Why prediction markets betting on a V-shaped Venezuelan oil recovery are mispricing global liquidity, crowding-out effects, and Big Tech’s capital monopoly.

1. The Diplomatic Mirage vs. Physical Reality

Event contract traders on Kalshi and Polymarket are exhibiting a severe structural mispricing by wagering on a V-shaped rebound in Venezuelan crude output following the political transitions of early 2026. This consensus commits a fatal analytical error: substituting diplomatic headlines for macrofinancial and physical reality.

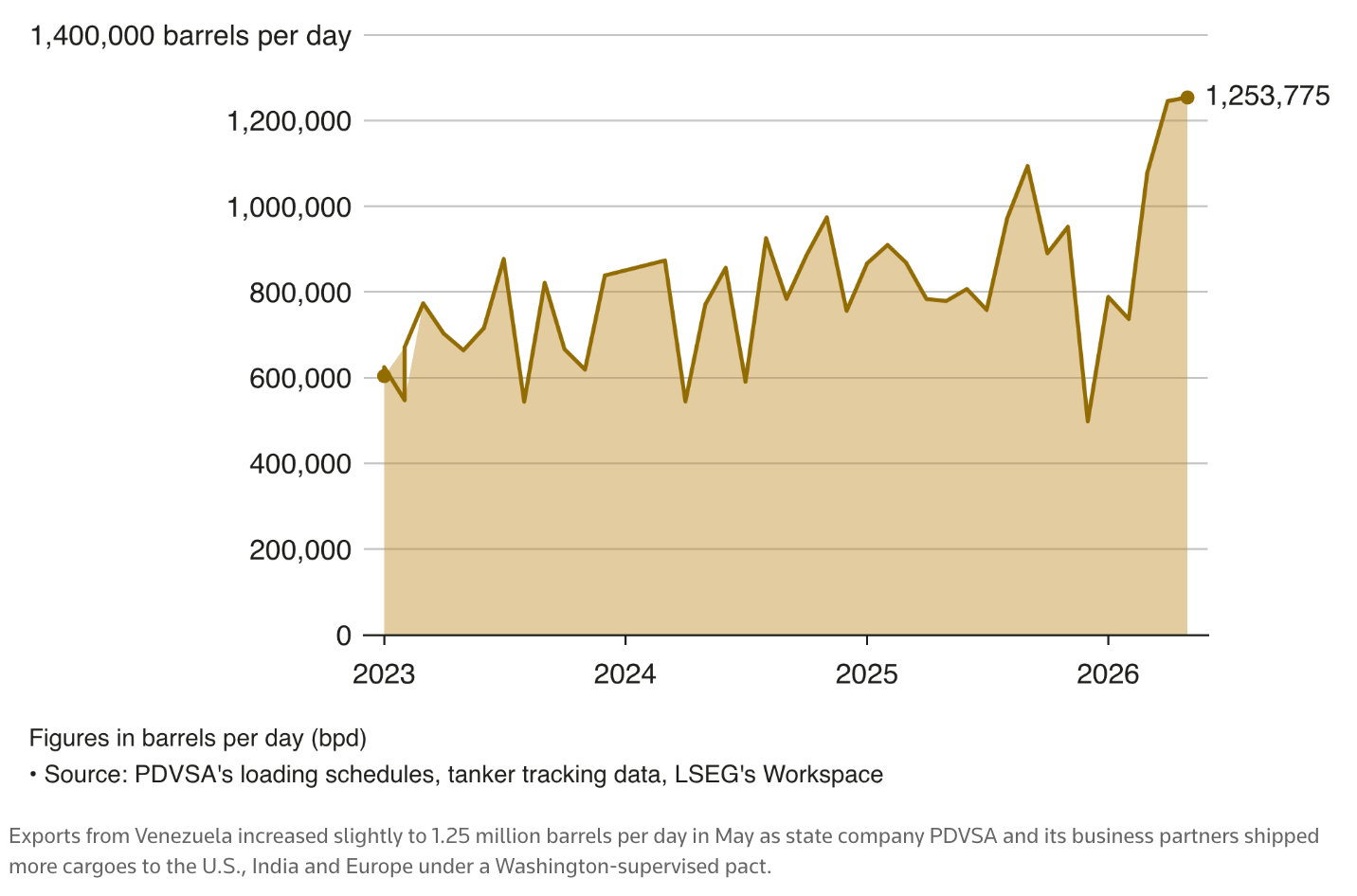

Maintaining output near 1.2 million barrels per day represents low-hanging fruit—the ceiling of marginal operational workovers by incumbent international oil companies (IOCs) like Chevron and Repsol. These operators are deploying zero greenfield CapEx; they are operating under strict debt-recovery waivers, reinvesting only localized cash flows without assuming balance-sheet risk.

