As a Burnham premiership is almost priced in by prediction markets, in my opinion, it turns UK equities into a test of fiscal credibility and sector-specific policy risk. The first question is not whether Burnham is left-wing or pro-growth. The first question is whether investors believe his government can spend more, reform more, and still keep the bond market calm.

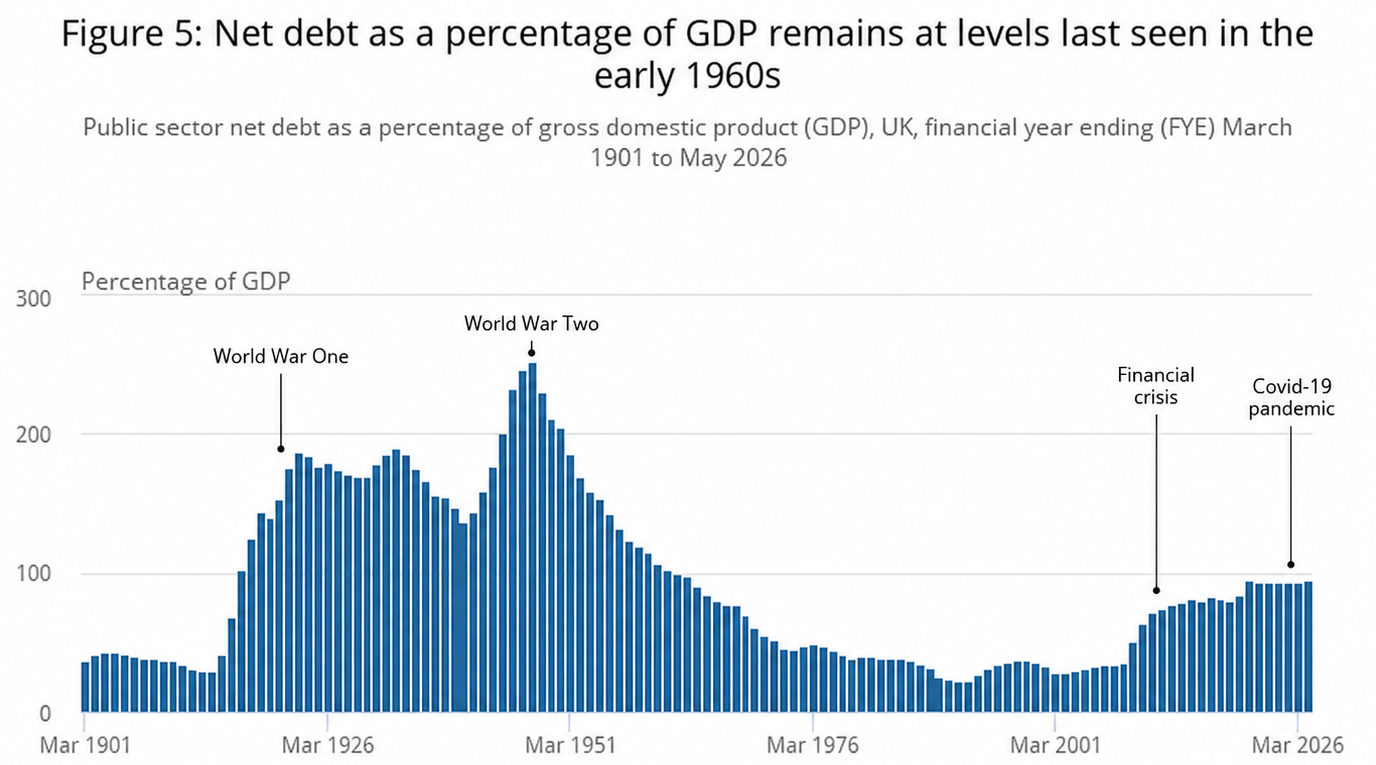

The UK already has a fragile fiscal backdrop. UK borrowing in May 2026 was £23.3bn, while central government debt interest payable reached £11.7bn, the highest May figure since 2020. The OBR also expects public sector net debt to rise from around 90.6% of GDP in 2025-26 to 94.5% in 2029-30 before easing. Public debt is high, debt interest is biting, and the gilt market has become the transmission channel for political risk. In that environment, the issue is whether investors view "good borrowing" as credible, growth-enhancing borrowing or as another sign that fiscal discipline is weakening and that they can demand higher rates.

