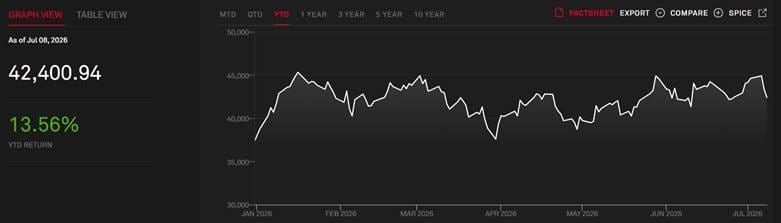

PwC's mid-year 2026 aerospace and defense outlook shows the five largest U.S. primes closing FY2025 with a combined $1.36 trillion backlog, up 23.7% year-over-year. Markets have priced this as record orders, rising budgets, primes trading at 20-25x forward earnings.

The Navy has been trying to deliver two Virginia-class submarines a year since 2011. It is currently delivering 1.3. The Congressional Budget Office puts the average delay at four years past the dates written into the original contracts, and this gap grew, not shrank, between 2025 and 2026, despite billions already spent trying to close it.

Current valuations appear to assume that most backlog converts with relatively limited execution risk. Delayed delivery doesn't shrink the backlog number itself, but it defers revenue recognition, pressures margins on fixed-price contracts, and slows cash generation. Basically, the things the multiple is actually being paid for. But step back and there's a simpler read hiding underneath all three: the market keeps treating a signed contract as a promise the industry can keep on schedule. Increasingly, it can't.

PwC's own report says as much: M&A is now being used as "a practical fix for capacity that organic investment cannot close quickly enough" across aircraft, engines, and shipbuilding.

Put simply, ships, engines, and munitions are stuck behind a wall of missing welders, pipefitters, and electricians.

So, can the industry staff the shop floor fast enough to fill them on schedule?

Where do you come down on defense backlog right now?

Here’s what the market is actually betting on

Defense budgets are expanding on both sides of the Atlantic. NATO members are treating higher spending as a durable planning assumption rather than a crisis response, and PwC notes that European revenue has grown by double digits across major US contractors this year.

Source: SPGlobal

The sector itself has risen roughly 15% since early 2026, outpacing the broader market, and Wall Street's baseline demand assumptions keep getting revised up, not down, as the FY2027 NDAA authorizes $1.15 trillion in military spending, and President Trump has floated pushing the number to $1.5 trillion.

Source: Department of War

On paper, this is a sector with multi-year revenue visibility that few others in the market can match.

What's notable is what the skeptics are actually skeptical about. Wells Fargo's David Strauss cut his Lockheed target by 12% and his Northrop target by 23% this week, but his reasoning was multiple compression after a period of "meaningful underperformance" relative to the defense budget's growth, so a valuation call, not a delivery call.

Nobody on the sell side is downgrading these names because the Navy can't find welders. The debate happening in research notes is entirely about whether the stocks have gotten ahead of themselves on price.

The issue? The market is pricing contracts as if they were deliveries

Companies aren't buying market share. They're buying the physical and human capacity to build things they've already been paid to build. When M&A becomes a substitute for organic capacity expansion, that's a tell that internal capacity isn't growing fast enough on its own.

The clearest example of this problem, though not the only one, is in shipbuilding, where almost all US defense construction capacity sits. Navy Secretary John Phelan said this year that the maritime industrial base needs roughly 250,000 new shipbuilders over the next decade just to hit existing fleet plans.

McKinsey's read of Department of Labor data lands in the same range, estimating a shortfall of 200,000 to 250,000 workers. This isn't a hiring problem that money fixes quickly. According to the same source, about 27% of shipbuilders are already 55 or older, first-year attrition among new welders and electricians runs as high as 20-22%, and a welder qualified for nuclear submarine work takes years of certification, not weeks of training.

The Columbia-class submarine program, the Navy's top acquisition priority, was contracted for an 84-month build and is now tracking closer to 96 months, with delivery pushed toward 2028, according to Congress. The Navy has attributed part of this slip to late turbine generators and a delayed bow section, both manufacturing execution problems rather than funding or design issues.

The Constellation-class frigate program is the more dramatic case: the Navy cut the program from a planned 20 ships to 2 in November 2025, after delays of at least three years pushed the first delivery from 2026 to 2029, driven in large part by workforce shortfalls at the building yard in Wisconsin.