Underneath headline volumes, the physical capital stock is severely depleted. As documented by Piergiuseppe Fiore in the Society of Petroleum Engineers (SPE, February 2026), rehabilitating corroded pipelines and extra-heavy crude upgrading facilities mandates an uncompromising 5-to-7-year technical overhaul. Furthermore, the sovereign is immobilized beneath a $150+ billion external debt wall, which halts international risk underwriting. Francisco Monaldi (Rice University’s Baker Institute, January 2026) confirms that breaching the 2-million-barrel-per-day threshold requires a sustained $100 billion CapEx program over a decade—roughly $10 billion annually. This requires heavy industrial engineering and project finance, not political sentiment.

2. The Global Liquidity Drought and Sovereign Crowding-Out

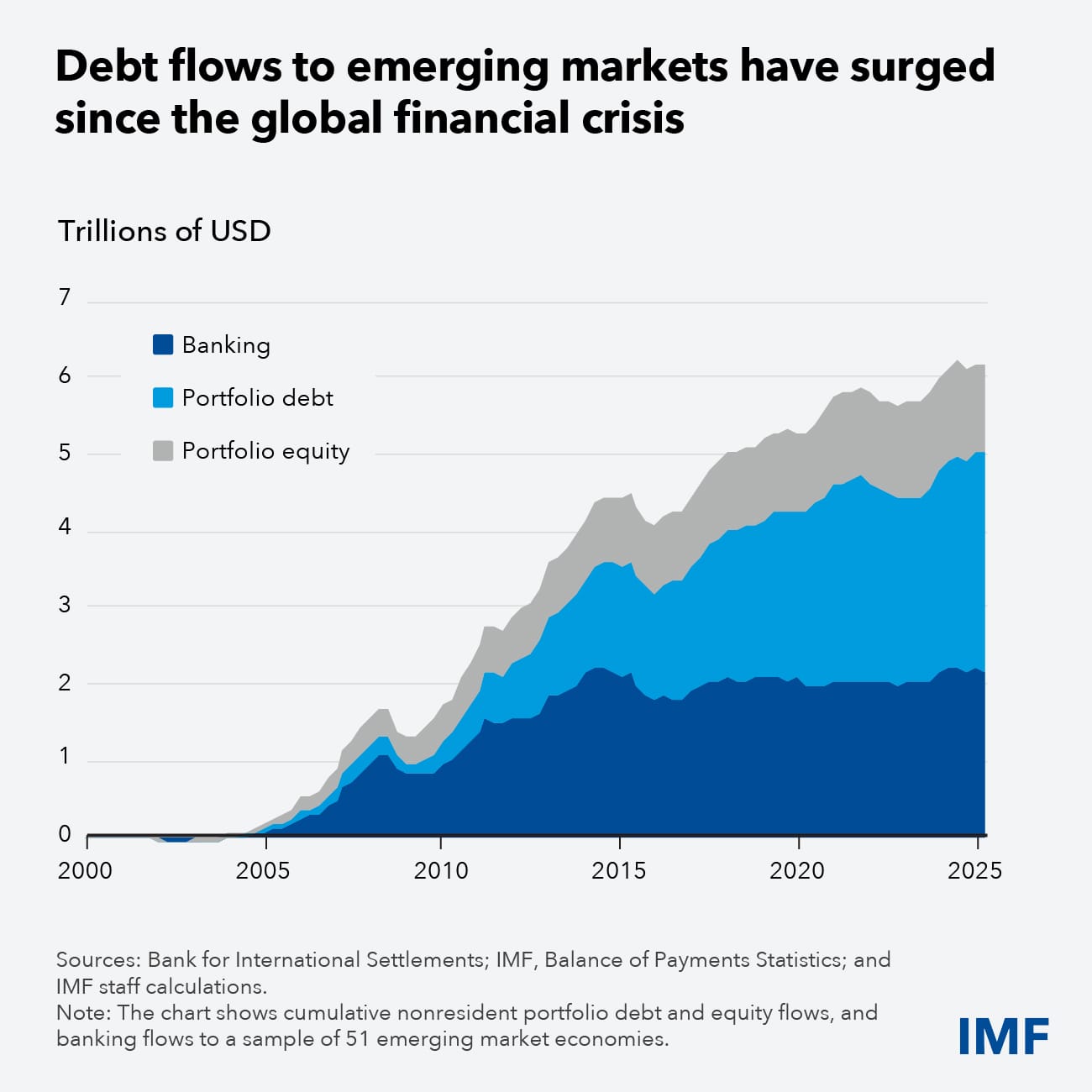

As of July 2026, emerging markets are facing an acute Global Liquidity Drought. Non-bank financial institutions (NBFIs), which hold over 80% of emerging market portfolio debt, are aggressively compressing risk. Confronted with elevated base rates and geopolitical shocks, institutional capital is executing sudden stops across high-yield developing jurisdictions. Simultaneously, Bank for International Settlements (BIS, 2026) locational data confirms that cross-border bank claims in U.S. dollars have stagnated, leaving Latin American sovereign lending paralyzed.

Shut out from international debt capital markets, vulnerable sovereigns are forced to tap domestic banking systems. This Crowding-Out dynamic absorbs local liquidity and denies essential commercial refinancing to industrial sub-contractors. Contrary to retail prediction market assumptions that PDVSA can self-fund via current oil sales, internal cash generation faces total free cash flow cannibalization. Gross export revenues are immediately siphoned off by legacy creditor arbitration claims, multilateral debt service, and basic operational survival, leaving zero net liquidity for capital deployment.

