S&P Global downgraded Oracle's long-term credit rating from BBB (Negative) to BBB- (Stable), citing elevated business risk and weaker near-term cash flows.

While the downgrade came as a surprise given Oracle's positive credit factors such as customer prepayments and the expansion of its Bring Your Own Cloud (BYOC) model, analysts believe the decision primarily reflects S&P's increasingly cautious view of the AI infrastructure sector rather than a sharp deterioration in Oracle's standalone fundamentals.

According to Barclays, the downgrade is driven by concerns over the industry's high capital expenditure requirements, intensifying competition, and rising component costs as AI infrastructure investment accelerates.

Will AI infrastructure capital expenditure growth decelerate in 2H2027?

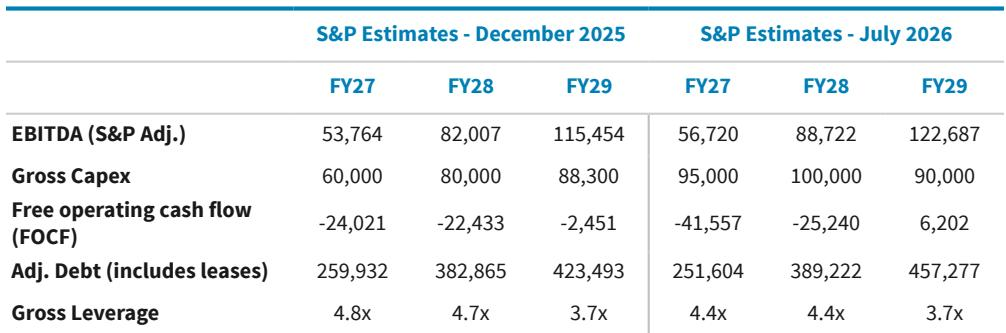

At the same time, S&P actually raised several of its long-term financial forecasts for Oracle, signaling continued confidence in the company's earnings potential. The agency increased its 2027 adjusted EBITDA forecast to $56.72 billion (from $53.76 billion) and lowered its projected peak leverage to 4.4x (from 4.8x), despite raising expected capital expenditures to $95 billion (from $60 billion) and forecasting free operating cash flow (FOCF) of -$41.56 billion (versus -$24.02 billion previously).

Will Oracle's gross leverage exceed 4.4x at the end of FY2027?

Although Oracle now sits at BBB-, the lowest investment-grade rating before high yield, the accompanying Stable outlook was more constructive than many investors had expected. The rating also leaves Oracle with limited room for further leverage-driven deterioration, which may increase management’s incentive to rely more on equity financing or other non-debt funding sources after 2026.

Market pricing suggests that a meaningful amount of credit concern has already been reflected in Oracle’s spreads. The company’s credit spreads trade wider than those of Charter Communications, despite both issuers sitting near the investment-grade boundary. This indicates that Oracle is already being valued with a significant risk premium. For investors who believe Oracle can eventually convert its AI-related capital spending into stronger earnings and cash flow, current spread levels may offer a more attractive risk-reward profile, even as the company navigates an unusually capital-intensive investment cycle.

Source: https://www.macrostream.ai/articles/6a501de8ee1fb5bdec94ab1d