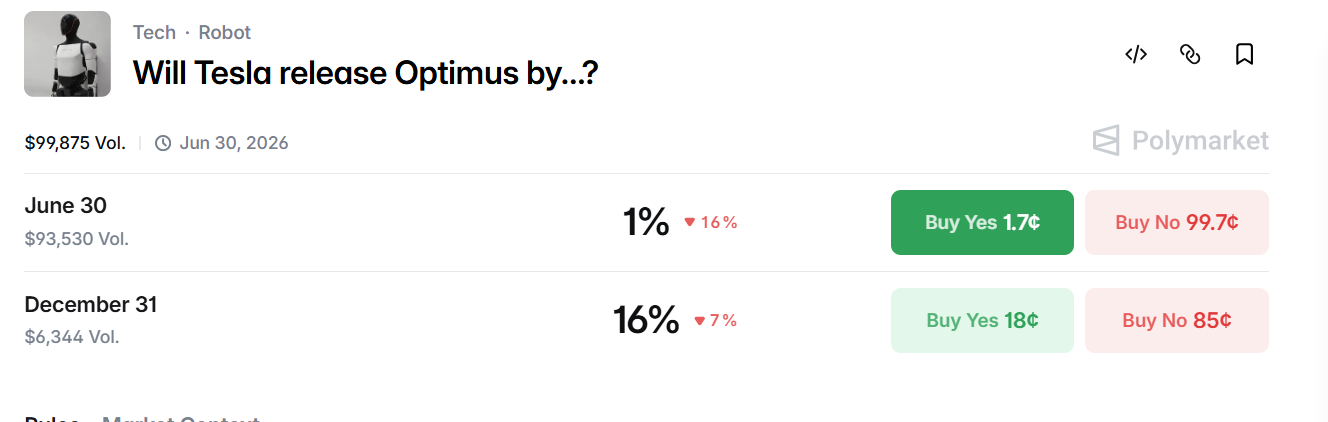

While Polymarket’s Optimus contracts may be priced accurately, the underlying reasons for these valuations are widely misunderstood. Ahead of the June 30 deadline, Polymarket’s contract on the likelihood of Tesla releasing Optimus sits at just 1%, while the consensus for the December 31 deadline is tilted slightly higher at 16%. The prices and the bets aren’t necessarily wrong, but their standard interpretation misses the mark.

Currently, Polymarket is running two Optimus release markets (June 30 and Dec. 31), while Kalshi is running a contract based on the robot's availability for sale in 2026.

All year long, we’ve seen the prices for these contracts drift downward. The June 30 market currently has an order book of around $93,530 against a lifetime volume of $99,873. It is safe to say the market isn’t expecting Tesla to make a massive Optimus announcement anytime soon, especially with public attention largely divided among Elon Musk's other ventures.

More importantly, resolving these contracts positively requires a very specific event: the availability of the Optimus robot for general purchase via an official Tesla press release, accompanied by a standard consumer checkout feature. Anything less than that—such as product demos, pilot launches, or asking visitors to register their interest without an exact launch date—will not trigger a payout.

Therefore, we can safely assume that these Polymarket contracts have nothing to do with the actual progression of AI or whether Tesla has the wherewithal to build a multi-use robot. They are exclusively pricing the odds of seeing a consumer checkout button.

The True Metric: Industrial Deployment

Currently, the market is pricing these contracts fairly accurately because Elon Musk has already informed investors that the earliest consumers could purchase Optimus would be in the latter half of 2027. Furthermore, the 2026 Optimus program is entirely focused on internal usage and a gradual transition toward industrial applications. The first units are slated to be deployed on Tesla’s own production lines later this year before moving to other industries.

This is exactly why citing these prediction contracts as a verdict on the viability of "embodied AI" is erroneous. While a contract might accurately answer its own narrow criteria, it is the wrong medium for the questions most investors are actually asking, such as "Does embodied intelligence actually work?"

The reality is that while Optimus has no presence on the retail floor, the actual leading indicators of embodied AI are purely industrial. This sector is moving incredibly fast, with several companies already running parallel to—or even ahead of—Tesla.

For now, anything linked with Optimus capabilities, pricing and demand would be confined to speculations and forecasts, with contracts serving as the closest source to gauge its prospects in the near term.

It can also be said that the existing contracts are handicapped and limited because of a lack of clear catalysts visible through the company's investor relations department. For Tesla, the key value this year could be assessing total robot hours clocked and rigorous testing before the product is ready for general consumer use.