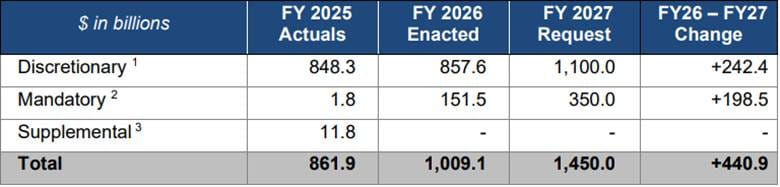

The Pentagon's own FY2027 budget request sets aside $3.1 billion specifically for "wage increases... to recruit and retain workers" at nuclear shipyards, and a separate workforce line for castings, forgings, and munitions plants. This is the government's own diagnosis of the bottleneck, not an outside critic's.

Four triggers to watch next

1. Q2 earnings, late July

Lockheed and Northrop report the same week, RTX close behind. Backlog may rise again, but that's not the number that matters. Watch book-to-bill against free cash flow, and whether more fixed-price charges show up on the same programs that are already behind.

2. Shipyard workforce data from the Department of Labor and Navy budget submissions

The Navy's Maritime Industrial Base program is now tracking hiring against its 250,000-worker target. If those numbers show meaningful progress by early 2027, some of this thesis weakens.

If attrition stays in the 20%-plus range and headcount growth stalls, expect more Columbia- and Constellation-style schedule resets across other programs, including Virginia-class submarines and the next tranche of destroyers.

These programs represent different segments of the industrial base (submarines, the surface combatants, and strategic deterrence), suggesting the issue is broader than a single contractor.

3. Further M&A aimed explicitly at capacity rather than capability

PwC flags distressed acquisitions of qualified facilities and roll-ups of Tier 2/3 suppliers as an active 2026 trend. T3 Defense Inc. (NASDAQ: DFNS) raised $20 million in February specifically to keep buying suppliers it describes in SEC filings as sitting at "critical bottlenecks at the sub-OEM level."

An acceleration of these deals, especially forced or distressed transactions rather than strategic ones, would confirm capacity scarcity is worsening, not stabilizing.

4. Munitions: Delivered units, not stated capacity

The Pentagon's targets call for PAC-3 MSE output rising from roughly 600 to 2,000 units a year by 2030 and PrSM output roughly quadrupling. Lockheed says its PAC-3 ramp is currently running ahead of commitments. If that holds across other programs, and if NATO's roughly sixfold increase in 155mm shell capacity since 2022 keeps translating into delivered rounds rather than just announced capacity, this is the strongest evidence the market has this right rather than wrong.

The gap between capacity announcements and delivered units program by program is the one number that settles this either way.

The bottom line

The market is paying a premium for hardware that doesn't exist yet, on a delivery timeline the industrial base keeps failing to hit, and nobody pricing these stocks is discounting for this gap.

Submarines are four years late.

Munitions ramps depend on workers who don't exist.

Fixed-price programs are bleeding cash on the exact contracts the backlog is supposed to convert.

Until delivery data starts closing the gap, this trade is a bet on an industrial base that hasn't earned the multiple yet.

Which trigger will you actually be watching?

Sources

- Breaking Defense: What the Constellation-class frigate’s cancellation means for Navy, Fincantieri

- CBO: Testimony on Challenges Facing the Navy’s and Coast Guard’s Shipbuilding Programs and the Shipbuilding Industrial Base

- Congress.Gov: Navy Columbia (SSBN-826) Class Ballistic Missile Submarine Program: Background and Issues for Congress

- CSIS: Is the Industrial Base on a Wartime Footing? A Progress Report

- Department of War: Budget Overview Book

- ExecutiveGov: Trump Wants $1.5T Defense Funding for FY 2027 to Build ‘Dream Military’

- GlobeNewswire: T3 Defense Inc. Announces Private Placement of up to $20 Million to Accelerate Acquisition Strategy

- McKinsey & Company: Helming a sea change: Building the future workforce for US shipbuilding

- PwC: A&D dealmaking reprices around capability, backlog, and production certainty

- USNI News: SECNAV: Shipbuilders Need to Hire 250,000 Workers Over the Next Decade for ‘Golden Fleet’

- USNI News: Virginia Subs Will Hit 2-A-Year Build Rate in 2030s, CNO Caudle Says