Most people open a prediction market and see probabilities.

A contract trading at 52 cents? The market thinks the event has a 52% chance.

A contract trading at 9 cents? Longshot.

A contract trading at 98 cents? Basically done.

That is the normal way to read these markets. But it is somewhat incomplete.

Because when an event contract gets close to certainty, it starts to behave less like a bet and more like a bond.

Not always. A 50-cent contract or a 10-cent longshot is still mostly about information. But a 98-cent contract that will not redeem for six months? That is a different animal. It is essentially a tiny fixed-income product wearing a prediction-market costume.

Do you understand what the word "bond/bonding" means in prediction-market contexts?

From odds to yield

Prediction market prices are often interpreted as probabilities because of its payout structure: a winner-take-all contract pays $1 if an event happens and $0 if it does not. Wolfers and Zitzewitz famously provided a theoretical case for why prediction market prices can be treated as probability-like signals under reasonable assumptions (but some are sometimes non-negligible in real life!).

This idea is useful. It is why prediction markets are interesting in the first place.

But it works best when the main question is still "Will the event happen?"

Near certainty changes the question and shifts the focus to something else.

When a contract trades at 97, 98, or 99 cents, the important question may no longer be "am I right?" It may be "When do I get paid?" or "Should I hold the contract into resolution or sell it now?"

That is the fixed-income layer hiding inside prediction markets.

A normal bond asks:

- How much do I pay today?

- How much do I receive later?

- How long do I wait?

- What risk do I take while waiting?

A near-certain prediction market contract asks almost the same thing:

- Price today: $0.96

- Expected payout: $1.00

- Time to settlement: 300 days

- Risks: settlement risk, liquidity risk, platform risk

So yes, it is still a prediction market contract. But economically, it starts to look like a zero-coupon event bond.

What is an event bond?

Let’s define it loosely.

An event bond is a near-certain prediction market position where the main economic question is no longer "will this happen?" but "what yield am I earning while waiting for settlement?"

This is not an official product category. You will not see a tab on Polymarket called "bonds". But the economics are there. The word "bond" is a slang term in the prediction markets community.

When you buy a contract at $0.96 and it later redeems at $1, your nominal gain is 4.17%. But that number is almost meaningless by itself.

If settlement happens tomorrow, that is huge.

If settlement happens in a year, that is the annual yield.

If settlement gets disputed, delayed, or blocked by some platform issue, that gain suddenly looks less sure, and it functions more like a risk premium in order to compensate you.

This only makes sense when event risk is close to zero. If the outcome is still genuinely uncertain, then the contract is not a clean event bond. It is a risky bond with default risk. The closer a contract gets to certainty, the more it starts to look like fixed income.

The Jesus market was not theology but duration

A recent paper, When Certainty Is Not Worth It: Capital Lock-Up and Settlement Discounting in Prediction Markets, makes this idea very clear.

The authors point to Polymarket’s "Will Jesus Christ return in 2025?" market. For months, the near-certain NO side traded around $0.96. At first glance, that looks absurd. Was the market really saying there was a 4% chance of the Second Coming? Probably not.

A better reading is that the market was pricing a delayed dollar. A trader buying NO at $0.96 could earn about 4.2% if the position eventually redeemed at $1, but only after locking capital for most of the year. That discount can be consistent with near certainty once you account for outside returns, liquidity needs, and residual platform risk.

So, the trade was not about miracles. It was about duration, or how much you should be compensated for locking your money in the contract for almost a year.

A contract below $1 does not always mean the market thinks the event still has real uncertainty. Sometimes the market is saying, "believe this wins, but I need to be paid to wait."

The hidden yield curve

The paper formalizes this as settlement-induced discounting. Instead of treating price as pure probability, it writes the price as: Price = Expected payoff × Settlement discount.

