In the Denmark vs. Ukraine international friendly on June 7, 2026. Denmark were leading 2-1 when the Danish player Christian Eriksen collapsed on the pitch. The match was suspended and then abandoned.

Eriksen was reported to be conscious, doing well under the circumstances, and taken for further medical checks 🤞.

But once the immediate shock passed, prediction-market traders were left with a technical question: if Denmark were leading 2-1 when the match was abandoned, did Denmark “win” for settlement purposes?

On Kalshi, the answer appeared relatively straightforward. The Denmark contract resolved Yes, while Tie and Ukraine resolved No. There was not much public controversy around that settlement.

On Polymarket, the same underlying event generated more discussion and dispute. Traders argued about whether the market should resolve Denmark Yes, follow cancellation logic, or be treated as an abnormal edge case.

Argument for Denmark YES on Polymarket

The strongest argument for Denmark YES is textual.

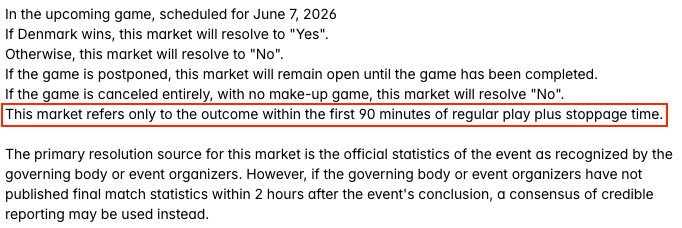

Polymarket’s moneyline rule says the market refers only to the outcome “within the first 90 minutes of regular play plus stoppage time.” This clause is usually used to exclude extra time & penalties, and clarify that the focus is on the regular-time window.

Denmark’s 2-1 lead was obtained within the first 90 minutes of regular play. The goals had already happened. The scoreline existed before the match was abandoned. If the market is asking what happened within that regular-time window, then Denmark backers can reasonably argue that Denmark were the winning side under the relevant time condition.

The rule did not say “after 90 minutes have been completed.” It did not say “only if the full 90 minutes are played.” It did not say “at full time.” It said “within the first 90 minutes.”

This argument becomes stronger if major sports data providers or media pages record the result as Denmark 2-1 Ukraine. If the listed or widely accepted sources treat 2-1 as the match result, then Denmark YES holders can argue that the market should follow the official or credible recorded score.

In fact, FIFA, ESPN, and Fox Sports are all showing a 2-1 score on their websites. Interestingly, FIFA, and Fox Sports both display a “interrupted/cancelled” label next to the score, while ESPN display a “FT” label (“FT” = “Full Time”). The “FT” label seems weird since it usually indicates the result after the complete 90 minutes of play plus any stoppage time in sports market.

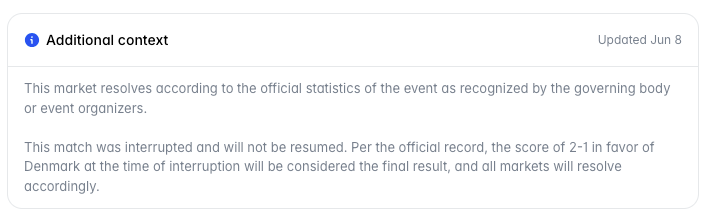

Polymarket added a clarification on June 8, stating that the 2-1 score in favor of Denmark at the time of interruption will be considered the final result. This directly supports the YES argument. However, this clarification appears to have been added only after the dispute had already emerged, rather than being clearly visible to traders before resolution. In that sense, it does not fully remove the concern that the original public-facing rules left too much room for interpretation.

Argument for Denmark NO on Polymarket

The strongest argument for Denmark NO is based on sports-market convention and match-completion logic.

In football betting, a moneyline or regular-time market usually means the result after 90 minutes plus stoppage time. The phrase “within 90 minutes” is often used to exclude extra time and penalties. It is not usually meant to say that whoever is leading at any point before minute 90 has already won the market. If Denmark lead 2-1 in minute 64 of a normal match, that is not yet a Denmark win. The market outcome is usually determined at the end of regular time, not at an intermediate point.

