Brent fell around 4% after Reuters reported that the two sides had reached a preliminary agreement to end the war and reopen the Strait of Hormuz, with a formal memorandum expected in Switzerland and broader nuclear and sanctions talks pushed into a 60-day ceasefire window.

A closed Hormuz was the nightmare scenario for energy markets. Once traders saw a path to reopening, the most extreme blockade premium had to come out of the curve. But the more important point is that financial markets can reopen in a minute, while physical energy systems reopen in stages. The peace deal changes the nature of the crisis, but it does not instantly undo the logistical, refining, inventory and demand damage created over the past three months.

Reuters already shows the gap between headline and reality. On the first trading day after the agreement, only one LNG tanker, Petronet’s Disha, passed through the strait, while shippers continued to wait for details on mine clearance and safety assurances. Kpler estimated 155 oil and chemical tankers in the Gulf area on June 15, while Oil Brokerage’s estimate was 215, and even under unrestricted navigation Oil Brokerage said the traffic pile-up would take 8-10 days to clear. That is the cleanest way to understand the post-deal phase: the blockade risk may collapse quickly, but the physical recovery will be much slower.

This was not another Russia-Ukraine-style oil shock

A useful starting point is to distinguish the Hormuz crisis from the Russia-Ukraine shock in 2022. In the Russia case, the first market panic was about whether Russian barrels would disappear. But over time, many of those barrels were rerouted. Russian crude that previously went to Europe increasingly moved to buyers such as India and China. The shock was severe, but it was largely a redirection shock.

Hormuz was different. Before the conflict, according to the IEA, roughly 20 million barrels per day of crude and oil products were moving through the strait, equivalent to about 25% of world seaborne oil trade, with around 80% destined for Asia. And the crisis created actual losses of supply rather than merely changing the destination of cargoes.

That distinction is important because re-routing is a price problem, while physical blockage is a system problem. If oil is merely rerouted, the market pays more for shipping, insurance and time. If the oil cannot leave, producers shut in output, storage fills, refiners lose feedstock, and consumers are forced to reduce usage.