My base case is that Burnham does not trigger an immediate crisis, but he raises the equity market’s sensitivity to each fiscal signal: the speed of the leadership transition, the choice of Chancellor, the first Budget, and the wording around "public control".

Reuters suggests investors are already watching the Chancellor choice closely. The Chancellor choice tells the market what kind of Burnham government it is dealing with. A continuity choice would suggest an attempt to preserve market credibility, even if the political agenda shifts. A soft-left choice would point toward higher investment borrowing, more tax rises, and a more active state. A reform-minded choice could be the most interesting outcome, with potentially more radical changes to property tax, welfare, pensions, and spending efficiency, but also with higher execution risk.

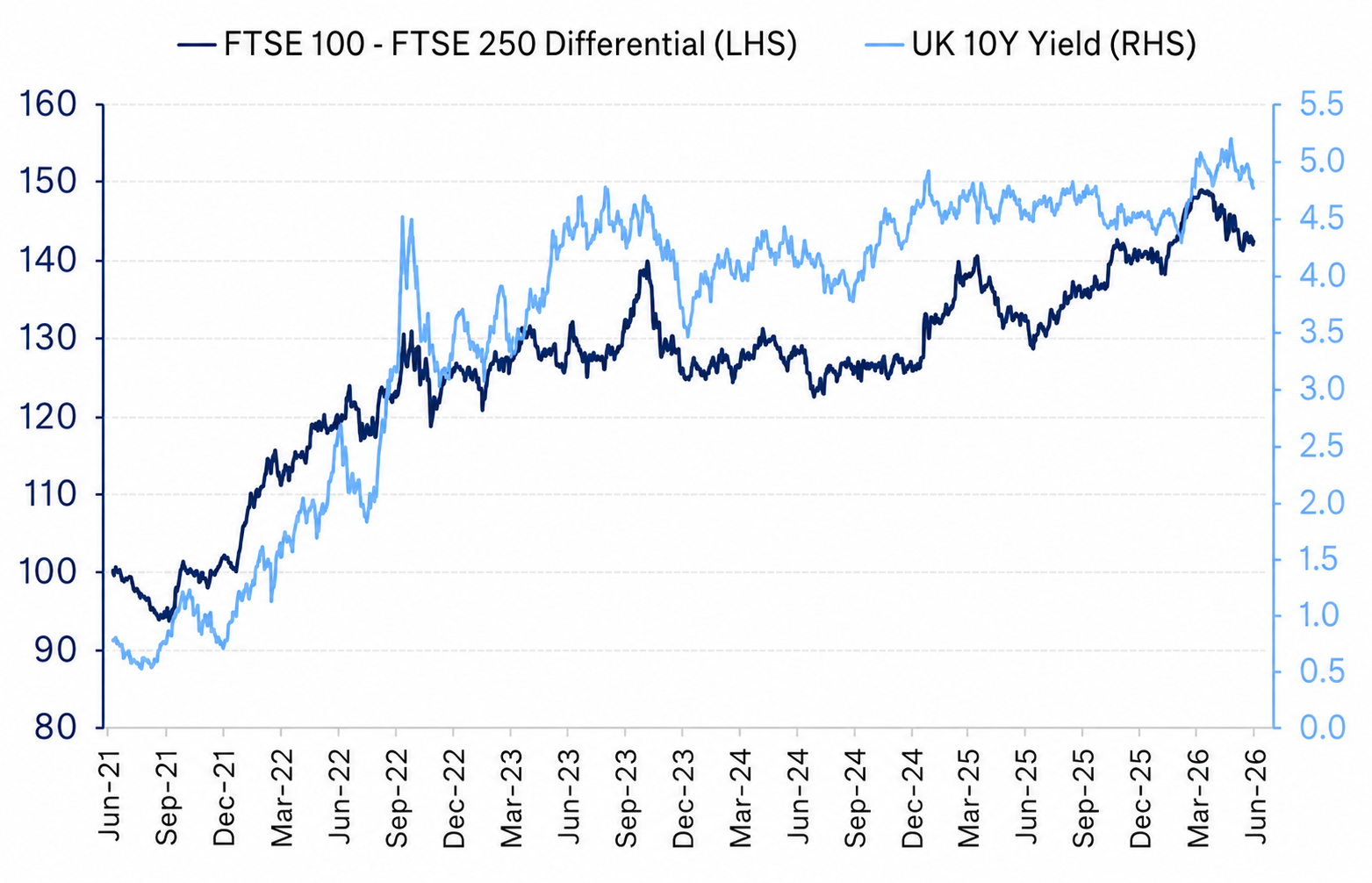

FTSE 100 over FTSE 250 if Yields Go Up

The cleanest equity implication when yields go up is FTSE 100 over FTSE 250. The FTSE 250 is more domestic, more rate-sensitive, and more exposed to UK-specific risks. The FTSE 100 is more international, more dollar-linked, and has heavier exposure to foreign revenues. Over 80% of the FTSE 100 constituent sales come from outside the UK, while the FTSE 250 is much more domestic, with overseas sales closer to 55% and UK revenue exposure around 43%. The US exposure also differs sharply. The FTSE 100 derives nearly 30% of revenue from the US, versus about 10% for the FTSE 250.

When 10-year gilt yields rise, the FTSE 100 tends to outperform the FTSE 250. And this is why I would treat a Burnham premiership as a relative trade first: large-cap international UK over mid-cap domestic UK.

