Kevin Warsh will become chair of the Federal Reserve next week, and he has promised to improve how inflation data is collected and analyzed. He should go further. Official statistics, crucial to crafting policy for the vast and complex American economy, are being challenged from two directions, and the squeeze will land on the new Fed chair.

President Donald Trump fired the previous Bureau of Labor Statistics Commissioner Erika McEntarfer last year over a jobs report he found inconvenient and has demanded interest rate cuts that the data does not support. This puts direct political pressure on the producers of the official numbers.

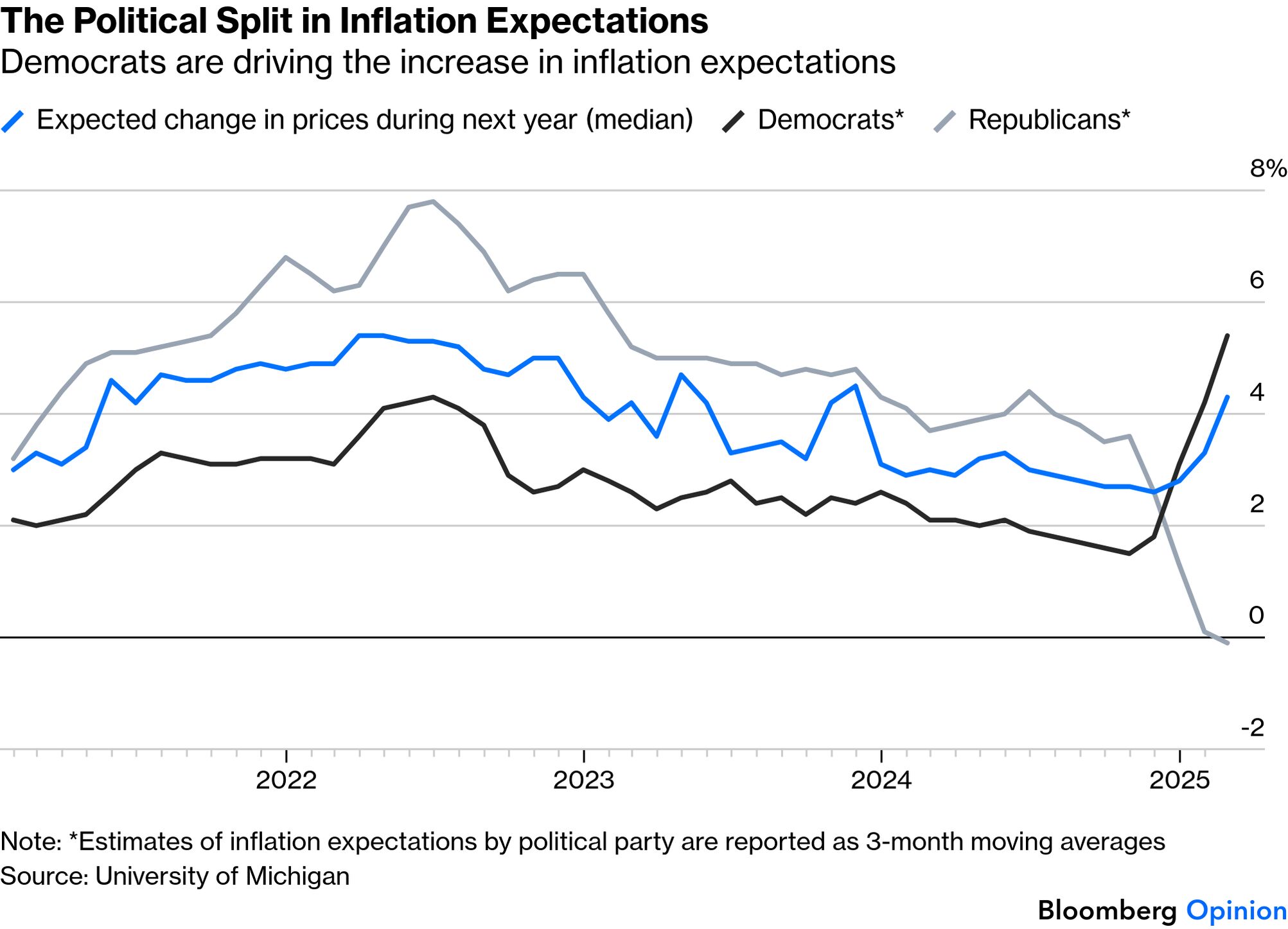

The other pressure comes from the marketplace: alternative statistics that bypass economists altogether and take the policy argument straight to the public political forum. The University of Michigan’s long-running consumer survey of inflation expectations is an example of this latter problem, where the survey has effectively become a partisan thermometer rather than a neutral indicator.

