A song called “Earrings” by Malcolm Todd suddenly reached No. 1 on Spotify’s U.S. daily chart on June 30. That would usually be a music story. Maybe the song went viral. Maybe TikTok pushed it. Maybe listeners just found it at the same time.

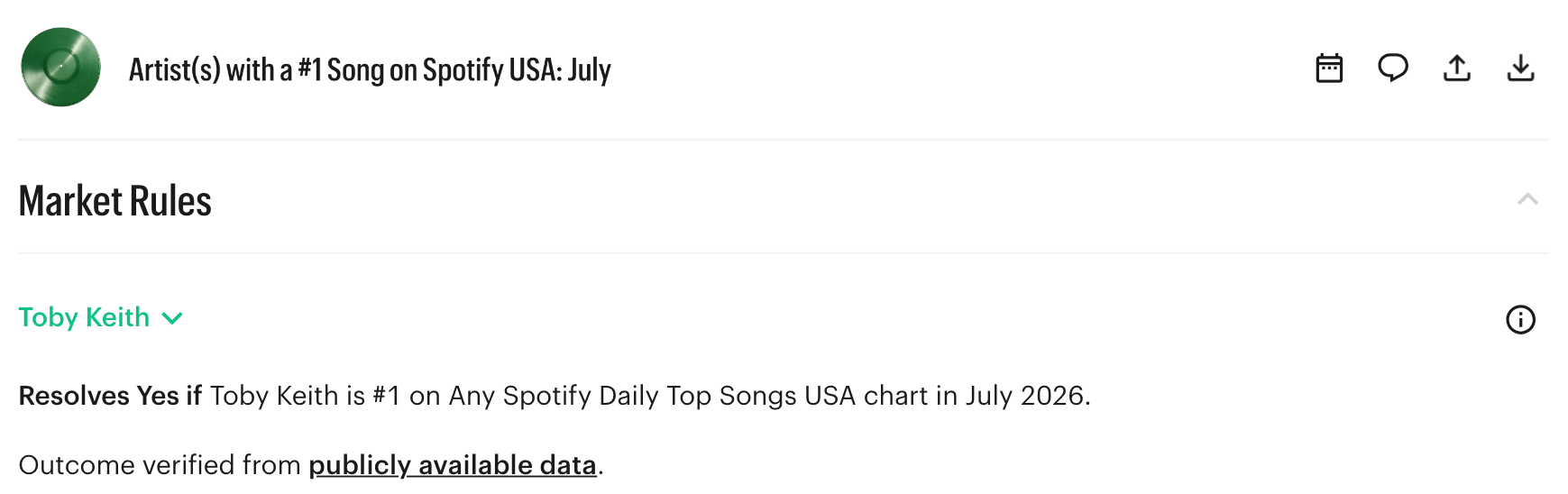

But the song was also tied to a prediction market on Kalshi. The market resolves Yes if the named artist is No. 1 on “Any Spotify Daily Top Songs USA chart in June 2026”, with the outcome verified from Spotify. The market was “Paid out 30 minutes after closing” according to the market page.

Malcolm Todd had been a long shot. Kalshi traders had priced his chance at roughly 2.5% before the dramatic move. Then Kalshi paid out, and Spotify later removed more than 500,000 artificial streams, pushing the track from 1st to 4th after review.

The problem was not simply that Spotify had fake streams. Spotify already has systems for artificial streaming. The problem was that the market paid out before Spotify’s correction arrived.

In other words, the prediction market settled on the first version of the data, not the corrected version.

That turns this from a music-industry story into a market-design story.

The incident

The trader who pushed the issue into public view was Caleb Davies, known as Gaeten Dugas on X (@GaetenD). WIRED described him as a major Kalshi culture-market trader who closely tracks Spotify data, and reported that he contacted Spotify, Kalshi, and Polymarket with concerns about what he believed was bot-driven manipulation.

Davies posted that the “Earrings” move was wildly abnormal. In one X post, he said the Sunday-to-Monday surge was an 11.24 sigma event, or roughly a 1 in 77 octillion chance of happening randomly.

As we await the final June Spotify update, one last look at how unlikely yesterday's Earrings surge was to have occurred by chance. Looking at the dataset of Sunday to Monday changes, it was a 11.24 sigma event, or a roughly 1 in 77 octillion chance of happening randomly. pic.twitter.com/Mklz784UDo

— Gaeten Dugas (@GaetenD) July 1, 2026

After Kalshi paid out, Davies also wrote on X that he had asked Kalshi not to pay the Spotify market until it investigated. Instead, he said, Kalshi “rushed to pay it out” and Spotify later removed the streams that gave “Earrings” the win. He lost about $4,500 on that.

