This is the first article in my Hormuz Strait March 2026 Analysis Series.

In the pieces that follow, I will break down the wider architecture of vulnerability behind Hormuz, trace the real transmission channels from Gulf disruption into the global economy, explain how different prediction markets are pricing different slices of the same crisis, and test whether these contracts have genuine economic value as hedging instruments.

💡 Sign up to Receive Further Updates if You Haven’t Done So.

Hormuz is usually discussed as an oil story. But that framing is too narrow. What sits behind it is a much larger architecture of vulnerability, one that links shipping, energy, industrial inputs, and ultimately the global cost of living.

Why Hormuz Matters: The Architecture of Global Vulnerability

The Strait of Hormuz functions as the “physiological aorta" of the global energy and industrial system, a critical node where a single physical blockage initiates a systemic cascade across disparate markets.

1.1. Quantifying the Flow: Beyond Crude Oil

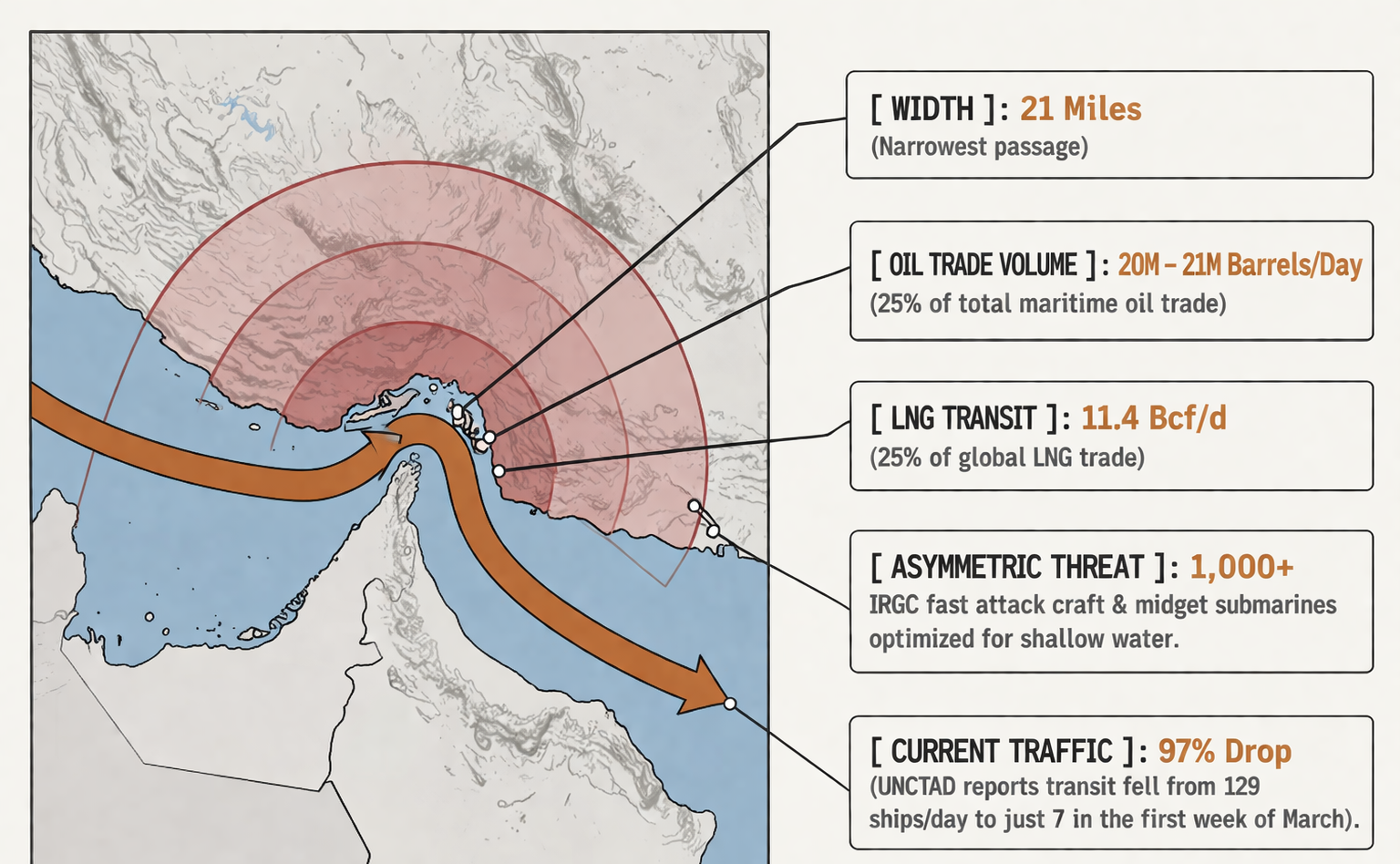

In the first half of 2025, the waterway facilitated the flow of approximately 20.9 million barrels per day (mb/d) of petroleum liquids. This volume represents 25% of total maritime oil trade and roughly 20% of world consumption.

The systemic vulnerability is articulated through the breakdown of specific flows:

- Crude Oil: Approximately 14.7 mb/d. Represents approximately 34% of all global crude oil trade.

- Refined Products: Approximately 6.1 mb/d, including essential industrial feedstocks and fuels (e.g. Gasoline, Diesel, Jet Fuel). Around 15% of global refined products trade.

- Liquefied Natural Gas (LNG): The Strait carries 11.4 billion cubic feet per day of LNG, or 20% of the global LNG trade. The export architecture of the region creates a near-total dependency for major producers, with 93% of Qatari LNG and 96% of UAE LNG relying on this single exit.