Another is the Ludwig Institute for Shared Economic Prosperity’s True Rate of Unemployment. The measure pegs “functional unemployment” at 23.6%, more than five times the official figure of 4.3% in March. It gets there not by finding hidden unemployment, but by adding the Bureau of Labor Statistics’ existing broader measure (U-6, which also counts the underemployed and runs a bit under 8%) and 16 percentage points of full-time but low-wage workers. It’s an unhelpful grouping since low wages, underemployment and joblessness are distinct phenomena that require distinct measurements and policy prescriptions.

These two pressures look opposite, but they are the same impulse approaching from different doors: The desire to override technocratic measurement with political will. What complicates Warsh’s job is that the official numbers are genuinely fraying, and the marketplace of alternative measures is not all advocacy; some of them fill real gaps.

Consider the BLS payrolls report, the monthly jobs number that moves markets and shapes the Fed’s interest rate decisions. The agency builds it from a survey of employers, but only 43% of employers now respond. This opens the door to revisions, which can sometimes be so large as to entirely alter our view of the labor market.

That’s what happened earlier this year when BLS revisions cut the prior year’s reported job growth by 70%. A labor market that had looked resilient turned out, in the rearview mirror, to have been stagnating. Last October’s Consumer Price Index release was lost entirely to the government shutdown. Even when the official numbers work, they are slow: monthly, quarterly, revised the following year.

A new generation of private competitors looks through the windshield instead. ADP Research’s National Employment Report, built on actual payroll data from 26 million workers, can tell you what is happening in the labor market this week. Truflation scrapes online prices daily. Kalshi Inc., a federally regulated prediction market, runs continuous bets on the next CPI release, aggregating the views of everyone willing to put money behind a forecast. These are windshield views. They are also smudged windshields.

Kalshi prices on the December 2025 CPI release showed two distinct peaks rather than a single consensus, with bettors clustering around 2.55% and 2.65% inflation — almost certainly a sign of partisan rooting. ADP excludes government workers and tilts toward midsize businesses, because that is the shape of its client base. None of this is methodologically clean.

But the smudges and the information are the same thing. The two Kalshi peaks were a signal — a partisan disagreement that is moving consumer behavior, market positioning and Fed credibility. ADP’s business-mix bias is a window into where employment is shifting. Forecasts produced by people with money at risk encode opinions; survey-based forecasts do not, but opinions are data too.

The Fed’s own staff has taken notice. A 2024 working paper, “Kalshi and the Rise of Macro Markets,” found that the prediction market’s prices match or beat the Bloomberg consensus of Wall Street economists on year-over-year CPI. The mode of the Kalshi distribution has matched the realized federal funds rate by the day of every meeting of the central bank’s rate-setting committee since 2022 — a feat neither professional surveys nor federal funds futures can claim.

Warsh’s easier challenge will be integrating reliable, tested, known-defect rearview-mirror numbers with the timelier, broader, messier attempts to peer through the windshield.

His harder job will be firmly rejecting the third category: alternatives that are not faster or richer, only louder. Ludwig’s TRU is the leading example. It conflates low wages with unemployment, even though the policies that would address the two phenomena conflict with each other. Raising the minimum wage, for example, would help some workers but also reduce employment at the margin. TRU couldn’t tell you if you’d helped or hurt because it counts both populations together. Despite its shortcomings, it nonetheless travels effortlessly through political coverage — which is precisely the problem.

The Fed should integrate windshield measures explicitly into its policy framework: prediction market-implied inflation expectations alongside breakeven inflation drawn from the Treasury market; ADP alongside BLS, with the divergences treated as information rather than noise; high-frequency price indexes alongside monthly CPI. It should resist the impulse to elevate every alternative metric that flatters a preferred conclusion.

And it should defend the official series against pressure from the political ins above and the political outs below — not because the official series are perfect, but because they are common. Everyone using the BLS unemployment rate is talking about the same thing.

The country does not need more statistics. It needs better ones, in the right places, with the discipline to know which is which. The temptation that will sit on Warsh’s desk — from one direction in the form of presidential demands, from the other in the form of methodologically aggressive private metrics — is to let the political process pick the numbers. The job of the next Fed chair is to just say no.

- Five Suggestions for Warsh on Fed 'Regime Change': Bill Dudley

- Warsh Has Been Too Quiet About Unemployment: Claudia Sahm

- The Bond ETF Sales Pitch Is Only Half the Story: Aaron Brown