The White House shows factory activity at a four-year high, framed as proof that manufacturing is "roaring back" to American soil. Markets have mostly bought the framing: reshoring means jobs, jobs mean wage growth in the industrial belt, and industrial belt strength is bullish for the broad reflation trade.

Since the reshoring wave started showing up in investment announcements, more than $1.7 trillion in U.S. manufacturing capital commitments has coincided with factory payrolls falling by roughly 75,000 from January 2025 to June 2026. Since January 2023, the ISM's manufacturing employment index has now contracted in 41 of the last 42 months. June's headline PMI expanded for a sixth straight month, but the jobs component stayed underwater.

The market is pricing reshoring as an employment story. But the more durable story is an automation story that happens to be wearing a jobs costume.

Is the reshoring boom mainly a jobs story or an automation story?

Twenty straight months of expansion is not nothing

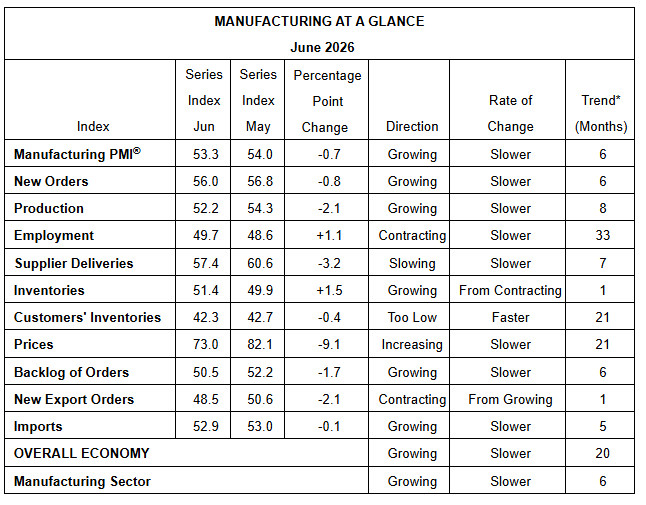

The bull case for "reshoring means jobs" isn't naive. With a PMI above 47.5 again in June (which is considered as a threshold for expansion by PR Newswire), overall economy has been in expansion territoriality for 20 months, and new orders have grown for six consecutive months.

Source: PR Newswire

This activity has real capital behind it, as two of just four major industries reporting both rising new orders and rising production in June: semiconductor investment (computer & electronic products) accounting for more than $640 billion of announced commitments and pharmaceutical pledges (chemical products) from major drugmakers have topped $500 billion.

Politically, this is a genuinely popular and genuinely large capital cycle, and capital cycles of this size have historically shown up in payrolls eventually. Traders betting that "more factories" eventually equals "more factory workers" are extrapolating from a century of prior cycles.

The weak assumption: Capital committed is payroll committed

The weak assumption is that investment dollars are a decent proxy for headcount. They aren't anymore, and the split has been visible in the data for over a year now.

The composition of the current investment wave is the tell. According to Reshoring Initiative, 90% of the manufacturing jobs actually announced through reshoring and foreign direct investment in the most recent full year were classified as high-tech or medium-high-tech: semiconductor fabs, advanced materials, EV battery plants, up from 88% the year before.

This split is already visible in the same ISM data behind the bull case above. In June, Computer & Electronic Products, the category that includes semiconductor manufacturing, was one of just four major industries reporting both rising new orders and rising production. It did not make the much shorter list of industries reporting employment growth. The orders are showing up in exactly the industry doing the most reshoring-driven growing. The hiring isn't.

When 81% of businesses say they'd favor automation over hiring people if production returns to the U.S., and when 92% of manufacturers say smart manufacturing (not headcount) will be the main driver of their competitiveness over the next three years, the capital being counted as "reshoring investment" is substantially capital being spent to avoid the labor problem, not solve it with headcount.

Forty-one percent are already prioritizing factory automation hardware investment over the next two years, even though only 29% currently use AI or machine learning at the facility level, so the intent to automate is running well ahead of the infrastructure to do it.

