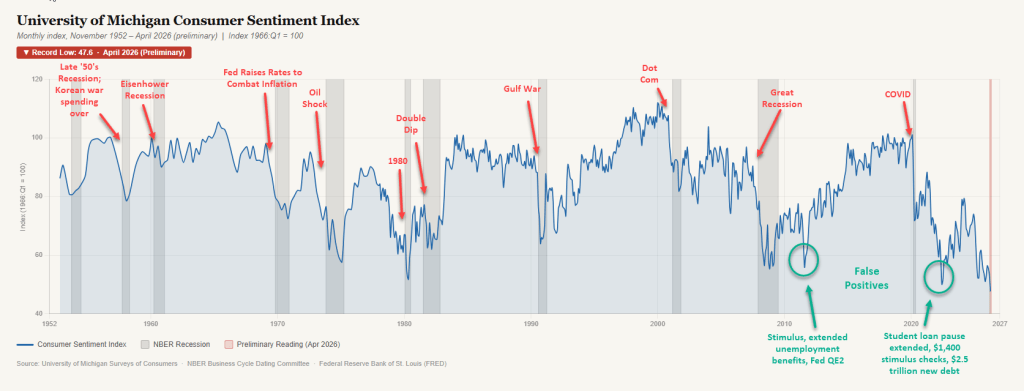

Consumer psychology is flashing its own warning, too. HousingWire points to a sharp drop in University of Michigan consumer sentiment, arguing that the index has historically been a strong recession signal, though it did cry wolf in 2011 and 2022.

Source: HousingWire

Oil risk may be the swing factor, but not in the obvious way

The easy story is that war pushes oil higher, consumers pay more at the pump, and recession odds go up.

But the bigger issue is what oil does to the Fed. If energy keeps headline inflation hot, the Fed cannot look at weaker growth and simply say, “Fine, time to cut.” It may have to sit tight while the economy slows, because inflation is still too uncomfortable to ignore.

This is why peace headlines can knock recession odds down so quickly. If the Iran shock fades, one of the main reasons for a trapped Fed fades with it. If it sticks around, Polymarket’s 25% odds stop looking so expensive.

The “Yes” case is more of a grind: higher costs, weaker real income, companies getting more careful, non-AI investment losing steam, and eventually a labor market that stops absorbing the pressure.

Here’s where the market may be mispricing it

A slow squeeze can be painful without being useful.

If Q2 GDP stays positive, the “Yes” side loses a lot of room. The GDP path would then likely need Q3 and Q4 to both come in negative on the advance estimates. The NBER path is not much easier. NBER can call recessions without waiting for two negative GDP quarters, but it still needs broad damage across jobs, income, production, and sales.

That is why 25% may be rich. The market may be reading the economy correctly, with weaker consumers, sticky inflation, and the Fed with less room to cut. But the missing part is speed, because all of this must become official before the deadline. A fairer number may be closer to the high teens, maybe 15% to 20%, unless Q2 starts deteriorating quickly.

Overall, Polymarket’s recession odds are not irrational. But they are demanding a lot from the next few quarters, relative to the path required from here, because Q1 GDP was positive and Q2 GDPNow is still strong.

Source: Polymarket

The market needs proof that the squeeze is becoming broad enough, deep enough, and fast enough to show up in the data before the settlement window closes.

Until then, the 25% odds look more like a premium on anxiety. Traders may be right that the U.S. economy is losing altitude. But will it fall quickly enough for this market to pay?

Data sources:

- AtlantaFed: Current and Past GDPNow Commentaries

- BEA: Personal Income and Outlays, March 2026

- BEA: Gross Domestic Product

- Federal Reserve: One Transitory Shock After Another

- US Bureau of Labor Statistics: Employment Situation Summary