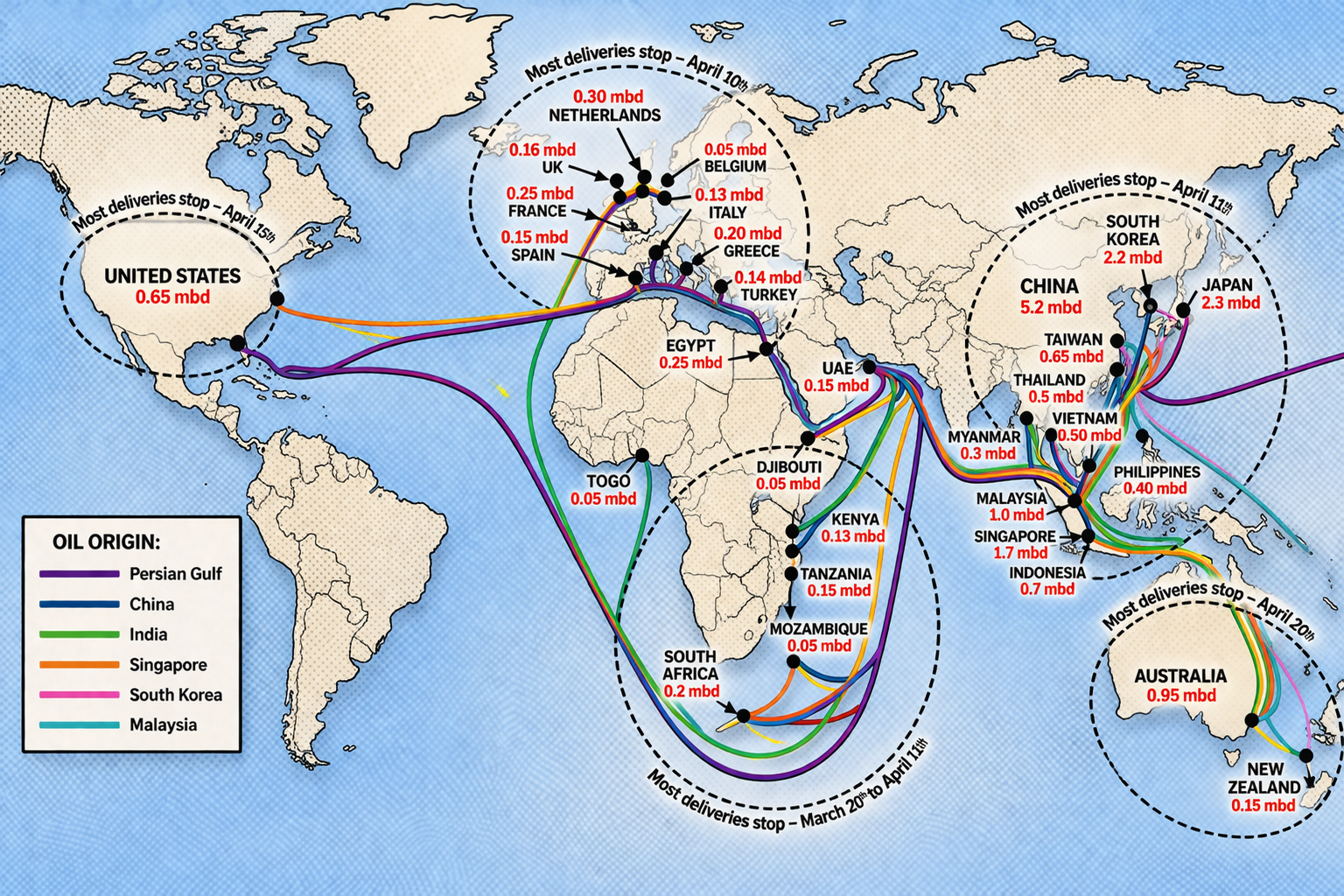

1.2. The Asymmetry of Exposure: Asia Gets Hit the Hardest

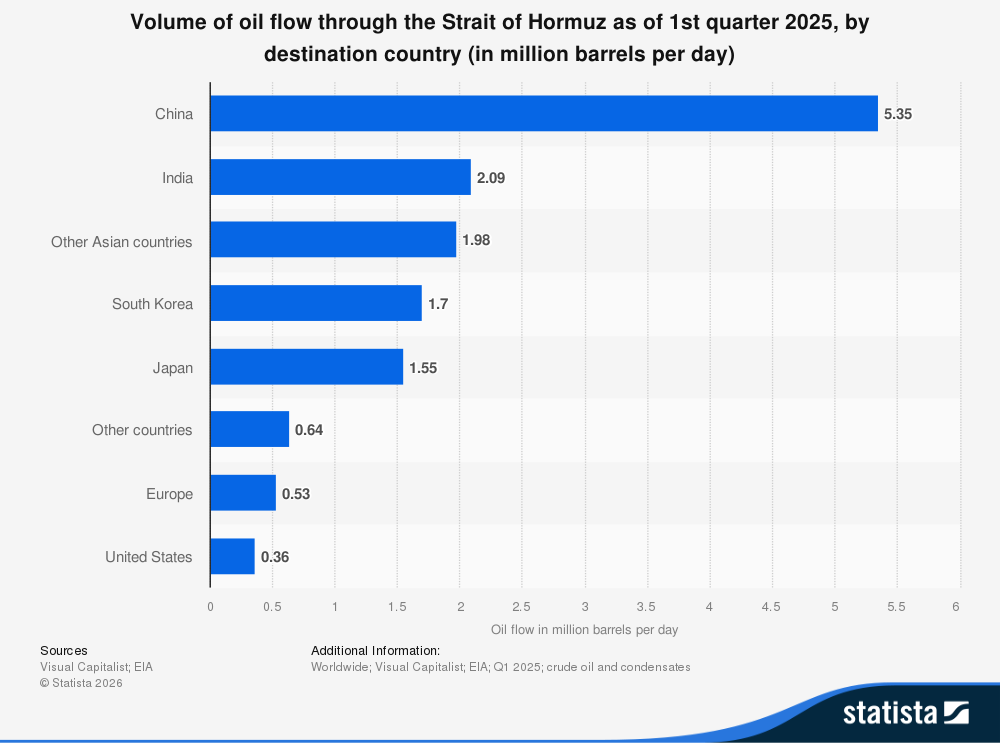

Global exposure to a Hormuz disruption is highly asymmetric, concentrated primarily in Asia, where over 80% of the oil and LNG passing through the Strait is destined.

Regional Dependency & Risk Profiles:

- Japan: Faces a critical 87% energy import reliance, with a staggering 95% of its crude oil locked into Gulf-origin routes.

- South Korea: Maintains an 81% energy import reliance, with over 70% of its oil supply tied to the Strait.

- China: Receives 38% of its total oil flow via the Strait, importing 30% of its LNG through the chokepoint.

- India: Its 88% overall crude import reliance ensures it cannot escape the global price shock. However, India has developed a "geoeconomic cushion" by moving 70% of its crude to non-Hormuz routes, providing significantly more resilience than its East Asian peers.

By contrast, the U.S. faces very limited direct risk, largely due to its role as a net exporter of oil and gas and its comparatively low levels of imports through the Strait.

