Economic forecasts tell us what analysts expect, but prediction markets show us where traders are willing to put capital behind a view.

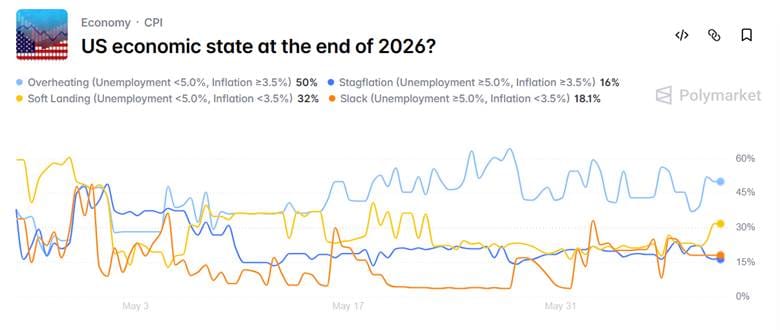

Right now, one of the more interesting macro markets on Polymarket is asking what kind of economy the US will have at the end of 2026. The market gives traders four choices: soft landing (32%), overheating (50%), stagflation (16%), or slack (18.1%). The contract resolves based on official BLS data for December 2026.

Strip away the labels and the trade comes down to two questions: does inflation stay sticky, and does unemployment cross 5%?

As of this writing, “overheating” at 50% looks like the obvious answer. Inflation is still high, unemployment is still below 5%, and the economy has not clearly cracked, so based on the latest data alone, the label fits almost too neatly.

But there may be a blind spot here.

Inflation is already close to the line

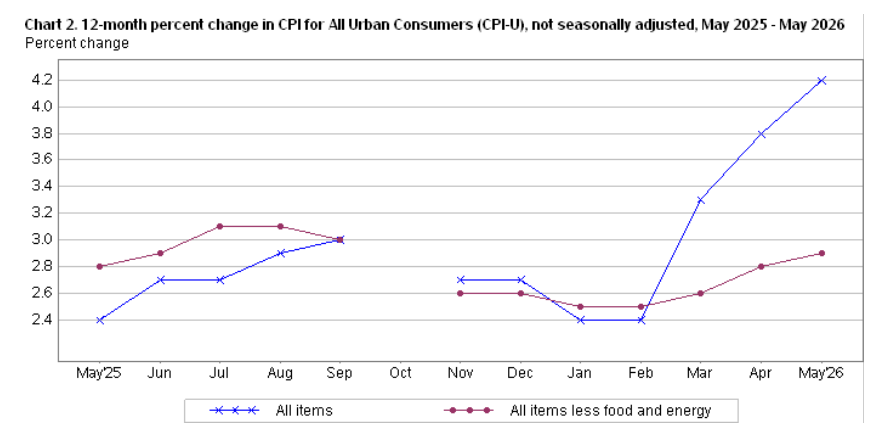

The inflation condition is currently satisfied, but the question is whether it stays satisfied through the market's December 2026 resolution data. May CPI was 4.2% year over year, while chained CPI was 4%. Both are above the market’s 3.5% cutoff.

So, for stagflation to resolve, December 2026 inflation needs to remain above the market's cutoff. And there are several reasons it could.

Source: BLS News Release

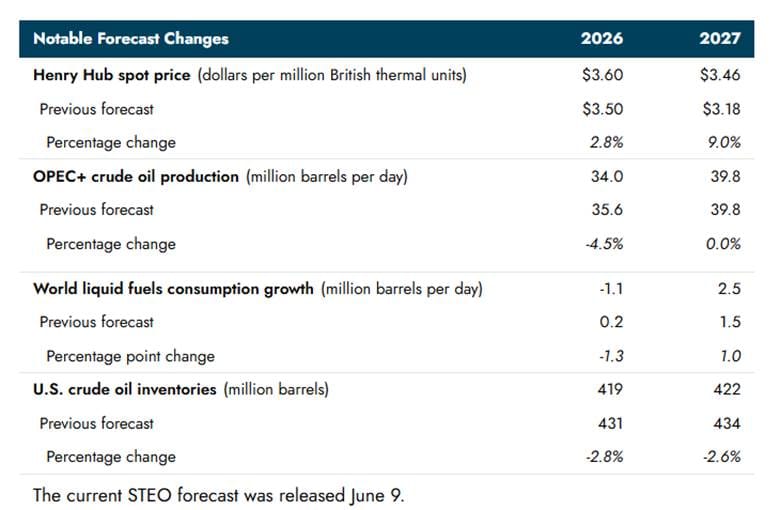

Energy prices are the obvious one. The EIA’s forecast points to a tight oil market through early summer. Its latest outlook assumes the Strait of Hormuz remains effectively closed in the near term, with shipments only starting to resume in the third quarter.