Yesterday I requested that Kalshi not pay out the Spotify market until they investigated it. Instead, they rushed to pay it out mere hours later. Today, Spotify removed the streams that gave Earrings the win yesterday. It should have been in 4th place, not 1st. pic.twitter.com/YTcc6TQrZL

— Gaeten Dugas (@GaetenD) July 1, 2026

There are two important caveats. First, Spotify confirmed artificial streaming, but it did not confirm that the motive was prediction-market manipulation. Second, there is no public evidence that Malcolm Todd or his team were involved. Todd might simply have been an innocent bystander.

The race: manipulation, detection, payout

Spotify is not blind to artificial streaming. Its own guidance says artificial streams include streams that do not reflect genuine listening intent, including attempts to manipulate Spotify using bots or scripts. Spotify also says artificial streams do not earn royalties, do not count toward public stream numbers or charts, and do not positively influence recommendation algorithms once detected.

So Spotify has a cleaning process. The problem is timing.

Kalshi’s broader streaming-rank rules state that the underlying is the ranking published by the platform as of a given date, and that revisions made after expiration are not counted in determining the expiration value.

If Spotify catches the fake streams and removes them before the market settles, the manipulation fails. If Spotify catches them after the market settles, the exchange may already have paid the wrong side.

That means the key race is not simply between honest traders and dishonest traders. It is a race between three clocks:

- The manipulator’s ability to move the metric before the market deadline

- Spotify’s ability to detect and remove artificial streams

- Kalshi’s payout clock

In this case, Kalshi’s payout clock appears to have been faster than Spotify’s correction clock.

But the deeper issue is not just that settlement was fast. It is that the contract used a third-party benchmark whose first reading could later be corrected, and then treated that provisional reading as final. The loophole exists when an event contract finalizes before the benchmark source has finished deciding whether the benchmark itself was real.

This is why Spotify’s anti-fraud system does not fully solve the prediction-market problem. Spotify can still clean the chart later, remove fake streams, and withhold royalties. But if the exchange has already paid out, the financial damage inside the prediction market has already happened.

For Spotify, a delayed correction may be acceptable. For a prediction market, it may be too late.

Kalshi API data shows that in the Spotify market that was manipulated, traders who put money on the wrong side of Malcolm Todd collectively lost a total of $145,000 unwittingly betting against bot streams pic.twitter.com/FykNPZBklr

— Bobby Allyn (@BobbyAllyn) July 3, 2026

No-side buyers of the Malcolm Todd contract lost roughly $145,000 in total before fees.

