This is the second article in my Hormuz Strait March 2026 Analysis Series.

In the series, I will break down the wider architecture of vulnerability behind Hormuz, trace the real transmission channels from Gulf disruption into the global economy, explain how different prediction markets are pricing different slices of the same crisis, and test whether these contracts have genuine economic value as hedging instruments.

💡 Sign up to Receive Further Updates if You Haven’t Done So.

Click on the Bookmark to read Article 1 of the Series

This article moves from the physical system to the market layer. When traders bet on "Hormuz" on Kalshi or Polymarket, what exactly are they betting on? I break down the contract taxonomy and explain why the 7-day threshold matters so much.

The core idea is simple: not every disruption is a true closure, and not every Hormuz contract is a bet on the same underlying reality.

Learn More if You Don’t Know How an Event Contract Works Before Proceeding

Contract Taxonomy: Systematizing Strait of Hormuz-Related Markets on Kalshi and Polymarket

One easy mistake in this story is to treat every Strait of Hormuz contract as if it were betting on the same thing. It isn’t.

Some markets are trying to answer a physical question: Are ships actually moving through the strait again?

Others are asking a political question: Has there been a formal ceasefire? Others sit somewhere in between: Has a military escort regime emerged that could allow limited passage even without peace?

That is why clean taxonomy matters. Without one, it is very easy to compare markets that sound related but are actually pricing different slices of the same crisis.

3.1 A quick way to think about the market universe

The easiest framework is to split Hormuz-related contracts into four buckets:

Direct disruption

Traffic-state

Diplomatic settlement

Military-facilitation

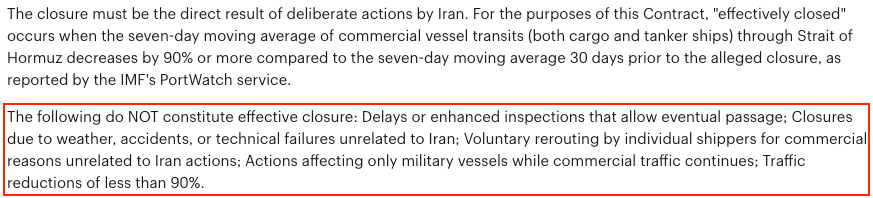

A direct disruption contract prices a real operating shutdown, not just higher tension. Kalshi’s 7+ day closure market is narrower than the headline suggests: delays, inspections, or other frictions that still allow eventual passage do not count as an “effective closure”. In other words, it is trying to capture a true disruption regime rather than generic geopolitical stress.

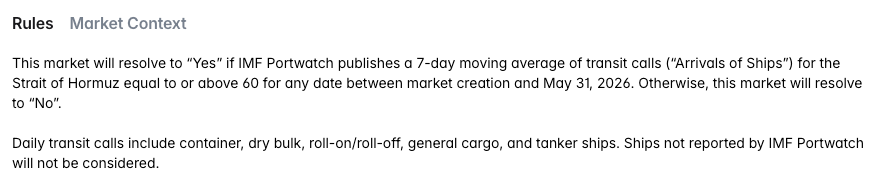

A traffic-state contract prices measurable throughput. The clearest example is the Polymarket traffic-normalization market, which resolves to “Yes” only if IMF PortWatch shows a 7-day moving average of transit calls of at least 60 by April 30. Kalshi’s return-to-normal and weekly traffic markets use similar threshold logic. These contracts are not about peace, they are about the actual traffic flow.

A diplomatic-settlement contract prices formal political de-escalation. Polymarket’s “US x Iran ceasefire by…?” market requires an official, mutually agreed halt in direct military engagement. Informal pauses or backchannel de-escalation do not count. That makes it fundamentally different from a traffic market. It prices a political state, not operating throughput. It is also much deeper, with roughly $65.6 million in volume versus about $1.64 million for the traffic-normalization market on Polymarket.