Source: EIA

Oil touches transport, food distribution, airline costs, manufacturing, and consumer expectations. When energy prices rise, they can show up across the economy in ways that are hard for central banks to ignore.

This is especially awkward for the Fed. If inflation is being pushed up by energy, cutting rates does not produce more oil. But keeping rates high can still hurt jobs, housing, credit, and business investment.

The labor market does not need to collapse

Inflation is already in the right zone for both overheating and stagflation, so unemployment is the swing variable.

The Fed’s own language points to this tension. Its April statement described an economy still expanding at a solid pace, but with job gains remaining low on average, unemployment little changed, and inflation elevated partly because of global energy prices.

For this market to resolve as stagflation, the December 2026 unemployment rate needs to reach at least 5.0%. The latest unemployment rate was 4.3%, so the gap is only 0.7 percentage points.

Fiscal pressure adds another layer

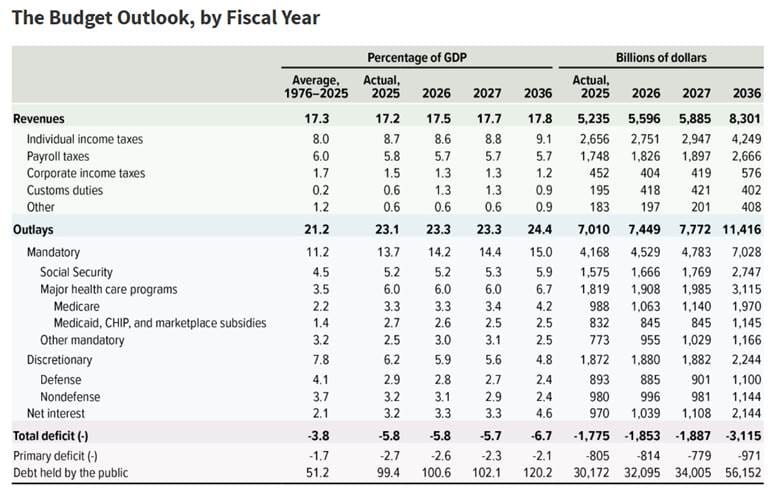

The US is running large deficits, and interest costs are a burden. If the government has to borrow more, investors may ask for a higher return before they agree to hold long-term debt. So yields can stay high even if the Fed is not the one pushing them up.

Source: CBO

Once yields move higher, the effects show up almost everywhere. Mortgages get priced off them. So do auto loans, corporate debt, and parts of the credit-card market. Stocks feel it too, because higher bond yields make future earnings look less valuable today.

The overheating outcome assumes the US can keep absorbing high inflation, high rates, high oil prices, and large deficits without the labor market crossing a fairly modest 5% unemployment line.

Maybe it can. But this is not a risk-free assumption.

Why stagflation may be the better mispricing

Overheating is basically the “everything keeps working, but inflation stays hot” outcome. Stagflation is the “inflation stays hot, but the labor market finally starts to feel the pressure” outcome.

The second path only requires a small rise in unemployment and inflation that refuses to cool below the market’s threshold.

This makes it a cleaner mispricing candidate than a basic recession market. A recession call needs broader economic damage. A stagflation call, at least in this Polymarket market, needs a milder shift: unemployment at 5.0% or above, inflation at 3.5% or above.

This is why this market is worth watching.

The crowd may be right that the US economy is too strong for a classic downturn. But it may still be wrong about the type of strength we are dealing with. An economy can look hot late in the cycle, then start to leak from the labor side while inflation remains sticky.

The bottom line

Prediction markets are good at showing what traders believe right now. For traders, the key question is not whether the economy is strong today, but whether today's strength can survive another several months of energy pressure, restrictive policy, and rising credit costs without the labor market crossing a relatively modest threshold.

Overheating is not a dumb market view; it is the current-data view. But stagflation is the convex risk if labor deteriorates while energy keeps CPI high. If unemployment moves only modestly higher while energy keeps CPI above 3.5%, this market could reprice faster than traders expect.

Data sources

- BLS: Consumer Price Index Summary

- CBO: The Budget and Economic Outlook: 2026 to 2036

- EIA: Short-Term Energy Outlook

- Reuters: Yields mixed after jobs data lifts Fed hike odds

- U.S. Bureau of Labor Statistics: Consumer Price Index News Release