Arbitrage desks looking to trade SK Hynix Inc.’s new American depository receipts are dusting off playbooks from Taiwan Semiconductor Manufacturing Co. But many say the comparison only goes so far.

Unlike TSMC, whose ADRs have decades of trading history that provide investors with a sense of where the premium to local shares tends to settle, SK Hynix’s ADRs begin trading for the first time on Friday. That leaves arbitrage investors without a historical benchmark for what constitutes a normal premium, making it far harder to judge when a spread is attractive or stretched.

The challenge extends beyond the lack of price history.

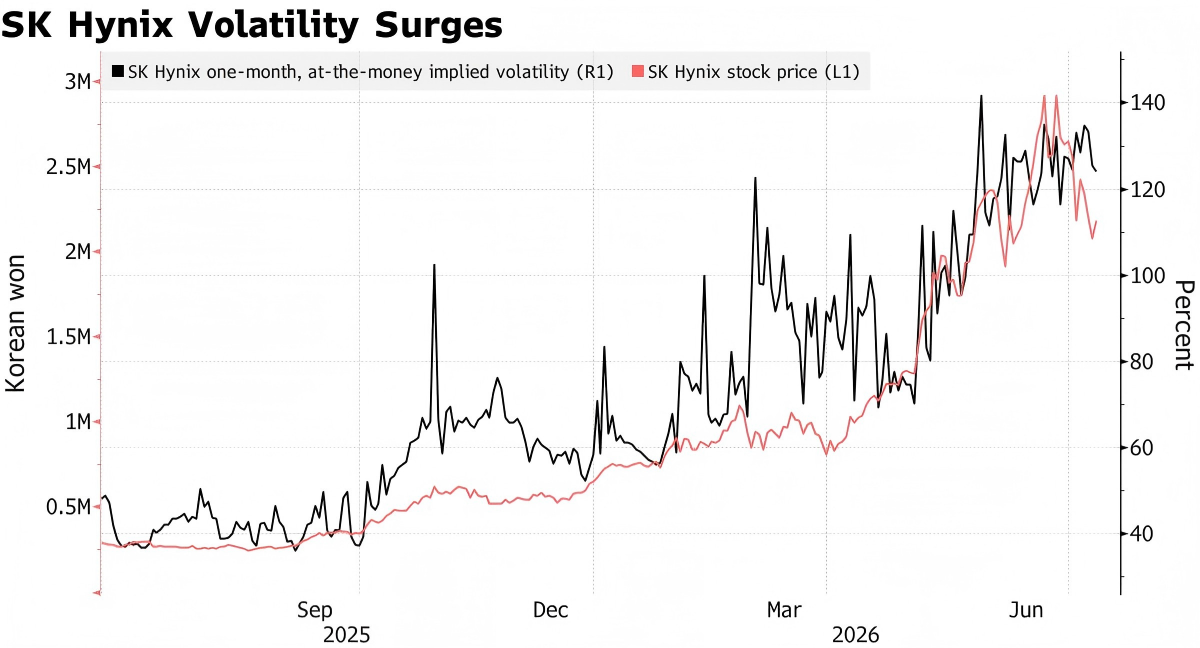

SK Hynix has become one of Asia’s most volatile large-cap stocks, regularly posting outsize daily swings as investors pile into AI-linked memory names and leveraged products tied to the shares. Those sharp moves increase the gap risk — the danger that the ADR and Seoul-listed stock diverge significantly from the trend the arbitragers were betting on.

“With SK Hynix’s volatility, the gap risk is much higher,” said Alex Au, managing director at Alphalex Capital Management HK Ltd., who traded TSMC’s ADR spread for years. “So for someone putting on this trade to capture the premium, you’d demand higher returns.”

Another uncertainty is the extent to which Seoul-listed shares can be converted into American depository receipts. According to a July 6 filing, holders of the US instruments will be able to cancel them and receive the corresponding number of Seoul-traded shares. But investors may not be able to later exchange the common stock for ADRs as such a transaction could require approvals such as permission from Korean regulators.

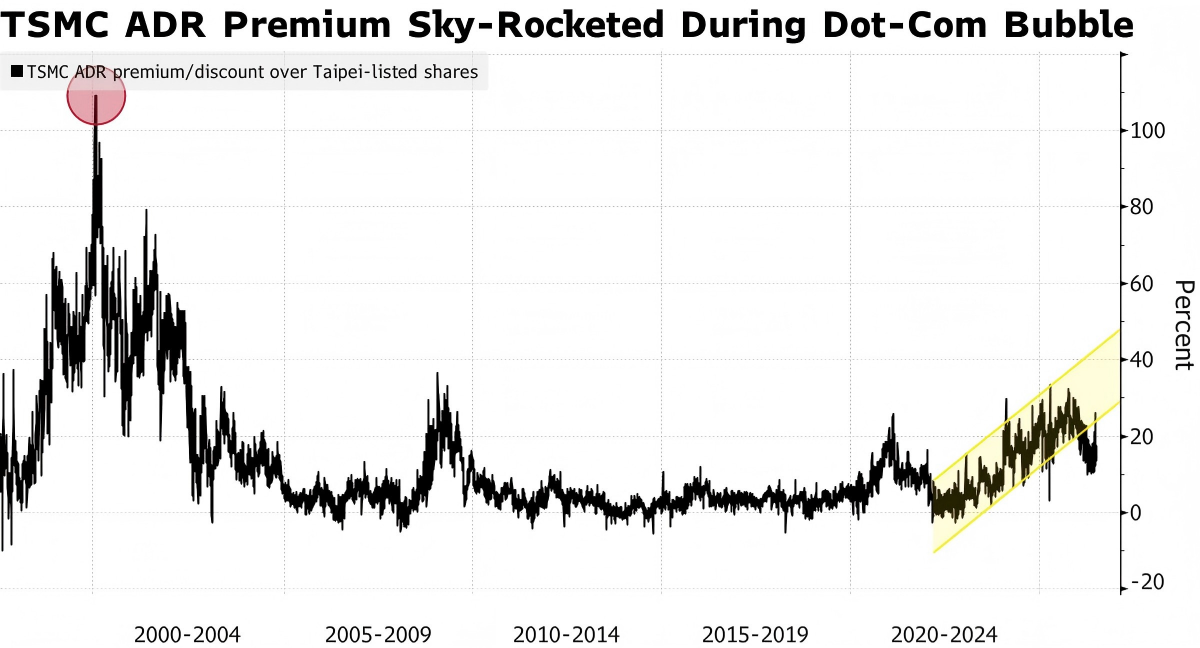

By comparison, traders have years of experience with TSMC’s partially fungible shares. Even though the spread has widened during the AI boom, investors have historical patterns to help assess when premiums become excessive and are likely to mean-revert.

TSMC’s ADRs traded at an average premium of 16% over the past month, according to data compiled by Bloomberg. The price difference largely showed a mean-reversion trend, which made it one of the most popular relative value trades before the current AI frenzy distorted the dynamic.

Institutional investors have floated estimates for an initial premium for the SK Hynix ADR ranging from about 5% to more than 30%, underscoring just how uncertain the market remains ahead of the debut. Morgan Stanley’s sales and trading desk on Wednesday estimated the gap in the 5% to 10% range, with scope to increase if the ADR is included in US indexes or exchange-traded funds, according to a note to institutional clients seen by Bloomberg.

Will SK Hynix ADR close at a premium of at least 16% to its Seoul-listed shares on its first trading day?

“Until it has seasoned, nobody will know what that premium is worth from day to day,” said Travis Lundy, an independent special situations analyst who publishes on Smartkarma. “History shows they can go high but don’t stay super high.”