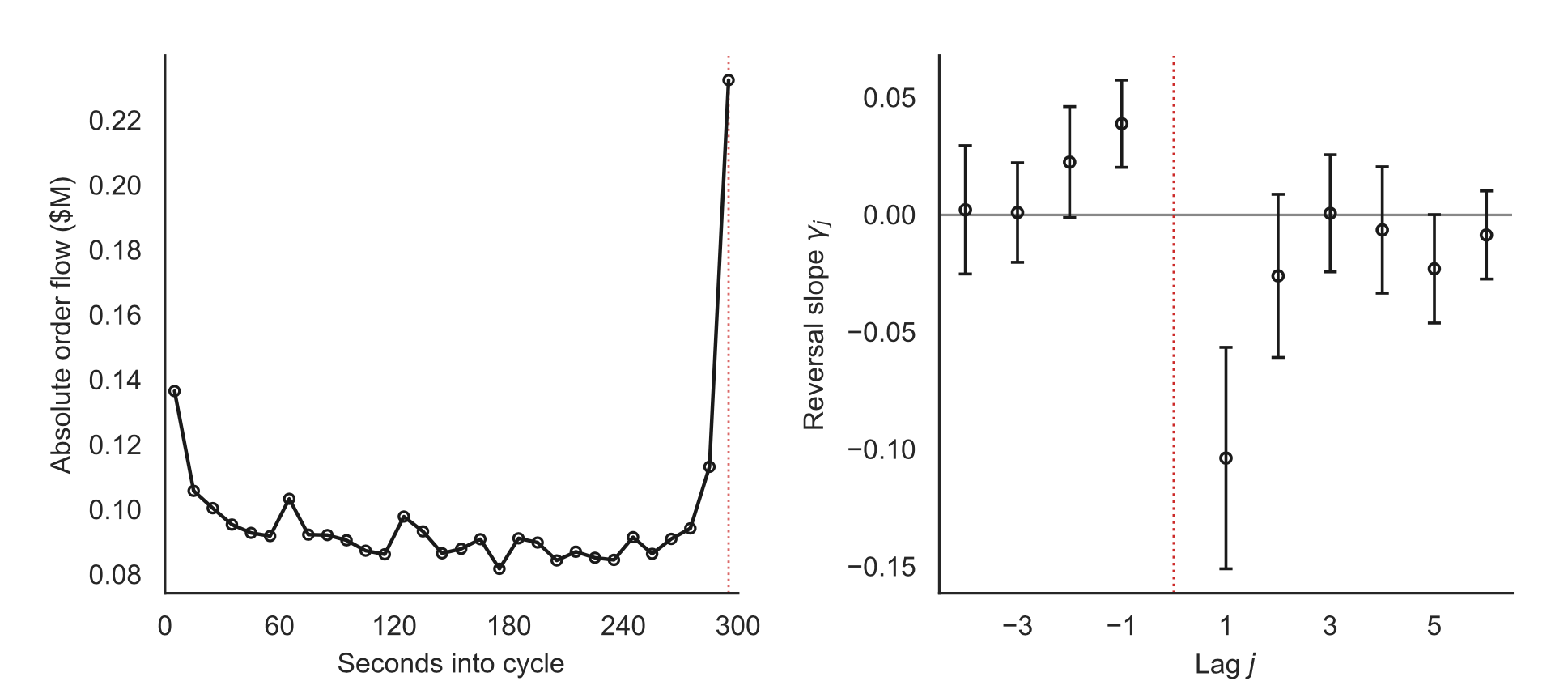

BTC 5 mins settlement manipulation

This case also rhymes with the issue in short-duration crypto prediction markets.

A recent paper on settlement manipulation in prediction markets studied Polymarket’s 5 mins Bitcoin contracts. The authors found that after those contracts launched, order flow spiked on the BTC spot market around when the event contract settles, and prices often reversed after settlement of the event contract.

Their interpretation is that, if a contract pays based on the BTC price at a very specific moment, traders can profit from the event contract by briefly pushing the underlying BTC spot price across the settlement threshold.

In the BTC case, the trader tries to move the price at the settlement moment. In the Spotify case, the trader tries to move the chart before the market deadline and Spotify's correction.

The exact tools are different. One uses trading in the underlying asset. The other may involve artificial streams. But the logic is similar: If a market pays on a temporary value, someone may try to manufacture that temporary value.

There is one important difference, though. A BTC price at a specific timestamp is still a real traded price, even if it was pushed around. It usually will not be “revised away”. Spotify streams are different. Spotify can later correct the stream numbers.

So BTC five-minute markets are mainly about settlement-price manipulation. The Spotify case is about settlement-source contamination.

The third-party source problem

Spotify did not design its charts to be financial settlement infrastructure. But once exchanges create markets based on Spotify charts, those charts become settlement benchmarks.

That changes the incentives around the charts.

Before prediction markets, artificial streaming was mainly about royalties, playlist placement, social proof, or artist promotion. With prediction markets, there is a new possibility: someone can profit from the artificial streams without being the artist, the label, or the distributor. They do not need Spotify royalties. They just need the chart to hit the right number before the market pays.

That creates a weird externality. The exchange creates the financial incentives, but Spotify has to deal with the mess. It has to detect the manipulation, clean the data, protect the chart, and answer questions about a market it did not necessarily ask to be part of.

Bloomberg reported that Spotify asked Kalshi and Polymarket to remove its logo and clarify that neither company had a partnership with the streaming service. WIRED also reported that Kalshi removed Spotify’s logo from related markets and changed language that had suggested Spotify verified chart results.

That reaction makes sense. If your data is being used to settle millions of dollars in contracts, you are no longer just a data publisher. You are being pulled into the role of an unwilling settlement agency.

The fundamental issue is not that prediction markets use outside data. They have to. The issue arises when the exchange relies on a third-party metric that can be influenced before settlement, audited after publication, and revised outside the exchange’s control. In that setting, the market is not simply importing clean information from the real world. It is importing a provisional benchmark whose validity may only be decided after traders have already been paid, subject to the source's discretion.

How should exchanges settle markets based on platform metrics like Spotify charts?

If an exchange settles on the latest result available at the end of a defined review window, how long should that window be after the first result is published?

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.