The split is already showing up in four places

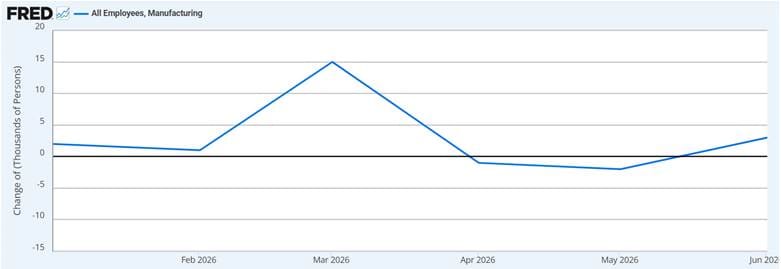

1. Monthly BLS manufacturing payrolls

Manufacturing added just 3,000 jobs in June after shedding 2,000 the previous month. On its own, it may sound positive, but against $1.7 trillion in announced capital and 12.6 million existing manufacturing workers, 3,000 is statistical noise.

If monthly adds start climbing into the tens of thousands and hold there, the job thesis could gain real ground, but otherwise, this flatline is an automation thesis, one release at a time.

Source: FRED

2. Average workweek and overtime hours

Average workweek and overtime hours show whether firms are squeezing existing staff instead of hiring. According to BLS, manufacturing's average workweek actually edged down in June while overtime edged up, a pattern more consistent with firms optimizing scheduling and automation around a fixed headcount than one consistent with a hiring wave.

This could be firms buying capacity from machines and shift management rather than the labor market.

3. Robot order and capex data

North American robot orders rose 6.6% in 2025 to the highest level since 2022, and industry group A3 just reported its most attended trade show ever in June 2026, with collaborative robot orders up more than 50% year-over-year in Q1.

4. Semiconductor employment intensity

Semiconductors is one of the largest categories of announced reshoring jobs, accounting for about 67% alongside EV batteries and solar, and fabs are among the most capital-intensive, least labor-intensive facilities in manufacturing. As fab construction shifts from building phase (which does employ a lot of construction labor) to operating phase (which doesn't need nearly as many people), watch for regional payroll data in fab-heavy states like Arizona and Texas to show hiring plateaus even as production ramps.

What to watch next

The next BLS Employment Situation report, covering July, lands August 7, and will show whether manufacturing payrolls stay stuck near zero or start closing the gap with the capex headlines. ISM's July manufacturing report follows shortly after, and the number that matters is whether the employment subindex holds above 48 or breaks back toward the low 40s.

The bigger date is August 28, when BLS publishes its preliminary annual benchmark revision to the establishment survey, based on unemployment-insurance tax records rather than the sampled monthly survey.

This revision has a real chance of moving the manufacturing jobs numbers more than any single monthly print this year, in either direction.

Sources:

- BLS: Job Openings and Labor Turnover Survey News Release

- BLS: The Employment Situation June 2026

- Business Wire: A3’s Automate 2026 Breaks Records as Demand for Robotics, AI and Automation Grows

- CNBC: Trump tariffs won’t lead supply chains back to U.S., companies will go low-tariff globe-hopping: CNBC survey

- Deloitte: 2025 Smart Manufacturing and Operations Survey: Navigating challenges to implementation

- FRED: All Employees, Manufacturing (MANEMP)

- IndustrialSage: U.S. Manufacturing Investment Tracker

- Manufacturing Dive: Manufacturing industry gained 3,000 jobs in June

- PRNewswire: Manufacturing PMI® at 53.3%; June 2026 ISM® Manufacturing PMI® Report

- Reshoring Initiative: Reshoring Initiative® 2024 Annual Report

- Reuters via Yahoo Finance: Factbox-Global drugmakers rush to boost US presence as tariff threat looms

- Semiconductor Industry Association: America’s Chip Resurgence: Over $640 Billion in Semiconductor Supply Chain Investments

- The Robot Report: North American robot orders rise by 6.6% in 2025, reports A3

- White House: Trump Effect: American Manufacturing Is Roaring Back as Factory Activity Hits Four-Year High