Reading the trajectory of AI infrastructure demand through the industry's purest — and riskiest — case study.

1.The Purest Tech Case Study (Introduction to the Meta Proxy)

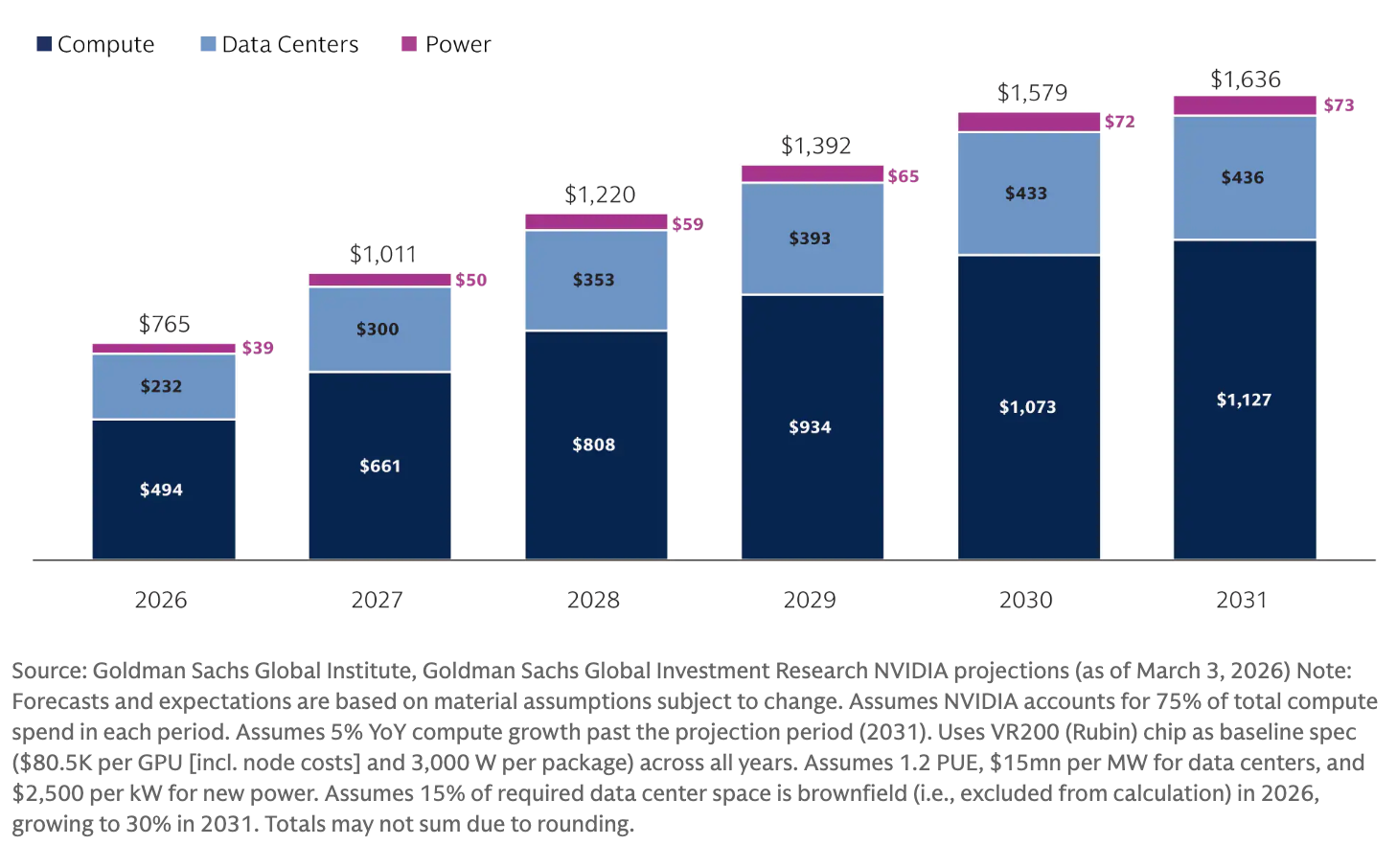

As the global financial system absorbs nearly $1 trillion in physical AI infrastructure, institutional skepticism is rising over the revenue gap. As Nicolai Tangen of Norway's sovereign wealth fund (NBIM) warned, a structural imbalance persists between the $1.4 trillion in projected global hardware expenditures and direct, verifiable AI revenues that struggle to cross $13 billion worldwide. In an era where markets demand proof of operational conversion and end-to-end viability, Meta emerges as the industry's most radical analytical proxy.

Unlike Microsoft’s Azure, Google’s GCP, or Amazon’s AWS, Meta operates as the purest unhedged bet in the generative AI landscape. The company possesses no external B2B cloud computing business to lease excess server capacity, monetize third-party compute, or subsidize its silicon infrastructure. Consequently, management's staggering CapEx guidance—officially projected between $125 billion and $145 billion for the fiscal year 2026 —must be justified entirely through internal monetization. Without a cloud safety net, every dollar spent on server farms and the pursuit of "superintelligence" represents an unhedged macroeconomic wager, completely reliant on translating brute compute power into ad-targeting efficiency and user engagement across Reels and Instagram.