The quality problem: not every barrel is the same

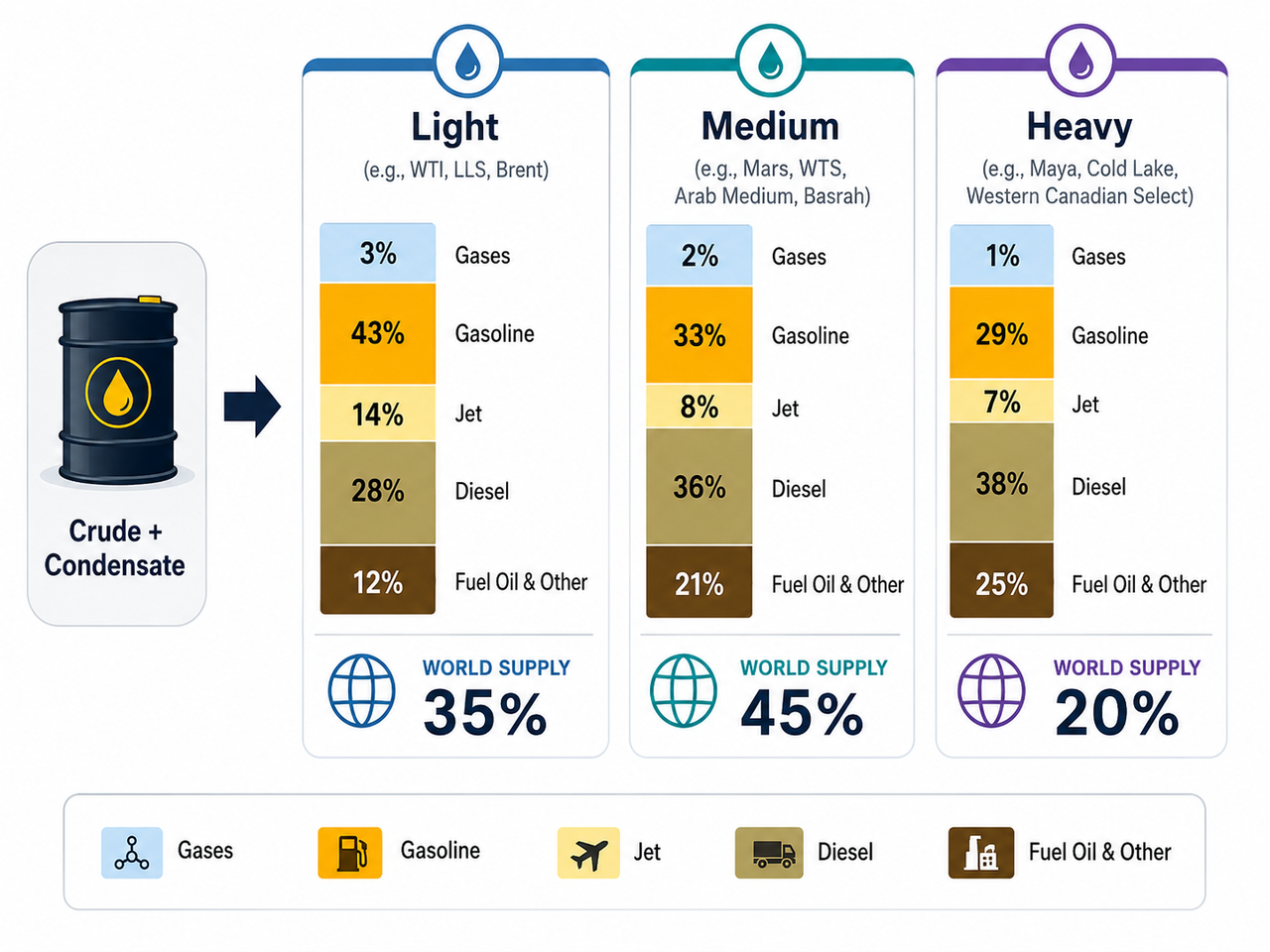

On the other hand, the public discussion often treats oil as a single commodity, but the refining system does not. Middle East Gulf exports are mostly medium-to-heavy sour barrels, and many Asian refiners are configured around those grades. Replacement barrels from the US are generally lighter and therefore less useful for Asian refiners trying to replicate their normal product yield.

This is a major reason why emergency stock releases and alternative supply cannot fully solve the problem. The IEA coordinated stock release helped, but much of the emergency crude available from IEA countries is Atlantic Basin crude, not the medium-heavy sour crude Asian refiners normally want.

In other words, the market does not just need “more barrels.” It needs the right barrels in the right place with the right logistics. That is what Hormuz restores, and it is also why reopening matters so much for Asia.

Reopening Hormuz is a sequence, not a switch

The first bottleneck is legal and security clearance. A peace framework does not automatically make shipowners comfortable sending vessels through a waterway that was effectively closed for months. Reuters reported that Japanese shippers welcomed the agreement but wanted concrete details, especially around mine clearance, before resuming normal navigation. This is not excessive caution. Tankers are expensive, insurance is sensitive to war risk, and a single incident after reopening would immediately reprice freight and oil markets.

The second bottleneck is maritime traffic. Sources estimated that roughly 150 million barrels of oil were stuck in the Persian Gulf at the end of May, and that even an orderly exit could take up to around 30 days, stretching the recovery well beyond the first wave of vessel exits. Free passage would need to be built over weeks before the wider shipping community regained confidence.

The third bottleneck is storage and production. During the closure, production that could not be exported accumulated in onshore storage. Once storage fills, output has to be shut in. Restarting production requires empty tankers to enter the Gulf and drain those storage tanks before oilfields can return to normal. It is estimated that draining onshore inventories could require around 200 VLCCs, with 4-6 weeks needed for up to 5 million barrels per day of shut-in production to return and potentially 2-3 months for the remaining shut-ins.

The fourth bottleneck is infrastructure repair. An important warning is that Gulf producers and refiners would compete for equipment, steel, valves, pipes and skilled labor to repair damaged facilities, meaning the constraint is not only money but also physical repair capacity. This is crucial because energy infrastructure is not software. It cannot be patched globally overnight.