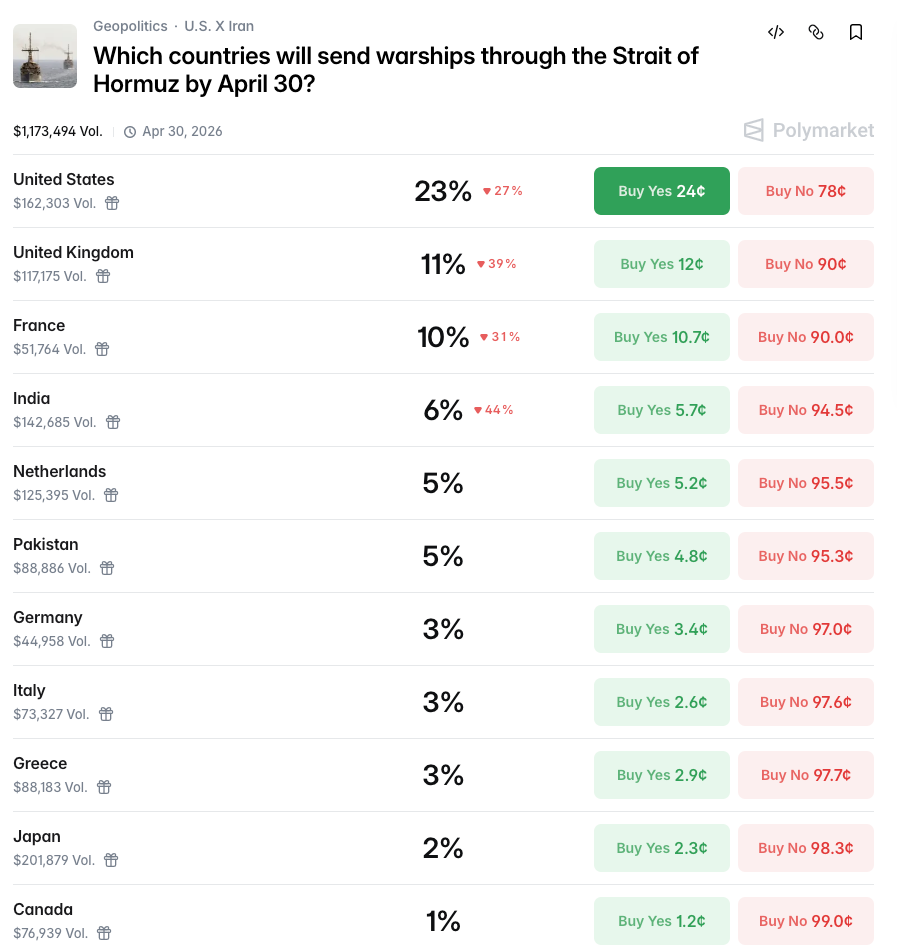

Finally, military-facilitation contracts price whether a security mechanism emerges that could enable partial reopening. Polymarket’s warship-transit market is the clearest example. It resolves based on confirmed warship passage through the strait itself, not just broader naval presence in the region. So it is best read as a market on a possible reopening mechanism, not on peace or traffic directly.

3.2 Why Kalshi and Polymarket feel a bit different

The cleanest practical difference between the two platforms is: Kalshi looks more like a threshold-and-throughput platform; Polymarket looks more like a layered geopolitical menu.

Kalshi’s Hormuz contracts are mostly binary or threshold-based. Polymarket, by contrast, is more willing to use multi-outcome structures. The ceasefire market is a date array, and the warship market has 11 outcomes.

That is not just a cosmetic design choice. Binary threshold products are naturally good at answering “Has this physical condition been met?”. Multi-outcome products are better at expressing timing distributions or outcome identity. That gives Polymarket a wider narrative range, but it also means you have to read the rules more carefully because similar headlines can resolve on very different criteria.

In that sense, the two platforms are often better viewed as complementary than as direct substitutes.

From curious to confident. Join the sharpest forecasters online, get top contracts, platform updates & market signals - free.