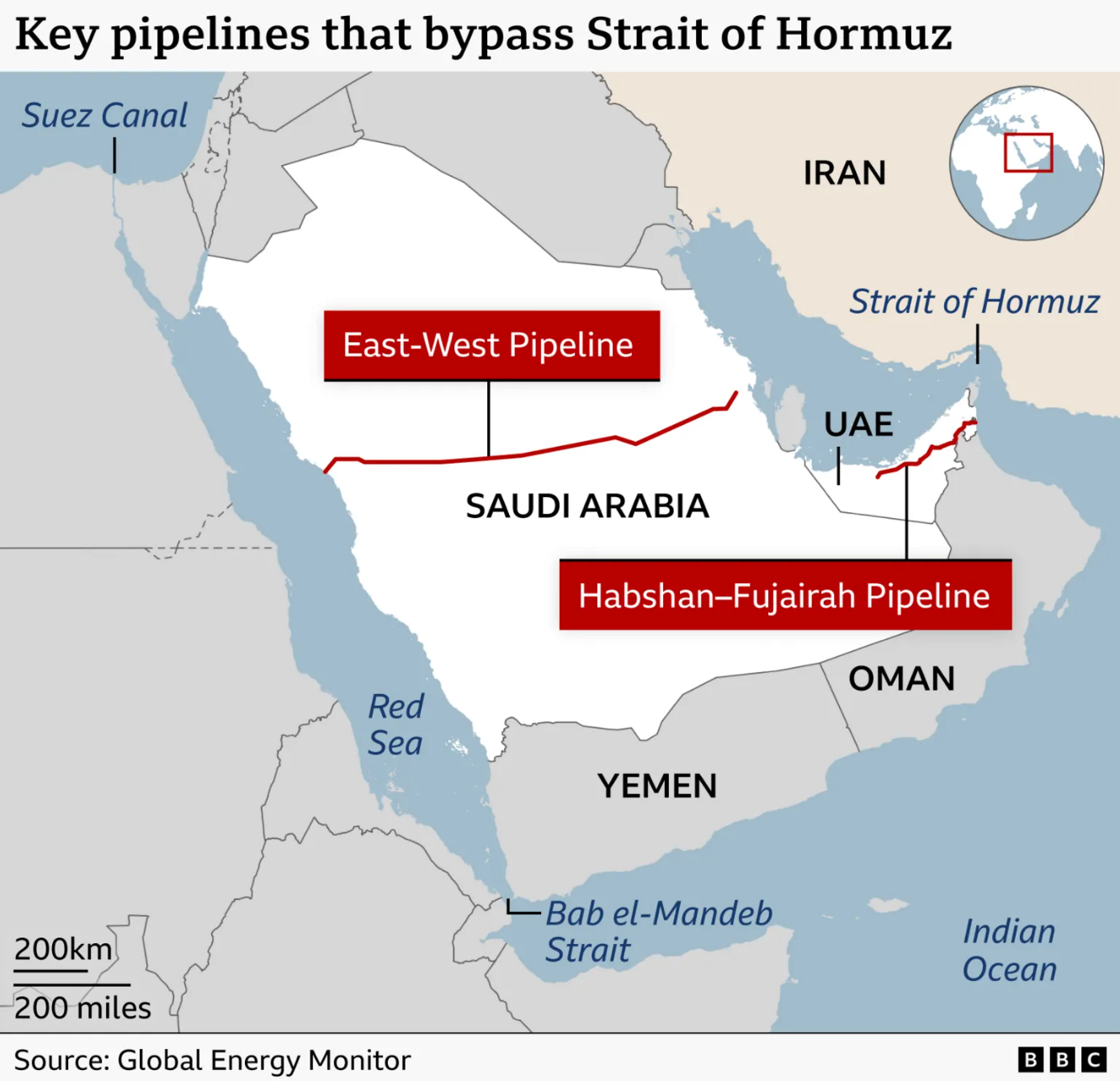

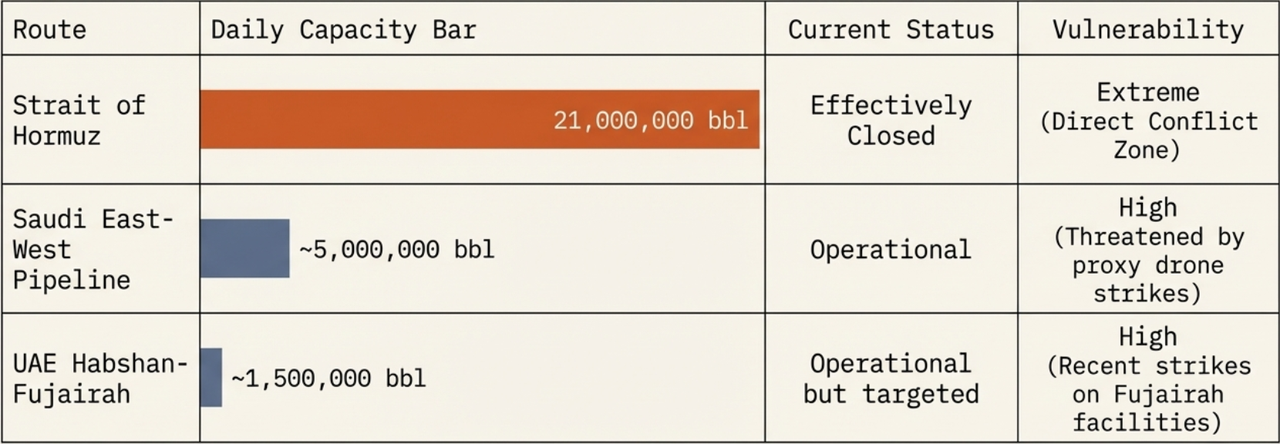

1.3. The Bypass Illusion: Capacity vs. Reality

Substitute routes offer a "bypass illusion" that fails under the pressure of a true systemic shock. While the Saudi East-West and UAE Habshan-Fujairah pipelines provide a theoretical combined additional available capacity of 3.5-5.5 mb/d (data from IEA; existing utilisation and operational constraints are taken into account), they are insufficient to offset a 20+ mb/d deficit.

The reason is that these alternatives face two structural failures:

- Cargo Incompatibility: Pipelines are restricted to carrying crude oil and cannot transport refined products or LNG.

- Physical Vulnerability: These routes are not "safe havens". The drone strikes in March on the port of Fujairah and infrastructure in Yanbu demonstrated that bypass routes are targeted during active conflicts, effectively tightening the ceiling on reroutable flows.

In summary, Hormuz is not a gate to be opened. It is a fuse that, once lit, necessitates a total re-pricing of the global industrial order.

Transmission Channels: The Anatomy of a Systemic Collapse

This systemic infection moves from energy prices to industrial inputs, eventually manifesting as a global cost-of-living crisis as shortages in fertilizers, high-tech gases, and refined fuels hit downstream sectors far removed from the Persian Gulf.