Therefore, the combined result is a staged recovery. First, headlines improve. Then some ships pass. Then insurance normalizes. Then inbound tankers return. Then storage drains. Then production restarts. Then refineries ramp. Then products flow. Only after that does the whole system return to normal.

Crude can fall before fuels become cheap

Brent reflects the financial market’s changing view of crude availability and geopolitical risk. But consumers do not buy crude oil directly. They buy gasoline, diesel, jet fuel, LPG, naphtha-linked goods and electricity generated through fuel-linked systems.

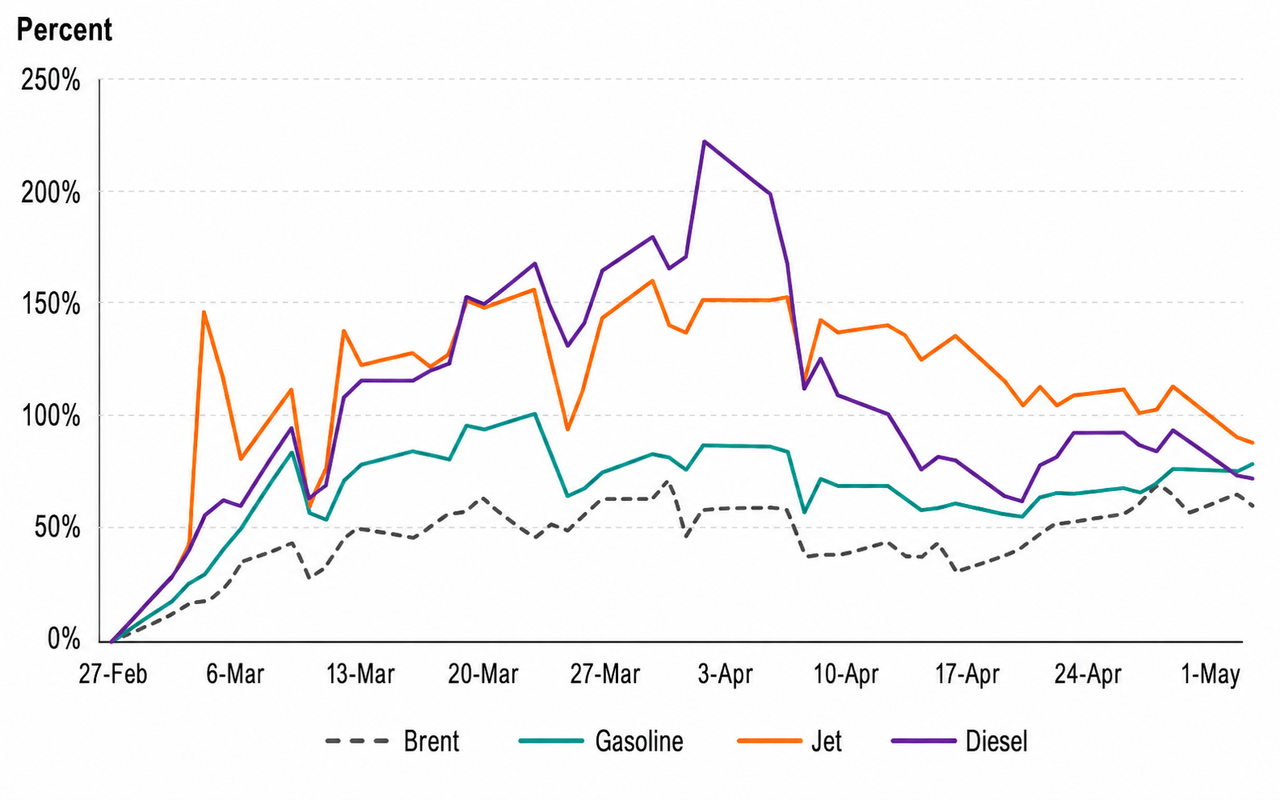

A disruption of this scale cannot be rebalanced through crude alone and the adjustment has already shifted downstream into refined products. From January through April, crude prices rose roughly 40%, while Asian refined product prices rose 60%-120%, meaning oil products repriced 1.5x-3x faster than crude.