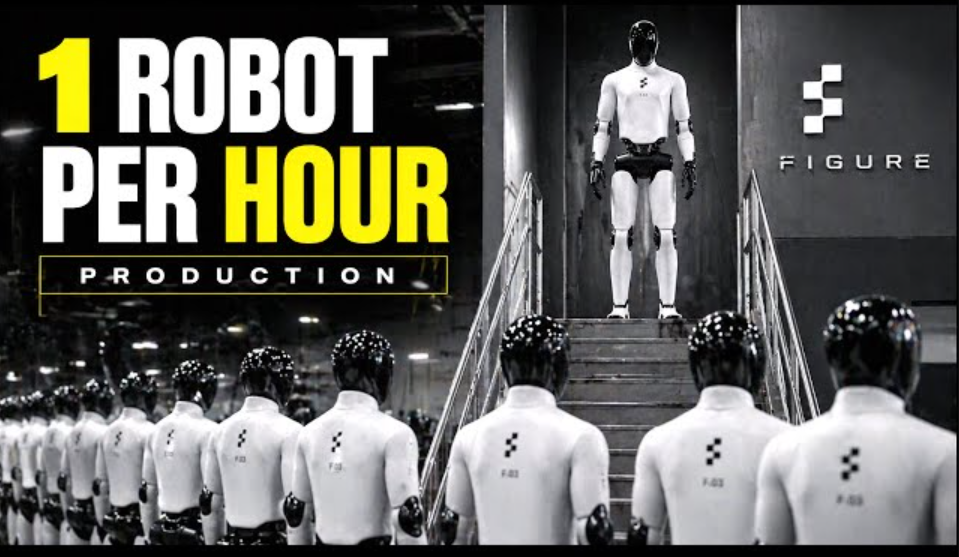

Figure, for instance, tested its Figure 02 robot at BMW’s Spartanburg Plant in an 11-month deployment. The robot clocked more than 1,200 hours, handled over 90,000 parts, and contributed to the manufacture of 30,000 vehicles. Since then, the company has deployed next-generation units in the same facility, and UPS is slated to become its second paying customer. Furthermore, Figure recently revealed how its Helix control model replaced human-built C++ balance code, reducing new development turnaround time from 12 months to roughly 30 days.

Meanwhile, Chinese manufacturers are already shipping hundreds of humanoid models, and industrial units are actively being deployed on automotive assembly lines. The key variable the broader market is currently blind to is the transition of embodied AI into tangible industrial robot-hours, which is already creating revenue streams and reducing deployment timelines.

Two Fundamental Flaws in the Optimus Contracts

Treating the Optimus retail contract as a bellwether for the robotics industry is a decoy. In fact, relying on it commits a double category error by getting two fundamental things wrong:

The Event Type: The contract is pricing a retail consumer launch, not a commercial deployment. Tesla has already hinted at having zero fully useful internal units currently and hasn’t even committed to a concrete production number for 2026.

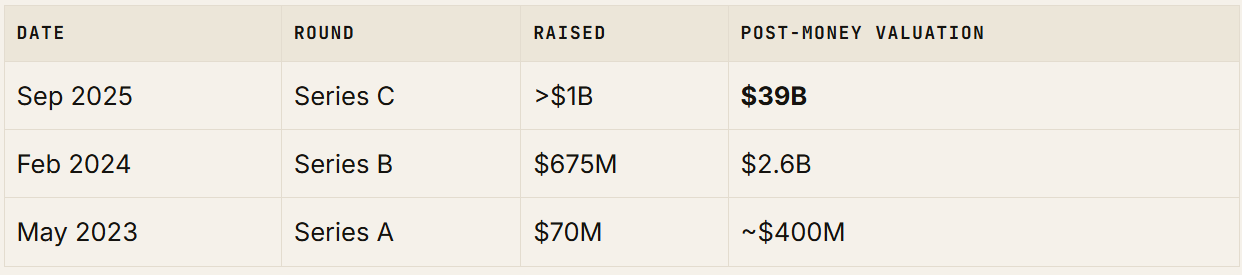

The Industry Benchmark: The market assumes Tesla is the sole vanguard of humanoid robotics. While Tesla’s massive valuation points to its potential, it isn’t actually at the forefront of industrial humanoid deployment. Figure raised over $1 billion at a $39 billion post-raise valuation last year, is already generating revenue via BMW, and is targeting production of 100,000 robots within four years.

It wouldn’t be a stretch to say that the existing Optimus prediction contracts are marketing artifacts rather than technical barometers. In time, we will likely see a "Reserve your Optimus" page with a refundable deposit—a standard launch playbook Tesla has previously used for the Cybertruck and Roadster. However, even if Tesla, Figure, and Chinese manufacturers deploy thousands of units in factories globally, these Polymarket contracts could remain unresolved because industrial reality rarely converges with an immediate consumer checkout option.