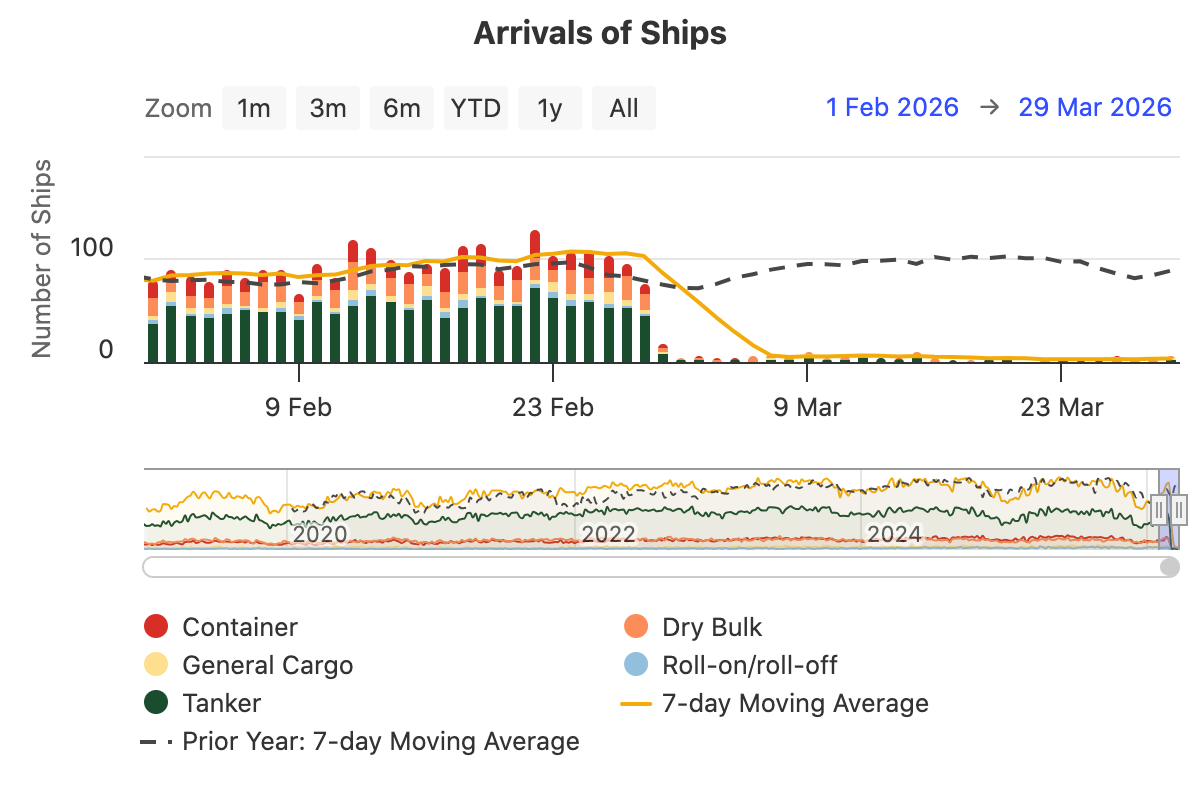

2.1. Logistics and Vessel Traffic: The Immediate Halt

The primary physical reaction to the 2026 crisis was a near-total collapse in commercial activity. Real-time IMF PortWatch data showed a 97% reduction in commercial transits, declining from an average of 129 daily transits in February to as few as 3 in the first week of March.

2.2. The Insurance and Freight Premium could Make Transit Commercially Unattractive

The JWC (Joint War Committee) and marine insurers can act as a de facto commercial choke point. By expanding Listed Areas and repricing or restricting cover, they can make Hormuz transits sharply more expensive even without a formal blockade.

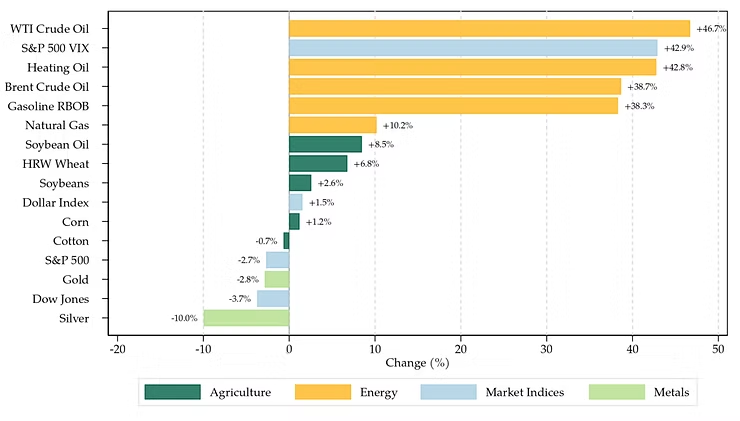

In March 2026, war-risk premiums rose from 0.25% of vessel value in normal conditions to around 1–3% in many cases, and, in some extreme mid-March cases, as high as 7.5–10% of hull value for higher-risk vessels. That pushed voyage insurance costs into millions of dollars and materially constrained commercial traffic, though shipping was also curtailed by direct crew-safety concerns rather than insurance alone.

2.3. Downstream Energy: The Refined Products Squeeze

In Asia, the naphtha shortage created an immediate crisis for the petrochemical sector, as a large share of Asia’s petrochemical feedstock imports comes from the Middle East, with dependence especially high in Northeast Asia (roughly 70% for Japan and about 50–54% for South Korea).

Major users, including South Korea’s YNCC and Indonesia’s Chandra Asri, were forced to declare force majeure, a legal declaration that they cannot fulfill contracts due to extraordinary circumstances, as their feedstock supplies were depleted.