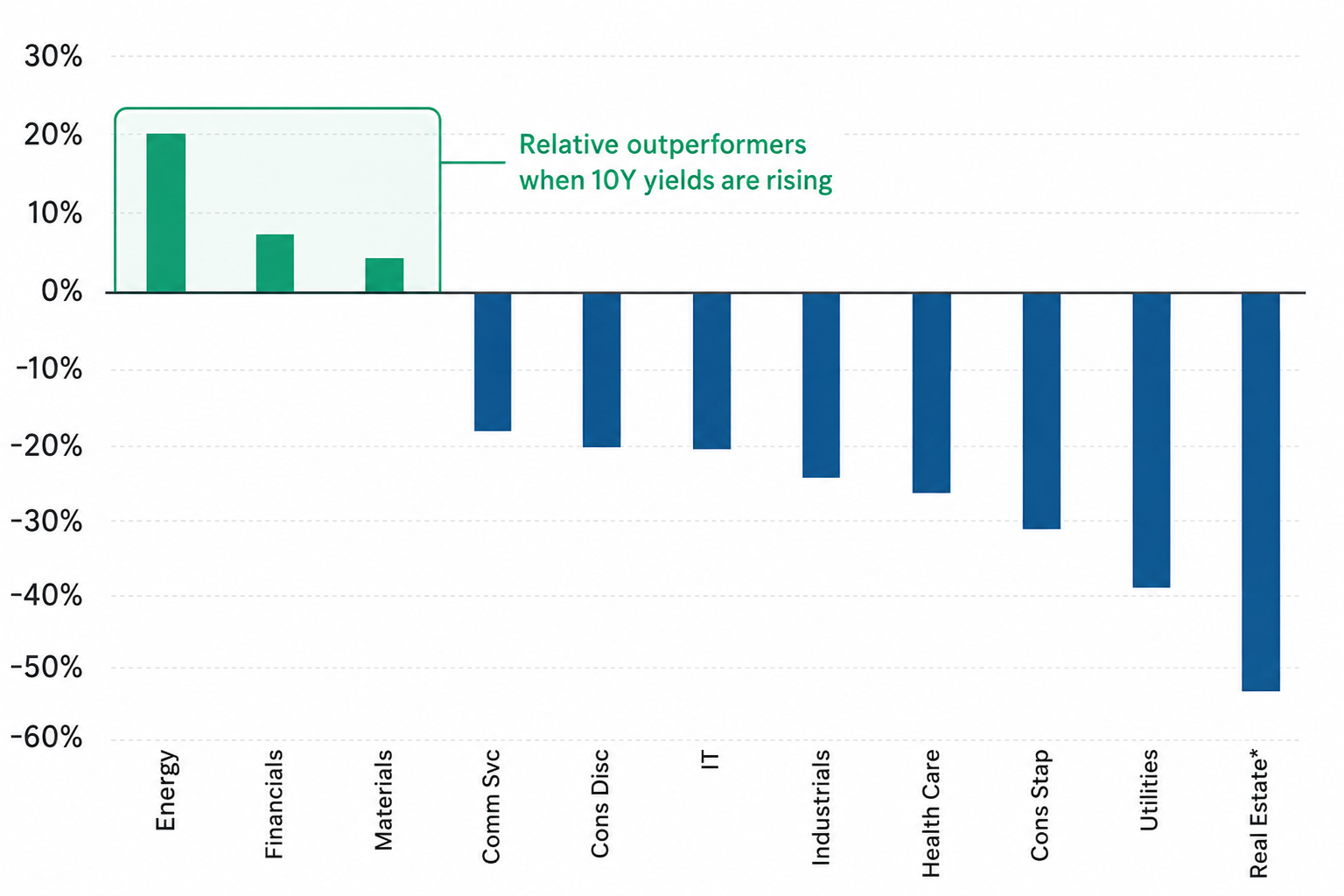

Energy and Resources Are Protected by Global Exposure

Sector-wise, energy and basic resources should be relatively insulated from a Burnham-led UK policy shock because their earnings are globally driven. They also benefit from their international revenue base and potential sterling weakness. Moreover, energy is one of the sectors that tends to benefit in relative terms when UK yields rise.

There is one domestic caveat: Burnham may face pressure from unions, climate groups, and industrial-policy factions over North Sea oil, net zero, and clean power. The Guardian has already framed climate and North Sea policy as one of the early tests of his leadership. But for large integrated energy names, the UK policy component is usually smaller than global factors like commodity prices, global capex discipline, and FX translation. I would therefore view energy as a relative hedge inside UK equities.

Real Estate Has the Weakest Setup

Real estate is the clearest loser from a higher-yield Burnham scenario. That makes intuitive sense. Higher discount rates reduce asset values, higher mortgage rates reduce affordability, and policy uncertainty can freeze transaction activities.

Housebuilders are also caught in a complicated policy cross-current. On the positive side, a reformist government could push planning, infrastructure, and regional development. On the negative side, fiscal pressure makes property taxation tempting. That could be good for long-term efficiency, but in the short term it creates uncertainty for residential property equities.

Utilities and Burnham's "Public Control" Language

Utilities are the most interesting sector because the top-down and bottom-up views conflict.

Top-down, utilities are rate-sensitive and therefore vulnerable if a Burnham premiership means higher borrowing and higher gilt yields. The broad equity framework puts utilities among the sectors that face headwinds when yields rise. There is also a political headline risk because Burnham has used "public control" language around energy, water, housing, and transport.