Looking Beyond the Headlines

Despite their flaws, the year-end contracts still offer valuable insights. Because they rely on a more distinct possibility, they gauge Tesla’s potential capability to expose Optimus to consumer purchase this year, offering a glimpse into the market's read on development timelines.

More importantly, the pricing reflects market bearishness regarding Musk’s notoriously optimistic timelines. While dedicated Optimus factory construction officially began at Giga Texas in May, actual production isn’t likely to begin before July or August. Even when it does, initial units will only support internal factory tasks. Earlier this year, Tesla archived its Model S and Model X lines, with the last units rolling out of Fremont in May, recalibrating the factory space to accommodate Optimus. The company is heavily betting on embodied AI to beef up its revenue, but it is entering a market where competitors are already scaling and serving paying customers.

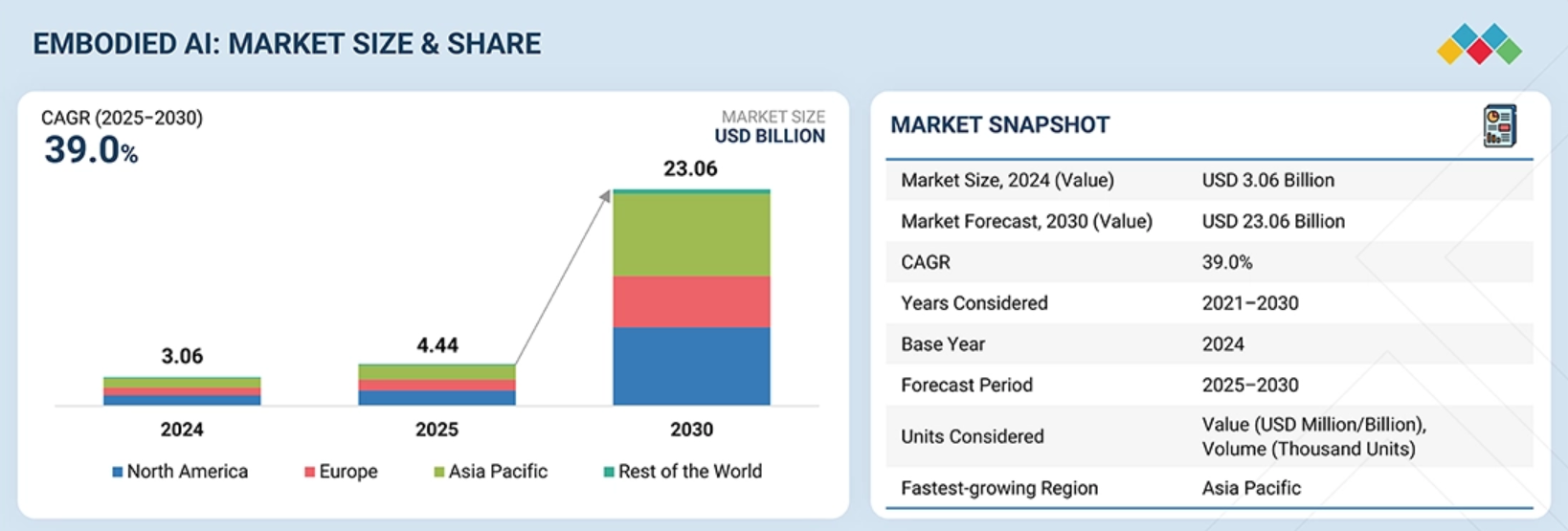

It is also crucial to look at where the embodied AI industry is heading. The near-term consensus seems modest with Goldman Sachs projecting roughly 502,000 humanoid shipments by the end of 2032 and a total addressable market of $38 billion by the same period, attributing this to AI breakthroughs and a potential 40% drop in manufacturing costs.

Additionally, Morgan Stanley has forecasted a $5 trillion total market by 2050 with around 13 million humanoids in service by 2035, before pushing to 1 billion by 2050.

Ultimately, if you are looking for a better instrument than a headline poll to track embodied AI, look off-market. Watch the metrics that matter: industrial deployment numbers and total robot-hours.

The Optimus contracts follow a prediction pattern similar to Tesla’s Robotaxi markets. While a driverless service is a technological certainty, the prediction contracts for Robotaxis in California are trading at around 11% because they bank on consumer regulatory approval and purchase optionality, not purely on the underlying technology.

Existing prediction markets don’t tell the whole story. As the industry matures, we should expect the narrative to deepen, eventually addressing the frontier-capability questions that investors actually want priced into future contracts.