This is why crude prices may fall first while fuel prices remain sticky. A peace deal removes some probability of prolonged closure. But product markets still face refinery outages, crude-quality mismatches, shipping delays and slow ramp-ups. Refiners cannot snap back to full rates after a prolonged shutdown, and that Middle East refinery run cuts near 3 million barrels per day could take 4-8 weeks to restore gradually.

That is also why the first phase of post-Hormuz price action may look contradictory. Crude benchmarks can fall, equity markets can rally, and yet airlines, petrochemical producers and consumers may still face elevated costs. The crude market trades expectations while the product market reflects bottlenecks.

Jet fuel is the clearest example. Jet fuel was the most acutely affected product, with prices nearly doubling across Asia, Europe and the US and jet cracks widening to $80-$100 per barrel over crude. But refining is a mass-balance system. If refiners try to maximize jet fuel, they usually reduce diesel output, and diesel sits at the center of trucking, shipping, rail, agriculture and mining.

This means the reopening of Hormuz does not just answer “where should Brent trade?” It creates a second question: which part of the refined-products system heals last?

Demand destruction does not instantly reverse

The market partially balanced during the crisis because demand was damaged. That sounds bearish for crude, but it is also a sign of economic stress. Sources estimated that observable global oil demand fell by 2.8 million barrels per day in March and 4.3 million barrels per day in April, with losses expected to deepen to around 5.6 million barrels per day in May and 5.0 million barrels per day in June.

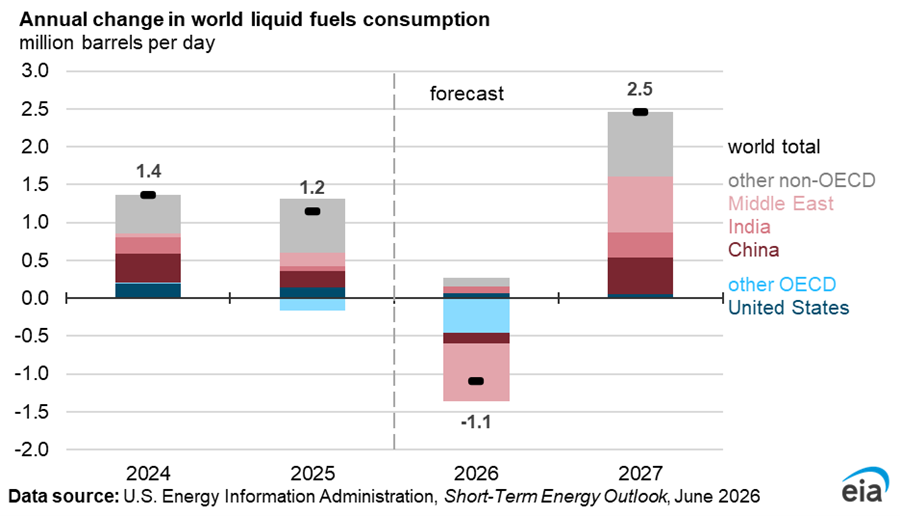

The EIA also says high fuel prices, reduced fuel availability and government initiatives have lowered oil demand, with most of the demand reduction in Asia because the region receives more crude supplies from the Middle East. It now forecasts global oil demand to fall by an average of 1.1 million barrels per day in 2026, compared with its previous expectation for growth, before rebounding by 2.5 million barrels per day in 2027 as prices drop and supply flows return later in 2026.

The IEA’s May Oil Market Report estimates that output from Gulf countries affected by the Hormuz closure was 14.4 million barrels per day below pre-war levels, while refinery crude throughputs are forecast to fall by 4.5 million barrels per day in 2Q26 because of infrastructure damage, export restrictions and lower feedstock availability.

This creates a rebound problem. When supply returns, demand does not automatically jump back to its old path. Airlines may have cancelled routes. Petrochemical plants may need to restart gradually. Households may have adjusted behavior. Governments may keep conservation measures in place. Inventories may be rebuilt before end-use demand fully recovers.

That means the post-reopening market may go through two opposing forces. On one side, supply improves and crude prices fall. On the other side, demand gradually recovers as fuel availability improves. The net price path depends on which side moves faster.