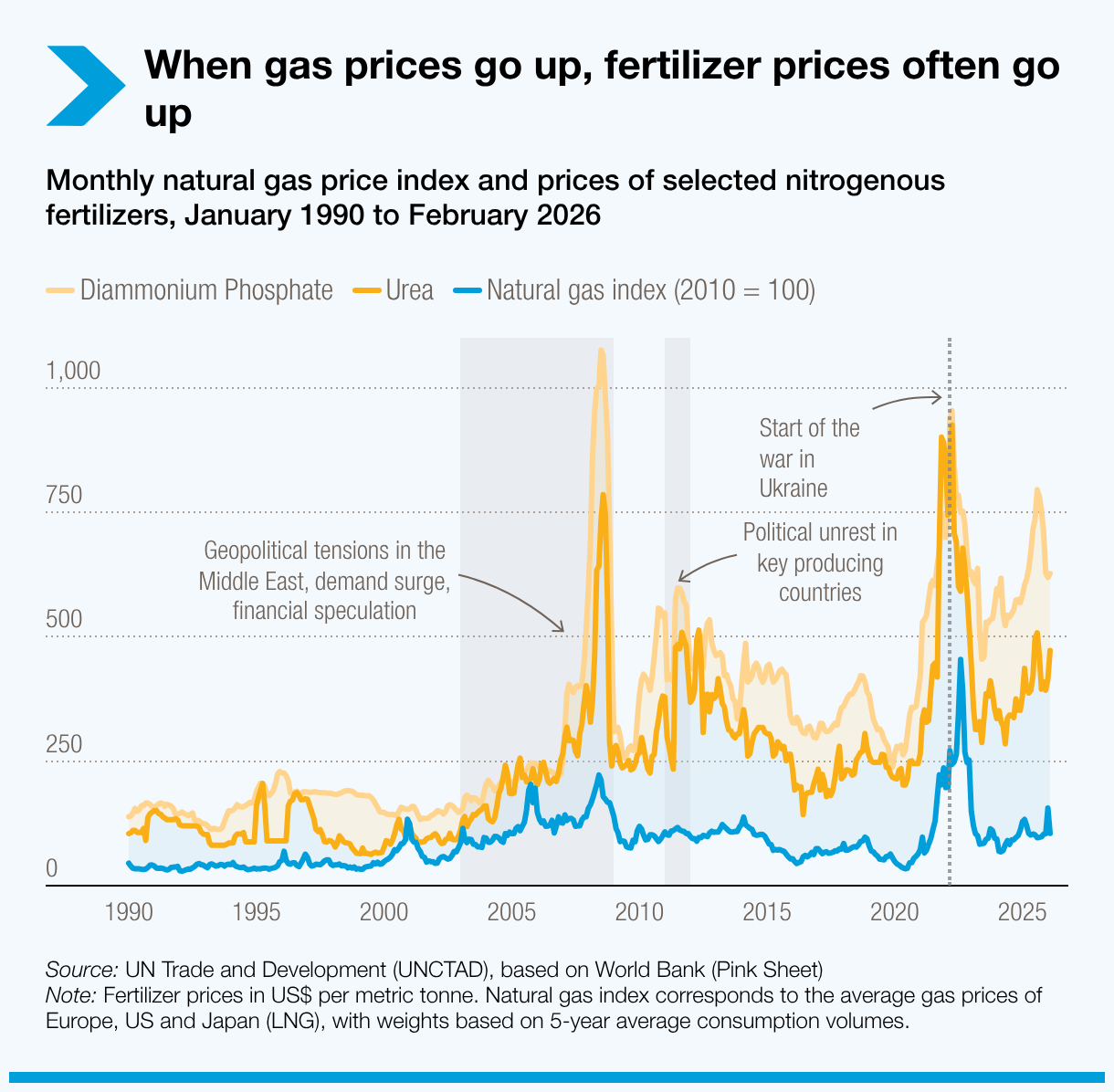

2.4. The Fertilizer and Food Security Link

The Strait also matters through fertilizer supply chains. The region accounts for 34% of global urea, 20% of ammonia, and nearly 50% of global seaborne sulfur trade.

Qatar Fertiliser Company's official website states that it is one of the world's largest single-location urea exporters, with an annual production of 5.6 million tons of urea, which could account for up to 14% of global supply.