Why "7 Days" Matters: Not 2 Days or 14+ Days

The contract "Will Iran effectively close the Strait of Hormuz for 7+ days?" on Kalshi has attracted around $7.3M traded volume, despite the fact that the first market ("Before 2027") was opened in early-January and the remaining markets ("Before May" and "Before August") were opened on 1st March as follow-ups. This contract probably has the highest traded volume among Hormuz-related events (excluding broader Iran-related events) across Kalshi and Polymarket.

This naturally triggers curiosity for prediction market operators and active thinkers: "Why does a 7-day closure of the Hormuz Strait receive so much attention? Why isn't the contract focusing on a shorter or longer period of closure?"

It is important to be explicit that primary rule pages from Kalshi and Polymarket do not publish white papers outlining this exact economic rationale. The market rules clearly define how the markets will resolve, but they do not explicitly justify why 7 days was chosen over 5 or 10 or another number.

Conclusion first: this threshold is the best inference drawn from the broader maritime and economic environment, though the choice is also likely driven by prediction market platforms' practical need to aggregate low-volume trade data into statistically robust, standardized weekly trading cycles. Or it could be that, though less likely, this is just an arbitrary threshold set by Kalshi.

4.1 Not every disruption is a closure

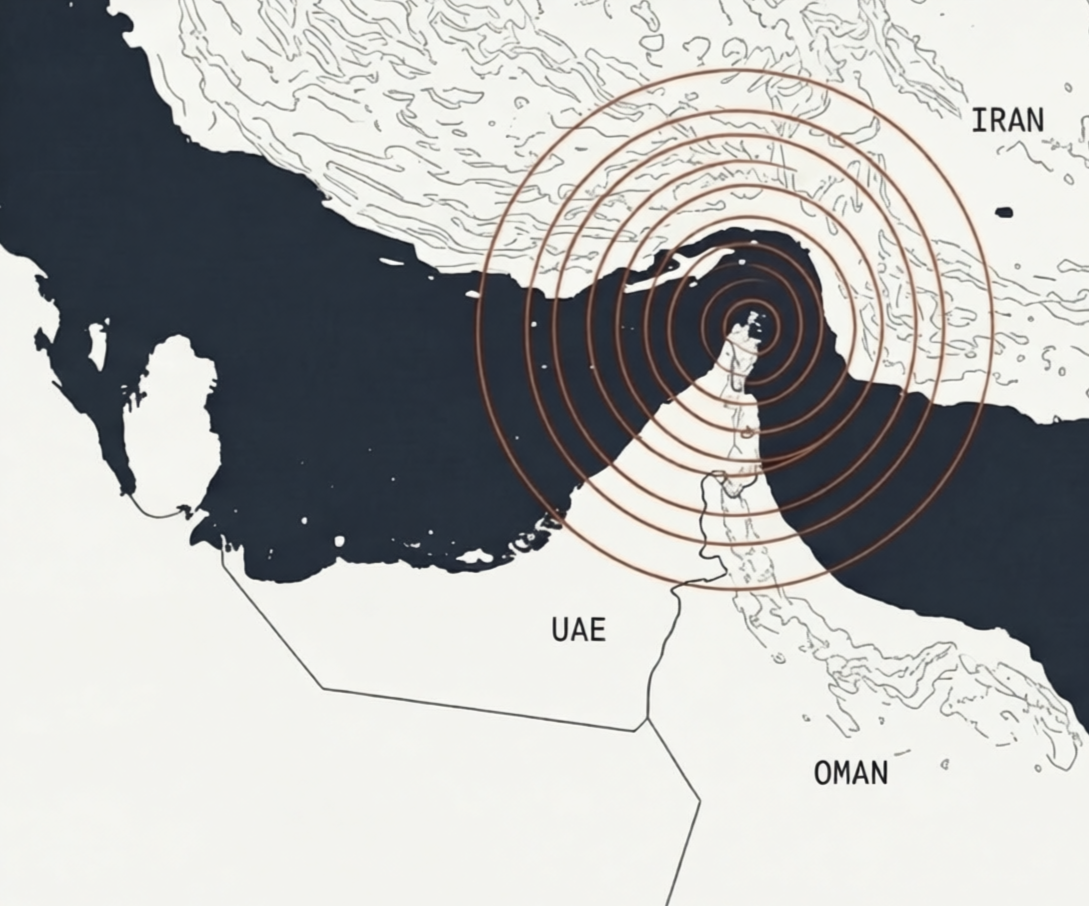

In this context, defining the "effective closure" of a vital maritime chokepoint cannot rely on the binary rhetoric of state actors or a single day of halted traffic.