Will Venezuela’s gross oil production return to pre-crisis levels (2M+ barrels/day) before 2028 end?

3. The Capital Monopoly: Big Tech AI vs. Emerging Market Debt

This emerging market refinancing crisis is exacerbated by an unprecedented structural drain: Artificial Intelligence. In its April 2026 Global Financial Stability Report (GFSR, Chapter 2 & Box 1.3), the International Monetary Fund (IMF) explicitly warns that hyperscaler compute infrastructure is monopolizing global debt capacity. The IMF projects AI data center buildouts will absorb $2.9 trillion in CapEx by 2028, siphoning over $800 billion from the private credit market.

By contrast, total private credit allocation across all emerging market infrastructure sits below $100 billion. For institutional asset managers (e.g., BlackRock, Brookfield), capital allocation is dictated by risk-adjusted arbitrage and collateral enforceability. Financing a North American GPU cluster secured by an investment-grade Big Tech balance sheet provides enforceable collateral and guaranteed yields, vastly outperforming the risk profile of an unhedged brownfield project in the Orinoco Belt. AI financial engineering is directly crowding out Latin American infrastructure reconstruction.

(also see our analysis on big tech company Capex & operation dilemma)

4. The Physical and Legal Impasse of a V-Shaped Recovery

On the ground, the V-shaped recovery thesis collides with an immediate two-pronged bottleneck: geological math and legal deadlock.

The most definitive physical barometer is the Baker Hughes Rig Count. Through mid-2026, active drilling rigs in Venezuela have flatlined at 2.00 active units—a 98% collapse compared to the 80 to 100+ rigs deployed in the early 2010s. In mature reservoirs exhibiting a natural decline rate of 15% to 20% annually, operating two rigs guarantees an imminent net production contraction, not a recovery.

Furthermore, the International Energy Agency (IEA OMR, May 2026) highlights a critical diluent bottleneck. Orinoco extra-heavy crude (Merey 16) cannot flow through pipeline networks without being blended with imported naphtha or light condensates. Securing these diluent cargoes requires an immediate upfront cash-burn in hard currency—working capital that PDVSA cannot access.

Finally, the April 2026 legal deadlock surrounding CITGO Petroleum illustrates sovereign insolvency. Encumbered by $20 billion in enforceable creditor judgments and restrained by the U.S. Treasury’s Office of Foreign Assets Control (OFAC), PDVSA is stripped of its primary foreign refining subsidiary, eliminating any capacity to capture international downstream refining margins.

In a global market facing tight capital constraints, where will institutional infrastructure funds prioritize deployment?

5. What Prediction Markets Are Missing: The Trader’s Checklist

For event contract traders positioning on Kalshi or Polymarket across 2026 and 2027 expiration cycles, capturing alpha requires ignoring political narratives and monitoring macrofinancial plumbing:

- J.P. Morgan EMBI (Venezuela Sub-Index): The primary feasibility filter. Until defaulted sovereign debt spreads compress to viable levels, international commercial banks will refuse to underwrite the credit facilities required for pipeline rehabilitation.

- IMF GFSR AI Private Credit Volumes: The global liquidity filter. Track Big Tech debt issuance and securitization absorption. The more private credit capacity AI compute consumes, the less liquidity remains available for high-yield Latin American risk.

- Baker Hughes Monthly Rig Count: The physical arbiter. If an event contract prices in a surge in gross barrel output over a 12-month horizon but active drilling rigs fail to scale exponentially, the market is structurally mispriced—signaling a high-conviction opportunity to short the contract (Bet NO).

References & Institutional Sources:

- Baker Hughes. (2026). International Rig Count: Latin America – Venezuela. Baker Hughes Energy Data Hub.

- Bank for International Settlements (BIS). (2026). International Banking Statistics and Global Liquidity Indicators. BIS Quarterly Review, International Financial Market Developments.

- Blackmon, D. (2026, April 2). CITGO Sale Twists In The Wind As Treasury Department Stalls. Forbes, Energy & Public Policy Analysis.

- Fiore, P. (2026, February). Venezuela Case History: Natural Resources, Operational Collapse, and Impact on Global Energy Business. Society of Petroleum Engineers (SPE) / Journal of Petroleum Technology (JPT).

- International Energy Agency (IEA). (2026, May). Oil Market Report: World Oil Supply – Latin America and Venezuela. IEA Publications, Paris.

- International Monetary Fund (IMF). (2026, April). Global Financial Stability Report: Global Financial Markets Confront the War in the Middle East and Amplification Risks. Chapter 2: "Capital Flows to Emerging Markets" & Box 1.3: "Required Financing and Securitization for Data Centers".

- Monaldi, F. (2026, January 26). Without Institutional Change, Venezuela's Oil Bonanza Remains Unviable. Rice University’s Baker Institute for Public Policy / Americas Quarterly.