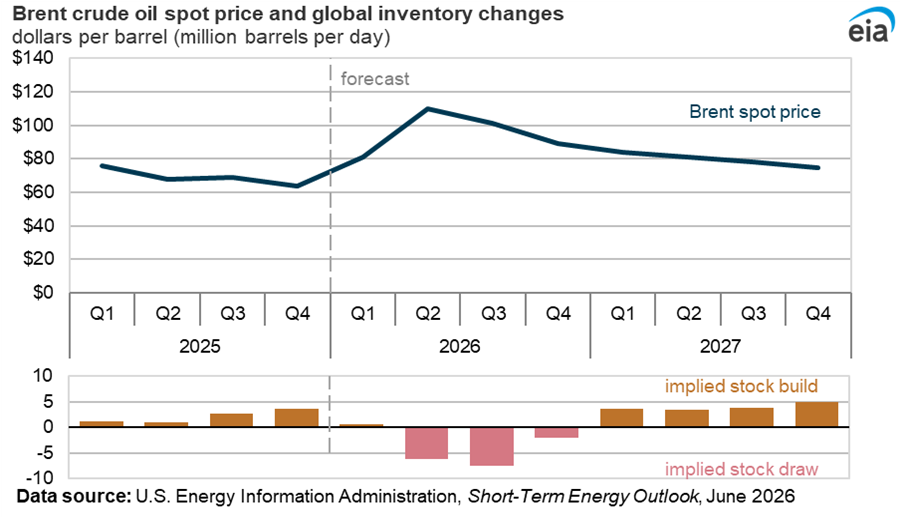

The EIA captures this tension well. Because global inventories have been drawn down sharply, it expects oil prices to remain elevated until flows normalize and inventories are replenished, and it estimates global inventories will fall by 6.3 million barrels per day in 2Q26. The IEA similarly says observed global inventories, including oil on water, were drawn down by 250 million barrels over March and April, and that resuming flows through Hormuz remains the single most important variable in easing pressure on energy supplies, prices and the global economy.

What happens next

The cleanest way to think about the next phase is not “open or closed,” but “how fast does the system heal?”

In the best case, the formal agreement is signed, mines and security concerns are cleared quickly, insurers lower war-risk premiums, shipowners resume passage, empty tankers enter the Gulf, storage begins to drain and refinery runs step higher over the next 4-8 weeks. In that scenario, crude prices probably remain under pressure because the market moves from scarcity fear to recovery pricing. Product prices would also ease, but with a lag because refineries and feedstock supply chains need time.

In the middle case, the strait technically reopens, but shipowners remain cautious, political terms are unclear, the 60-day negotiation period creates headline risk and traffic normalizes only gradually. This is the scenario implied by Reuters’ early shipping reports: one tanker passes, many remain stuck, and confidence has to be rebuilt over weeks rather than hours. In this case, Brent may be capped by peace optimism, while product cracks, freight rates and Asian fuel stress stay elevated.

In the downside case, the agreement becomes a ceasefire in name but not in practice. Any renewed military action, mine incident, insurance shock or dispute over Iran’s nuclear program could quickly reintroduce the risk premium. This risk is not theoretical because Reuters reported that the preliminary pact leaves Iran’s nuclear program to later talks and that Lebanon remained a sticking point in negotiations.

The most interesting possibility is that crude becomes bearish before the real economy becomes comfortable. If tankers exit and producers rush to recover revenue while demand remains depressed, crude could fall faster than refined products. That would not mean the shock is over. It would mean the bottleneck has shifted from crude availability to product availability, refinery configuration and end-user recovery.

What to watch

The key indicators now are different from the indicators during the closure. During the crisis, the main question was whether Hormuz could reopen. After the agreement, the key indicators are tanker transits, oil-on-water, inbound VLCC flows, refinery runs, and the stability of the US-Iran negotiation process.

A simple rule is useful: Brent tells you how the market prices the probability of reopening; oil product cracks tell you how the physical system is actually healing.

That is the deeper story of Hormuz. The peace deal is a turning point, but not a reset button. The visible blockade may end on a date. The energy shock unwinds through the supply chain over weeks or months.