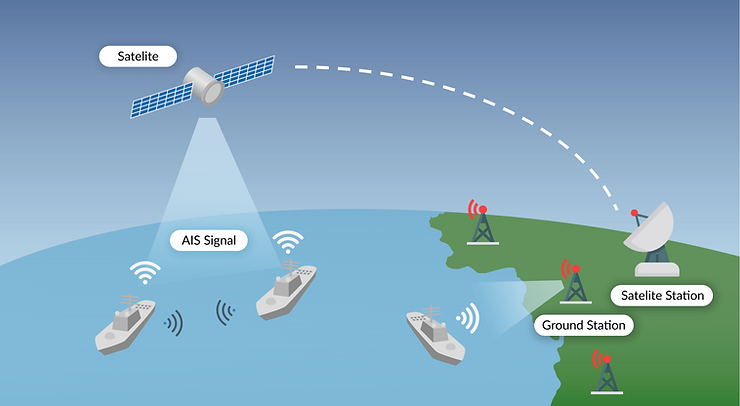

Maritime traffic data, primarily sourced from the Automatic Identification System (AIS), is inherently volatile on a day-to-day basis. Daily transit counts are subject to transient factors, including normal berthing delays at major transshipment hubs, fluctuations in loading schedules, and environmental impediments such as heavy seas.

In a conflict environment, this baseline volatility is compounded by tactical anomalies, including GPS jamming, AIS spoofing, and vessels intentionally "going dark" to avoid targeting.

Consequently, brief disruptions lasting only one to three days are frequently driven by tactical noise rather than a persistent disruption regime. The history of the Hormuz Strait shows that short gaps in transit may be the result of temporary inspections, military exercises, localized incidents, or environmental hazards.

Thus, resolving a contract based on a 24- or 48-hour disruption would risk triggering a "false positive", rewarding speculation on temporary headline volatility rather than a structural regime shift with true global economic consequences.

4.2 Why is 7 days a meaningful threshold?

A 7-day window represents the precise horizon where transient friction transforms into a structural crisis.

Operationally, some contracts on Kalshi and Polymarket utilize a 7-day moving average of vessel transits through the Strait in their resolution rules, in order to filter out daily AIS noise and capture a full weekly operational cycle.

Economically, the commercial insurance landscape undergoes a total transformation by the 7-day mark. The most potent mechanism for closing a maritime chokepoint is the withdrawal of commercial insurance rather than physical blockade.

When kinetic escalation occurs at Hormuz, marine insurers activate "72-hour War Cancellation Clauses", creating a 3-day notice period that forces shipowners to exit the risk zone or secure replacement coverage at significantly higher rates before existing policies are cancelled.

Following the expiration of these notices, the market enters a phase of weekly resets. War-risk coverage is often repriced every 7 days to reflect the rapidly evolving threat environment, usually resulting in multi-fold premium increases that can possibly reach 10% of a vessel's hull value. If the strait is inaccessible for 7 days, the initial wave of covered voyages has ended, and the global fleet operates under a prohibitively expensive new insurance regime.

4.3 Why not 14+ days?

A 14+ day threshold would capture a very serious disruption, but for an event contract it is usually too late.

By the time a Hormuz disruption has lasted two weeks, shipping lines have often already rerouted vessels, insurers have already raised war-risk costs, and freight markets have already repriced. At that point, the market is no longer asking whether the disruption is real. It is already dealing with the consequences.

That is why a 7-day threshold works better. A one-week threshold is long enough to filter out short-lived noise, but still able to hedge against uncertainties before the global economy fully adapts to the new normal.

Singapore Minister Says Worst Case on War is Not Fully Priced

Click on the Bookmark to read Article 3 of the Series

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.