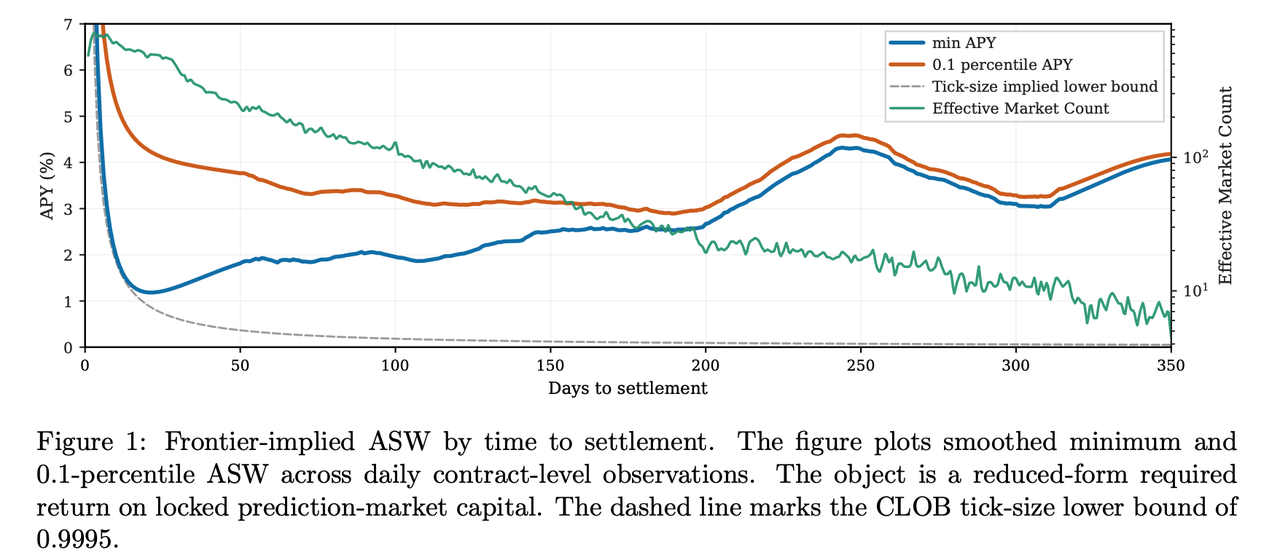

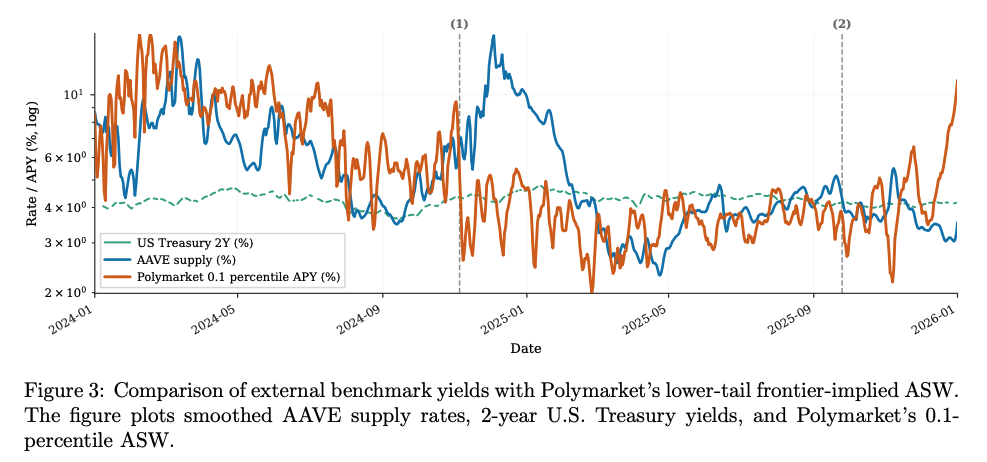

The settlement discount captures the value of delayed redemption, capital lock-up, outside opportunities, liquidity demand, and residual platform or oracle risk. The authors summarize this discount as an Annualized Settlement Wedge, or ASW, which is basically the implied required return for capital locked in near-certain prediction market claims.

In other words, prediction markets have a hidden yield curve. It is not printed on the homepage. It is implicit in the prices and appears when near-certain contracts refuse to trade at $1.

The paper finds that the ASW is positive, maturity-dependent, and time-varying.

Many long-dated high-probability contracts look like they underprice certainty, but a lot of that apparent mispricing is actually the price of locked capital. People love to call these trades "free money". But they are often not free money. They are yields, with risks.

On the other hand, a lot of near-settlement contracts offer attract yields on an annualized basis. These are great opportunities, but those gains are one-off only. You cannot earn the full annualized gains since they are not recurring profits.

Why this changes how we read prediction markets

Prediction markets are financial markets, not magic probability dashboards. Some prediction market mispricing is informational. Some are behavioral. Some come from thin liquidity or retail demand. But near certainty reveals mostly funding friction.

This also helps explain why long-horizon markets are hard. Earlier research found that markets are reasonably well calibrated in short horizons but can become biased further from expiration. When the time value of money is considered, exploiting miscalibration depends on the trader having a low enough discount rate.

Another paper on interest-bearing positions makes a similar design point from another angle: long horizons can reduce liquidity and accuracy because committed capital has an opportunity cost, while paying interest can reduce the horizon effect and increase participation.

In other words, long-dated uncertainty is expensive because capital has alternatives. If a platform wants better long-term pricing, it cannot only attract smarter traders. It also has to make capital more productive.

Why collateral matters

Event contracts are fully collateralized. Each complete YES/NO pair is backed by $1 of collateral locked in the system. In simple terms, when traders enter positions, capital is committed to the system and remains tied up until they exit or the market settles. That locked capital has an opportunity cost, especially in long-dated markets.

Therefore, long-dated near-certain contracts should trade at a discount. Someone has to be compensated for tying up money that can be useful elsewhere (e.g., earning interests in banks, committing to alternative investment opportunities).

But if platforms pay yield on collateral or open positions, that discount should shrink.

Kalshi introduced interest accrual on cash and open positions in March 2026, explaining that users can earn interest on the underlying collateral even before a market resolves. Its help page listed a 3.25% variable interest rate for eligible accounts.