From this perspective, Denmark were leading, but they had not yet completed a regular-time win.

The Denmark NO side can argue that “within the first 90 minutes” should be understood as “the regular-time result,” not “the score at abandonment”, as per the conventions. If regular time was never completed, then there was no valid regular-time outcome.

There is a stronger cancellation or abandonment argument.

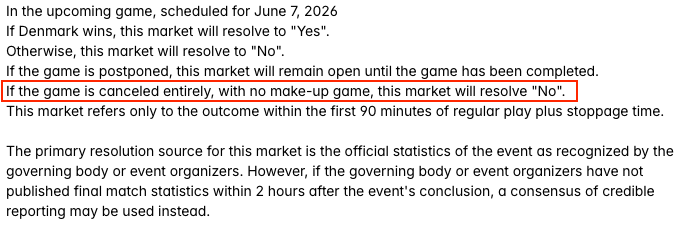

Polymarket’s rule says that if the game is canceled entirely with no make-up game, Denmark resolves No. From this perspective, the key issue is whether an abandoned match with no continuation or replay should be treated as a canceled game under the market rules. If yes, then Denmark should resolve No despite the scoreline at the time of abandonment.

This framing shifts the debate away from the legitimacy of the score and toward the hierarchy of the rules. Denmark NO holders can respond that the market also had a cancellation fallback, and that fallback should apply when the match was not completed and no make-up game is played.

The real ambiguity is that Polymarket’s rule did not clearly say whether “canceled entirely” includes a match abandoned after kickoff. This creates room for arguments in favor of YES holders.

The same market on Kalshi

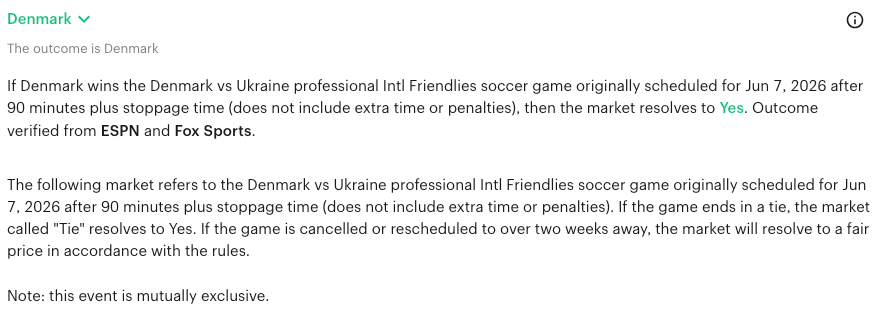

Kalshi’s market on the same match resolved Denmark Yes, Tie No, and Ukraine No. It also named ESPN and Fox Sports as verification sources.

The important difference is Kalshi’s broader soccer contract terms. Those terms included a clause stating that if an official result is reported even though the event was truncated or ended early, the market resolves based on that reported result.

That clause changes everything as Kalshi did not need to resolve the philosophical question of whether a 64-minute match is equivalent to a completed 90-minute match. The rulebook already anticipated the relevant edge case. It recognized that sports events can be truncated or ended early, and it told traders what happens if an official result is still reported.

Polymarket should borrow that kind of rule hierarchy for live sports markets. A better football-market rule should say exactly what happens in each abnormal scenario.

Resolution process

Polymarket’s resolution process is more open and more social. Its oracle-based system allows outcomes to be proposed, disputed, discussed, and potentially escalated. This can be useful because it gives market participants a way to challenge bad resolutions. But it also means that edge cases can become public coordination games.

Here is another recent incident of resolution dispute on Polymarket.

Kalshi is more centralized. Its rulebook and settlement process give the exchange more direct authority. Traders can still disagree, but the disagreement is less likely to become a long public dispute.

Polymarket exposed traders to more visible oracle risk. Kalshi reduced that risk by using a more centralized resolution process. This does not mean Kalshi is always better (and I have no financial association with either party). A centralized exchange can still make controversial decisions. But in this specific case, Kalshi’s rule structure gave traders fewer points to fight over.

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.