Bottom-up, however, the nationalisation fear may be overdone. "Greater public control" may mean more strategic planning, regional coordination, and regulated investment, not outright public ownership of listed utilities. In addition, UK electricity networks and water companies have regulatory mechanisms that pass through some inflation and financing-cost pressure. For electricity transmission, half of the regulated asset base is CPIH-indexed, while allowed debt and equity returns adjust through regulatory mechanisms. For water, the RAB is fully CPIH-indexed, and water companies can still deliver 10% plus nominal returns over the regulatory period to 2030.

Therefore, I would separate this sector into different buckets.

First, companies with underlevered balance sheets and exposure to higher or more volatile power prices look better positioned. Centrica and Drax are in this category.

Second, electricity networks may still be structurally supported because the UK needs grid investment for clean power and electrification. Official planning is also moving toward more centralized energy-system coordination through NESO’s Strategic Spatial Energy Plan and Regional Energy Strategic Plans.

Third, water names remain politically exposed, but valuation and regulation matter. This is the kind of sector where political headlines can create forced selling, but the actual cash-flow mechanics may be more resilient than the first reaction suggests.

What to watch next

First, the leadership process. A quick transition would calm markets and support gilts, helping domestic equities. A prolonged contest would keep fiscal uncertainty high and likely favour FTSE 100 over FTSE 250.

Second, the Chancellor. This matters more than the leadership result. A continuity pick would reassure markets, while a soft-left choice implies more borrowing and taxes. A reform-minded option could be positive, but only with credible fiscal plans.

Third, fiscal rules. The key is not whether they change, but whether any extra borrowing is tied to productive investment and a credible debt path. Markets will react differently to growth-focused spending versus fiscal drift.

Fourth, “public control.” Nationalisation rhetoric would pressure utilities, while a focus on regulation and coordination could ease concerns.

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.