Polymarket also introduced Holding Rewards for certain long-term markets, describing them as rewards on eligible positions designed to help maintain long-term pricing accuracy. Its help page listed a 3.25% annualized reward rate on total position value for eligible markets, with rewards sampled hourly and distributed daily.

That sounds like a small product feature. It is bigger than that. Once open positions can earn yield, event bonds stop being just an analogy. They start behaving even more like fixed-income instruments.

A 97-cent contract with no collateral yield is different from a 97-cent contract earning 3.25% while you wait. Same event, different bonds.

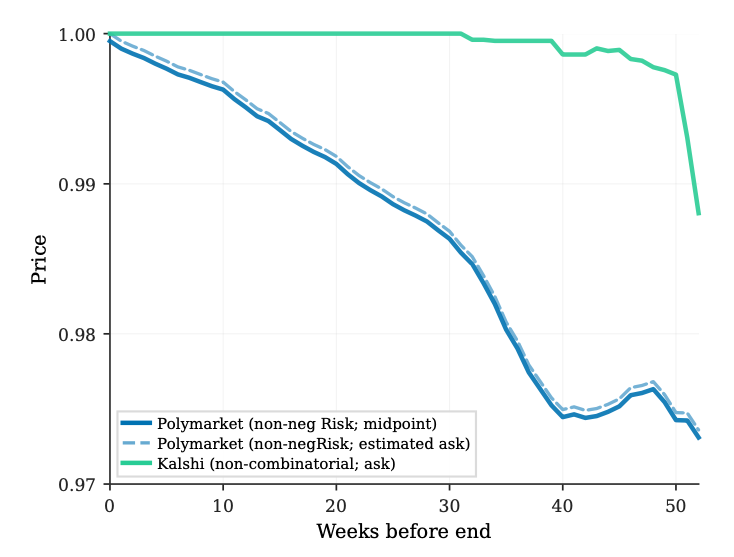

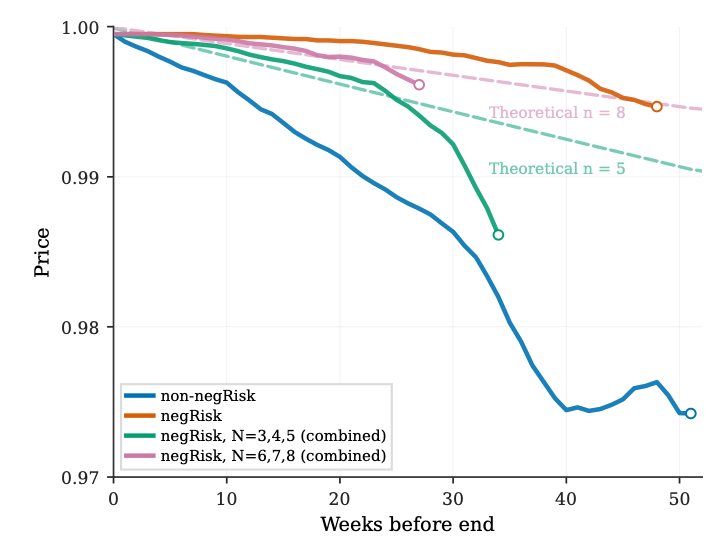

NegRisk as collateral engineering

There is another design feature that matters: NegRisk markets and capital recycling.

In certain mutually exclusive multi-outcome events on Polymatket, baskets of NO tokens can be converted into something closer to cash plus residual exposure. This compresses the settlement discount because part of the position can be recycled rather than staying fully locked until final settlement.

That may sound technical, but the intuition is simple. In fixed income, traders care about collateral, netting, and balance-sheet efficiency. In prediction markets, traders should care about the same things.

A market design that lets you recycle capital makes the claim more cash-like. A claim that is more cash-like should trade closer to $1.

"Free money" is usually just yield

Prediction market starters often say things like, "This is basically guaranteed. Why is it only 98 cents?"

Other traders would ask a better question, "What is the yield, and what risk am I warehousing?"

Before buying a near-certain contract, ask:

- What is the true probability of payout? Are there vague rules that can lead to disputes?

- How many days until settlement?

- What is the yield to settlement? Is collateral earning yield?

- What is my next-best use of capital? What are the yields I can earn elsewhere?

- Why am I being offered this yield?” Maybe the other side simply wants cash now/finds a better opportunity/is closing a winning position/knows something adverse that you are not aware of.

If you do not calculate the yield and risks, you are not trading near-certain contracts. You are just staring at cents, and you will lose big when things don't work out for you.

In addition, the most dangerous part of bonding is psychological. You win again and again, so it feels like the strategy works. But if you are buying 96-cent contracts, even a bad strategy can look good for a long time. The losses are rare, and rare losses do not give fast feedback. You may need hundreds of similar trades to know whether you actually have an edge. This is why a high win rate is not the same as positive expectancy. And Rare events teach slowly.

Would you try the "bonding" strategy in the future?

Disclaimer: The content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this article constitutes a solicitation, recommendation, endorsement, or offer by the author(s) or any third party service provider to buy or sell any securities or other financial instruments in your or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. The author(s) report(s) no conflict of interest.