2. The CapEx Wall and the Inference Tax

The paradigm of the modern internet economy is undergoing a structural mutation. For two decades, tech scaling relied on the zero marginal cost framework of traditional software. Generative AI shatters this foundation. Every prompt, synthetic recommendation, and AI-driven ad placement requires dedicated silicon cycles and immediate electron consumption. This reality imposes a permanent Inference Tax directly on Meta’s Cost of Revenue, structurally shifting it from an ethereal asset to a heavy-industry operating expense.

As Forrester Research highlights, this shift has created a "Pilot Graveyard," with 55% of global IT decision-makers admitting their legacy infrastructure cannot scale AI without severely eroding profit margins. For Meta, deploying generative models across its massive user base—particularly through its automated ad engine, Advantage+—means that higher engagement no longer yields pure profit. Instead, it triggers a linear surge in variable compute costs, threatening to permanently compress historically high gross margins under the weight of an unyielding CapEx wall.

Will Meta’s internal ad and engagement ROI justify its massive AI infrastructure CapEx over the next 24 months?

3. The Accounting Depreciation Cycle: From Assets to Liabilities

The current valuation of hyperscalers suffers from a profound market mispricing regarding AI hardware infrastructure. While traditional industrial assets provided decades of predictable utility, modern AI clusters powered by Nvidia H100 or Blackwell architectures are bound to a brutal 3-to-4-year economic and technical useful life before complete obsolescence. This rapid decay creates an economic trap: tech giants are not building permanent capital moats, but are locked in a treadmill of perpetual reinvestment just to maintain baseline compute competitiveness.

To temporarily mask this structural erosion of margins, companies like Meta have resorted to an opportunistic accounting maneuver—a depreciation schedule extension for servers from four to five or six years. While this book-keeping extension artificially cushions reported operating income, it cannot alter the hard physical reality of hardware decay. The unavoidable necessity of replacing obsolete chips every 36 to 48 months directly eviscerates Free Cash Flow (FCF), converting what Wall Street treats as long-term capital assets into recurring operational liabilities.

4. Hitting the "Watt Wall" (The Energy Limit)

The true technical ceiling for AI is not financial, but thermodynamic: The Watt Wall. While hyperscalers possess virtually infinite capital, they are colliding with a hard physical glass ceiling: power grid saturation. According to the IEA, data centers now absorb 22% of Ireland’s total electricity—forcing grid connection freezes in Dublin—and will devour 50% of US electricity demand growth by 2030. This structural deficit forces an intense Physical Crowding Out, where compute clusters displace heavy industry and residential grid electrification. To bypass these transmission bottlenecks, operators like Meta are desperately pivoting to dedicated baseload power, signing PPAs for 1.1 GW of existing nuclear and 150 MW of next-gen geothermal energy. Ultimately, money cannot print megawatts; without grid infrastructure, AI growth stops.

What will be the primary bottleneck throttling the hyperscalers' AI infrastructure boom?

Comprehensive Analytical Bibliography:

- Bank for International Settlements (BIS). (2025). BIS Quarterly Review: International banking and financial market developments. Basel: BIS, December 2025.

- International Energy Agency (IEA). (2026). Electricity 2026 Report: Global Infrastructure & Thermodynamic Trends. Paris: IEA.

- Norges Bank Investment Management (NBIM). (2026). Capital Allocation Doctrines and Institutional Mandates 2025/2026. Oslo: NBIM.

- Organisation for Economic Co-operation and Development (OECD). (2026). Compendium of Productivity Indicators. Paris: OECD, January 2026.

- Andreessen Horowitz (a16z). (2025). Where Value Will Accrue in AI: Structural Realities of Algorithmic Gross Margins. Research Briefing by Martin Casado and Sarah Wang.

- Bessemer Venture Partners & Meritech Capital. (2026). State of the Cloud 2026 & Meritech Software Pulse Index. New York/San Francisco: Open Access Multiples Matrix.

- Forrester Research. (2026). Predictions 2026: Artificial Intelligence and Corporate Infrastructure Stress. Cambridge: Forrester.

- Goldman Sachs Global Investment Research. (2024). Gen AI: Too much spend, too little benefit? Global Macro-Equity Strategy Briefing managed by Jim Covello.

- Goldman Sachs Global Investment Research. (2026). Tracking Trillions: The Assumptions Shaping the Scale of the AI Build-Out, by George Lee & Lucas Greenbaum.

- Morgan Stanley. (2026). US Software Outlook & Big Tech CapEx Projections. New York: Equity Research Division.

- Brynjolfsson, Erik, Daniel Rock, and Chad Syverson. (2019). The Productivity J-Curve: How Intangibles Complement General Purpose Technologies. Cambridge: National Bureau of Economic Research, Working Paper No. 25148.

- Chen, Xupeng. (2026). Abundant Intelligence and Deficient Demand: A Macro-Financial Stress Test of Rapid AI Adoption. Academic Working Paper, March 2026.

- Also includes Ccrporate filling files and briefing or media materials.