Meanwhile, a recent Reuters report indicates that the disruption to Hormuz has tightened global fertilizer supply, prompting China to release its fertilizer reserves ahead of schedule, and that approximately one-third of seaborne fertilizer supply is related to Hormuz.

This creates direct transmission into food systems, as stress in Gulf energy and chemical exports can spill into fertilizer availability and pricing, and from there into food production costs and, potentially, food inflation.

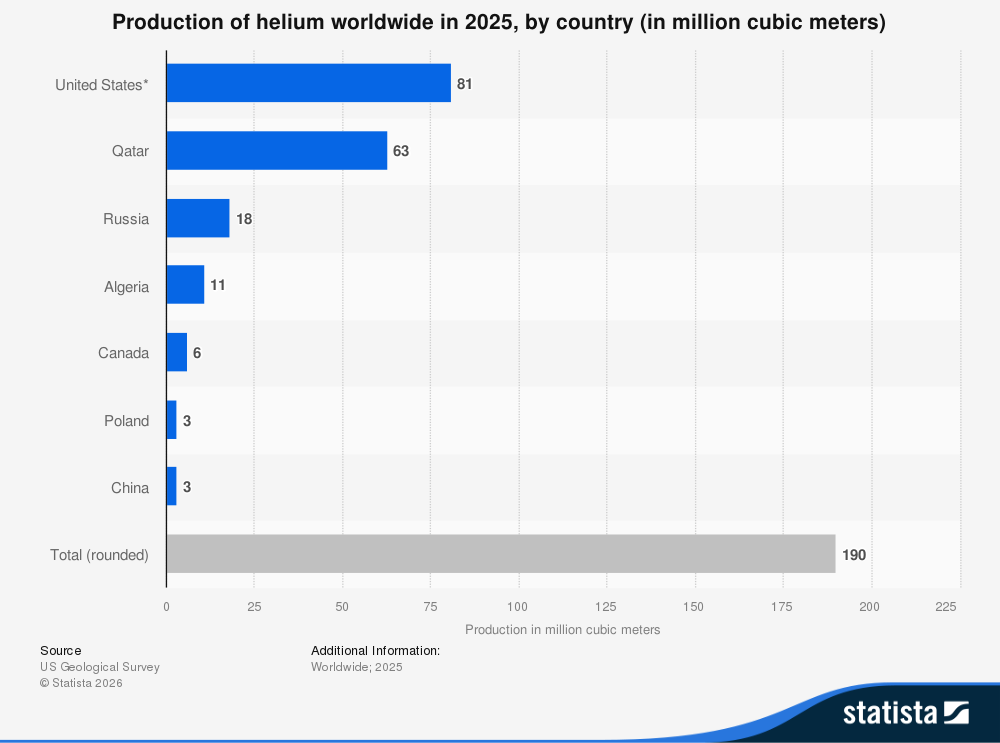

2.5. Helium and High-Tech Bottlenecks

An overlooked transmission channel is the "Helium Link". Helium is extracted from Qatari LNG processing, and the region accounts for 30-38% of global supply. Because helium is non-substitutable, a halt in transits can spill into sectors that rely on helium as a specialized industrial input, including semiconductor manufacturing and certain medical applications like MRI systems.

Market stress shows up within days, as spot supply is tighter and buyers scrambles for alternative cargoes. Reuters reported this had already begun affecting tech supply chains by March 26, and Air Liquide, a leader in the helium market, said on March 25 that a short-term helium shortage was already expected.

Large users often have some buffer stock or contracted supply. But helium is hard to stockpile for long in liquid form. It typically needs to be transported within roughly 40-60 days of liquefaction. That means a short disruption may be absorbed, but a multi-week disruption starts to bite much harder later.

2.6. Timing, Sequencing, and Persistence

The economic significance of a Hormuz disruption depends not only on size but also on duration.

Some effects appear almost immediately, such as changes in traffic, freight, insurance, and headline energy prices. Others are slower and depend on inventories, contract structures, and the ability of firms to draw on buffers or alternative supply.

The longer the disruption lasts, the more likely it is to move from transport and pricing shocks into a broader industrial and food-system problem.

The Dark Edge Case of Prediction-Market Era Exposed?

💡 This is the First Article in the Series. Sign up to Receive Further Updates if You Haven’t Done So.

Click on the Bookmark to read Article 2 of the Series

Click on the Bookmark to read Article 2 of the Series

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.