This week’s Nonfarm Payrolls report lands on Thursday, July 2, at 8:30 a.m. ET, according to the US Bureau of Labor Statistics (BLS), one day earlier than usual because US markets are closed Friday for Independence Day.

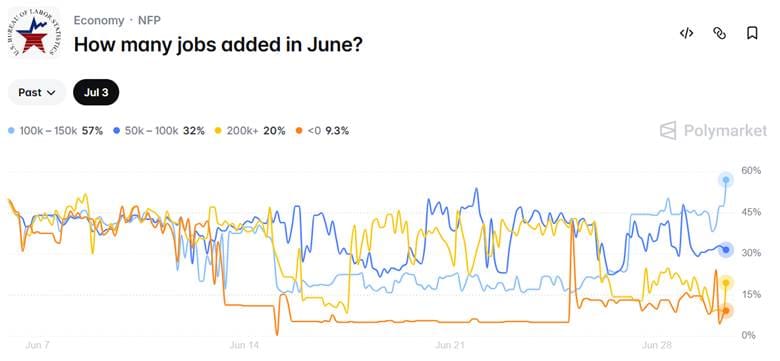

Polymarket is currently pricing the July 2 U.S. Nonfarm Payrolls release with a huge tilt toward 100k-150k jobs added, just below 60%, but the upside tail is not negligible.

This is consistent with economists' forecasts. According to a Reuters poll, economists are clustered around 110,000 jobs added in June, down from May’s 172,000 gain. Unemployment is expected to hold near 4.3%, while wage growth is expected to stay around 0.3% month over month.

But what if the market is overconfident in the stability of the 100k-150k range because it is anchoring on lagged, revised, and smoothing labor indicators?

What do you think the market is underestimating the most?

May made the bar harder to clear

The reason this week’s report is more interesting than the consensus number suggests is May.

Economists expected only 85,000 jobs last month. The actual number came in at 172,000. March and April were also revised higher by a combined 93,000 jobs. A few weeks ago, the concern was that hiring had become too soft. After May, the cleaner question is whether the slowdown thesis got too much credit too early.

Still, the devil is in the details because May was not a perfectly broad-based boom. Leisure and hospitality added 70,000 jobs, local government added 55,000, and health care added 35,000. Financial activities lost 22,000 jobs. This shows an uneven labor market holding headline strength.

Another report above 150,000 would make May look less like a one-off. A number below 100,000 would bring back the idea that the labor market’s surface strength is hiding weaker hiring underneath.

But is headline NFP a clean signal?

Everything in the pricing depends on this: headline payrolls accurately reflect underlying labor momentum.

But NFP is not a direct measure, it’s a modelled survey estimate that makes it vulnerable. The current consensus stability relies heavily on data that has already been revised multiple times this year.

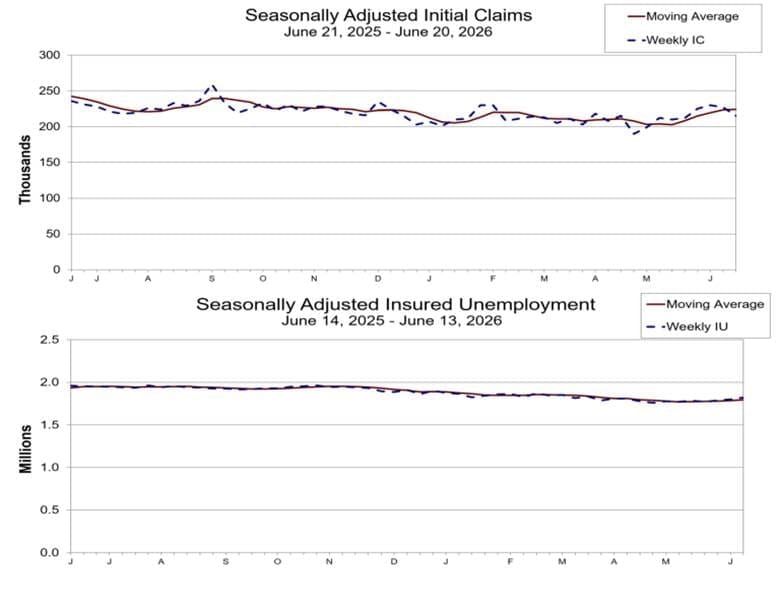

Initial claims fell to 215,000 for the week ending June 20, below the 225,000 economists expected. This alone tells you companies are not suddenly rushing to cut workers.

The softer signal is in continuing claims, which rose to 1.821 million. Low initial claims say layoffs are contained, but higher continuing claims say people who lose jobs may be taking longer to find the next one.

The latest JOLTS data shows that job openings rose to 7.6 million in April, but hires fell to 5.1 million and total separations dropped to 5.0 million. Quits were little changed at 3.0 million, while layoffs and discharges were also little changed at 1.7 million.

Taken together, it’s not a classic “everyone is getting fired” labor market, but it does look more like a frozen one. A low-churn environment where hiring momentum is softening even as headline stability is preserved.

Wages may matter more than the jobs number

The payroll number gets the headline, but wages may decide the market reaction.

In May, average hourly earnings rose 0.3% on the month and 3.4% from a year earlier. Another 0.3% wage print in June would not look shocking on its own. Paired with a strong jobs number, though, it becomes harder for the market to treat labor strength as harmless.

A softer payroll number with cooler wages would do the opposite. It would support the argument that demand is fading and that policy is already restrictive enough. The unemployment rate would then become the tie-breaker. A move up from 4.3% would carry more weight than a small miss on payrolls alone.

What traders should watch on Thursday

The key risk this week is that markets overweight the stability implied by recent revisions. March was revised up 29,000 and April up 64,000, reinforcing the perception that initial prints understate true strength.

A market pricing the initial June print needs the actual release to land soft, not just the eventual, revised reality, and on a year where every revision has added jobs back rather than taken them away, betting heavily against the consensus bracket has a real headwind.

The first number to watch is the headline payroll range. A 100,000 to 150,000 print broadly confirms the market’s base case. A sub-100,000 print makes the slowdown story harder to ignore. A 150,000-plus print puts the “too hot” debate back on the table.

A 4.3% unemployment rate keeps the soft-landing read in place, but that reading depends on the rate staying pinned inside a narrow 4.3%-4.5% band where small shifts change how much slack the market thinks exists. At 4.4%, this stability starts to look less certain, and a drop toward 4.2% would make it harder to argue that hiring is cooling fast enough.

The third number is wages. Payrolls can miss or beat for noisy reasons, especially in summer. Wage growth is harder to shrug off because it feeds directly into the Fed debate.

Revisions also deserve a close read. May looked strong partly because previous months were revised higher. A June miss would sting less with upward revisions. A June beat would look more convincing with another positive revision behind it.

The print won't move the July 28-29 FOMC decision directly, but it's the last full labor read before it, and a soft surprise would revive easing hopes, while a strong payroll-and-wage combination would strengthen the case for higher-rate risk.

Sources:

1. Barron’s: Additional 93,000 Jobs Added to March and April Totals

2. BLS: Employment Situation Summary (March)

3. BLS: Employment Situation Summary (May)

4. BLS: Job Openings and Labor Turnover Summary

5. DOL: Unemployment Insurance Weekly Claim

6. Reuters: Wall St Week Ahead Jobs data, rate bets in focus as US stocks close solid first half